Growth Thoughts, Continued

Simplifying the growth framework with Copart (again).

Going Deeper On Growth

In a prior post, I examined growth as a concept: How it adds value, and the different ways companies can grow (i.e., margin expansion and/or reinvestment via retained earnings).

In last week’s post, I went deeper and presented a framework for thinking about the sources of growth embedded in our assumptions using a real-world example of Copart (Disclosure: Long).

A Simplified (But No Less Useful) Framework

The value bridge approach presented last week suffered from too much complexity. It wasn’t wrong, just too noisy.

I think a simplified model1 can serve as a useful middle ground between a complex Wall Street-type model with multiple sheets of inputs/assumptions and the too-simplified perpetual growth or shorthand models.

We’ll break the valuation into three components:

What is the value of the existing earning power?

What value is created by reinvestment over the next 10 years?

What is the value of the mature business at Year 10?

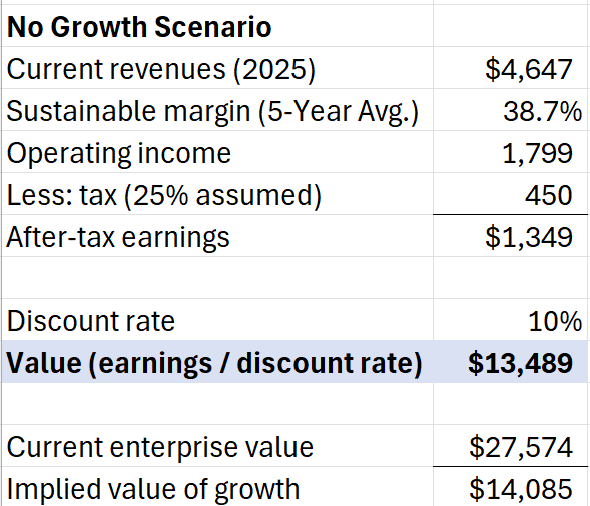

Existing Earnings Power

Note: Bruce Greenwald calls this the Earnings Power Value (EPV).

The base case scenario assumes all earnings are distributed. As such, the value of the business in this scenario is simply the after-tax earnings divided by the discount rate.

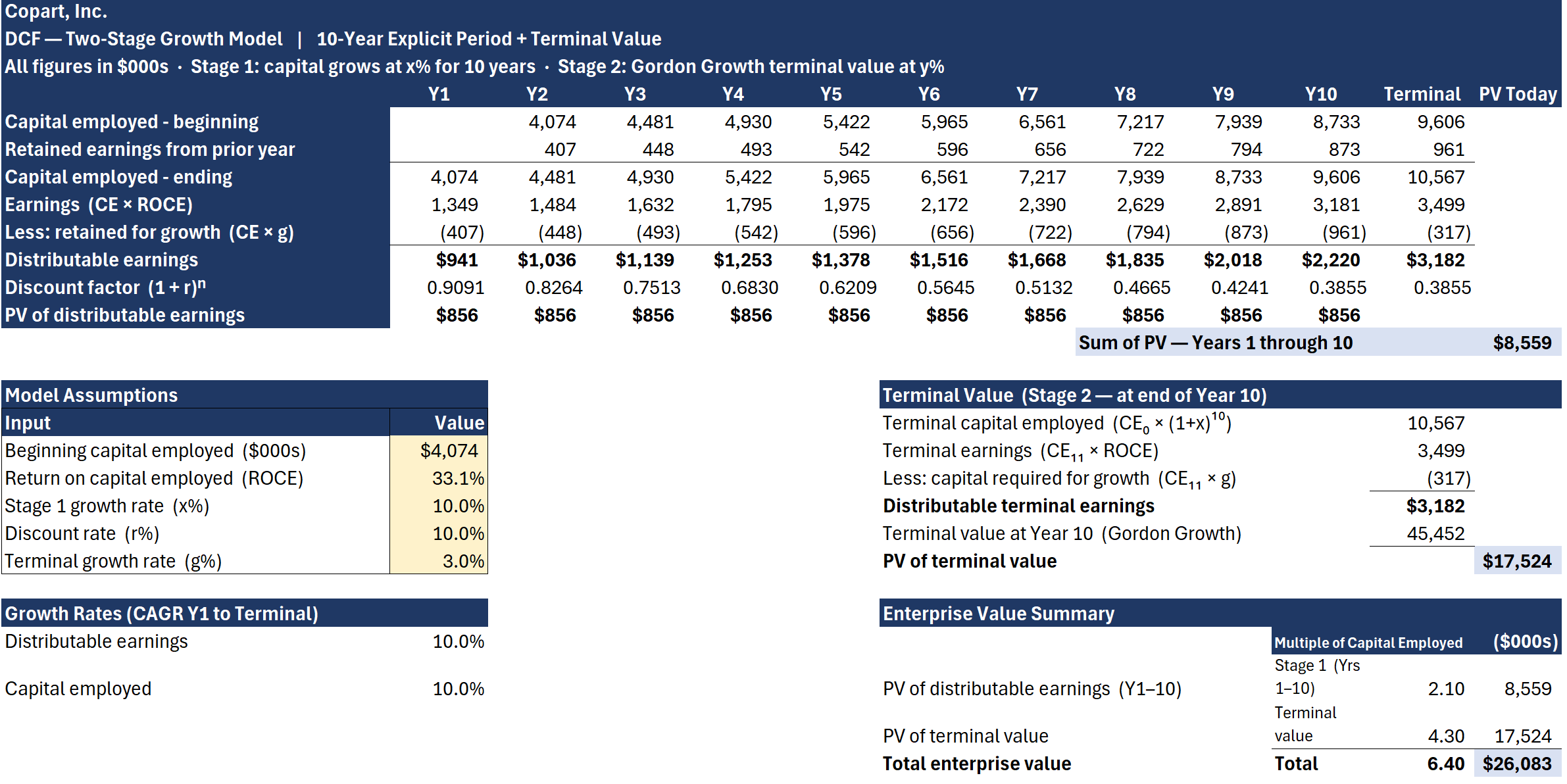

For example, Copart’s sustainable current after-tax earnings are $1,349 million. We take that and divide by 10% (my chosen discount rate) to arrive at a value of about $13.5 billion.

What value is created by reinvestment over the next 10 years?

Providing an explicit growth period followed by a terminal value allows us to segment a value creation period that more closely tracks reality. We’re content to get closer to reality without deluding ourselves that we can predict the exact course of a company’s development.

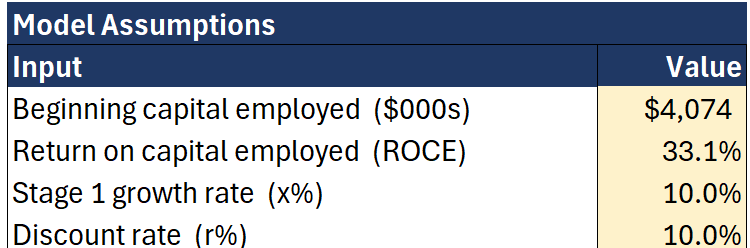

This model uses the same beginning capital employed and return on capital. This time, however, I’m assuming that earnings grow at 10% per year for the first ten years.

Note that by using a growth rate equal to the discount rate, the present value of distributable earnings remains constant. Though you’ll notice that earnings retained for growth continue to increase in dollar terms (at the same 10% rate).

What we end up with is a present value of the first ten years of cash flows of $8.6 billion. We can also clearly see that we’ve retained $6.5 billion over that period of time to fund growth in earnings. If we hadn’t, all things being equal, earnings would still be $1.349 billion as in the no growth scenario. Instead, earnings at year 10 are $3.181 billion. It’s from this base that we’ll calculate our terminal value.

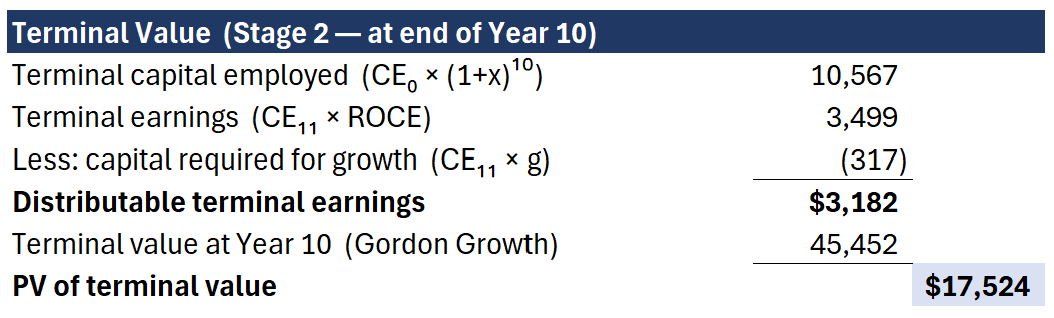

What is the value of the mature business at Year 10?

Quick math note: The terminal earnings we use in the table above are the year 11 earnings, which come from the year 10 ending capital x our return on capital.

Growth capital is lower (i.e., distributable earnings are higher) because we’re assuming a lower terminal growth rate, in this case 3%.

The distributable terminal earnings of $3.2 billion get capitalized at 7% (10% discount rate minus 3% growth rate) = $45.4 billion and then discounted back to today = $17.5 billion.

Putting It All Together

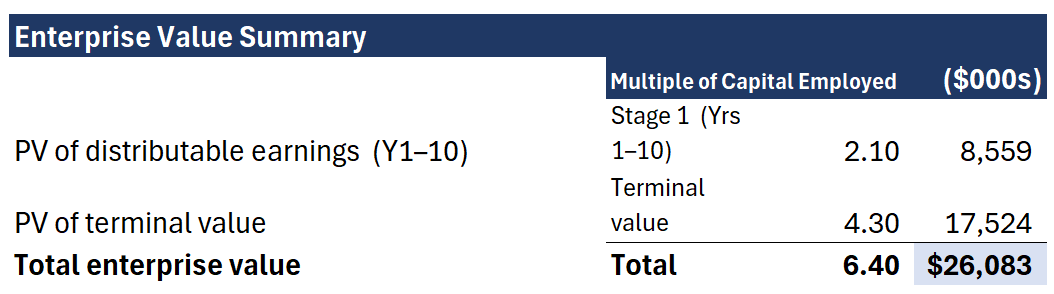

So now we have two numbers:

$8.6 billion: value of Years 1 to 10

$17.5 billion: value of Years 11 to forever

Together, they equal $26.1 billion, our present value estimate of Copart’s intrinsic value.

We can see that growth added $26.1 billion - $13.5 billion = $12.6 billion of value. That growth came from deferring capital equal to 10% of capital employed each year, or 10% / 33% = ~30% of earnings each year in the first decade, plus about 9% of earnings forever ($317 / $3,499) in the terminal growth.

Final Thoughts

This simplified model still suffers from the basic ailment of all models. Namely, its assumptions.

How did I calculate capital employed?

How did I choose which sustainable ROCE to use?

Is the initial growth period appropriate?

Can the company actually reinvest that amount of capital?

Is the terminal growth rate appropriate?

It also doesn’t account for structural changes as the business matures. What happens if competition or market saturation erodes returns or growth? Will return on capital change (+ or -) when the company matures?

You could certainly take this model and tweak any number of assumptions and add any level of detail you want.

Though what’s reassuring is that such a complex model probably wouldn’t get you much of a different estimate of intrinsic value. The complexity might look impressive (and who doesn’t like a good spreadsheet?), but it could come at the cost of either making a mistake in building it or data entry, or in the time you could spend thinking about various aspects of the business.

In my view, the big questions such as how the business develops, how much capital can be reinvested and at what return, and how long can that growth be sustained, get you 95% of the way there.

As I said last week:

The real value isn’t in having a high-powered calculator to spit out a number. Instead, it’s thinking through each part, reasoning based on what you’ve learned about the company and what seems reasonable, and considering the magnitude of each component and the risks of it getting disrupted.

Let me know what you think about this approach. Is it clear enough? What’s not so clear? What did I get wrong?

Hit reply, leave a comment, or shoot me an email.

More thoughts? Let me know in a private message or leave a comment.

Stay Rational!

Adam

Pre-Order the 2nd Edition Now!

Amazon, Barnes & Noble, or directly from Harriman House, and at other major bookstores, for delivery in April 2026.

Praise for the 2nd Edition

I’m incredibly grateful for the people who took the time to review early drafts of the new material and provided feedback, as well as praise for both editions:

“If you want to understand how Warren Buffett built Berkshire Hathaway into one of the most valuable businesses in the world, you have to read this book. This is your opportunity to stand beside Picasso as he paints each brush stroke. A must read for all Buffett and Berkshire groupies.”

- Bill Ackman, Founder and CEO of Pershing Square

“I and my teammates at the Gabelli Organization have been tracking Warren’s success for some 50 years. Adam’s book captures the work and highlights the history of Berkshire and the hard and diligent work of Buffett and Munger, Jain and Abel, and Combs and Weschler.”

- Mario Gabelli, Chairman and CEO, Gabelli Funds

“Adam Mead’s discussion of the values and virtues which have shaped Berkshire Hathaway over 50 years is a must read for those investors in search of the forces that have delivered such investment value over time.” – Thomas A. Russo, Gardner Russo & Quinn LLC

“Few activities can be more rewarding for any value investor than studying the history and evolution of Warren Buffett and Berkshire Hathaway. Adam has done us a huge favor with his yeoman efforts in producing this treatise. Since it is chronologically ordered, it is an invaluable reference guide for all things Berkshire.” — Mohnish Pabrai

“Adam continues to deliver a resource very valuable to both Berkshire fans and the investor community as a whole, his depth of knowledge is clearly demonstrated here again. I thoroughly enjoyed this latest addition.” - Dan Calkins, Chairman & CEO, Benjamin Moore

“The question must be asked, ‘Why another Berkshire book?’ When you read this monumental effort by Adam Mead, the answer will be obvious. Read cover to cover, both the uninitiated to Berkshire and its most ardent followers will derive enormous utility and satisfaction from it. I learned so many new and important things about Berkshire and its history. It is my pleasure to encourage you to enjoy this gem.”

- Christopher P. Bloomstran

“Whatever Adam writes is always first-class - guaranteed.

-Andy Kilpatrick, Author, Of Permanent Value: The Story of Warren Buffett

This is essentially a 2-stage DCF model.

Is valuing Copart’s no growth earnings as a perpetuity sufficiently conservative? Much of the value is implicitly after year 20 and there are valid terminal value risks to any business. For copart, this may manifest in AVs.

good stuff.

am hoping for a simplified (updated?) public version of why ~10% discount on EV is very exciting.

(+ ceo change !)