Growth Thoughts

Deeper thinking on a concept central to value.

Growth plays a big part in the calculation of value. Yet I see many people using the concept loosely and without tying it to return on capital and reinvestment.

Scenario 1: Earnings Capitalized - No Growth

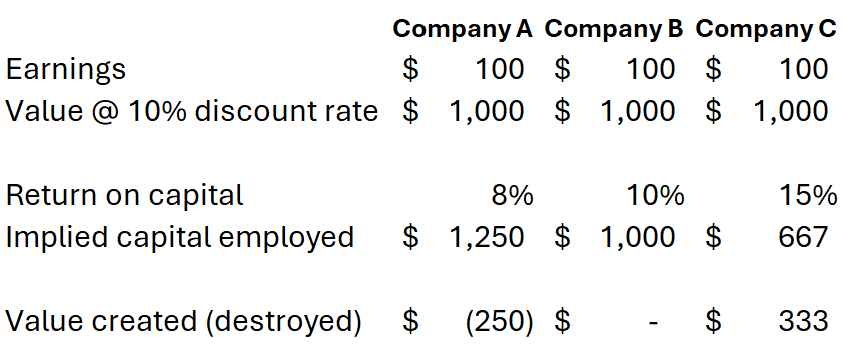

Question: What is the value of a $100 stream of earnings capitalized at 10%?

Answer: Not surprisingly, the values are all the same.

Now, does it matter what the underlying return on capital is for each company?

If the company isn’t going to grow and will distribute all of its earnings, then no, it doesn’t matter.

This example assumes that each company continues in perpetuity. Sometimes that’s the case, but there are going to be pressures on Company A and C for different reasons.

Company A should be liquidated, and its capital returned to shareholders.

Company B is earning its cost of capital

Company C is earning above its cost of capital. Keeping it in existence or, better yet, growing it, will add economic value.

Two Ways to Grow

There are two ways a company can grow and add value:

Margin expansion. A discrete or limited event

Reinvestment > cost of capital. Which depends on:

Amount reinvested

Duration of investment period

Margin Expansion

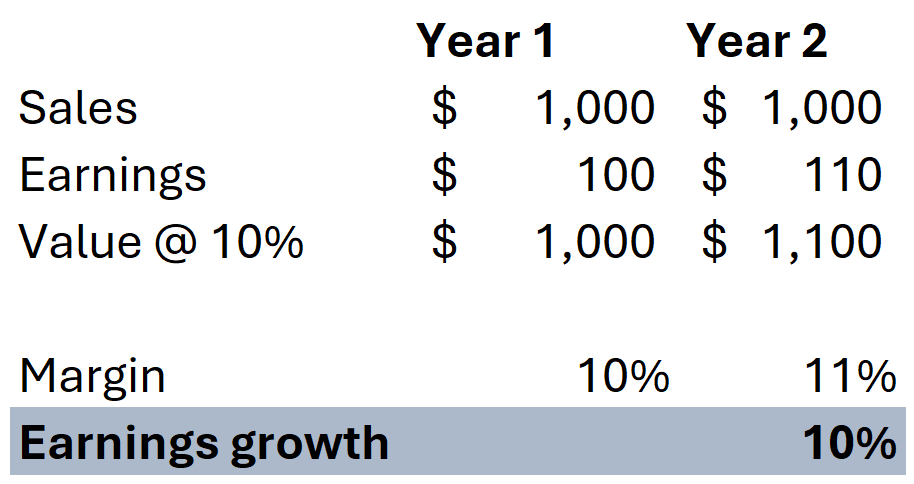

Here we have a company whose earnings increased by 10% by expanding margins. Sales remained unchanged. Invested capital (not shown) remained the same, and return on capital increased, too.

It may be selling more units at a higher price or (more likely) it found efficiencies and conducted the same amount of business at lower costs.

In either case, while this growth is real, it can’t go on forever. For earnings to grow by 10% in Year 3, all things being equal, it will need to increase its margin again.

If this new margin profile is sustainable, then the growth added 10% to the value of the firm. This is not recurring growth unless margins can keep expanding. It is a one-time step-up in earnings power.

Growth By Retained Earnings

“This company has earnings of $100 and will grow at 5% per year in perpetuity. Therefore, it is worth 20x earnings or $2,000.”

We now enter fuzzy thinking territory. I see too much bandying about of growth rates without digging into what they imply.

The question must be asked: How will the company grow?

Most businesses require capital to grow. You can’t have your earnings and grow, too (aside from the margin scenario above).

Where does the capital come from? If sustainable, then it must come from earnings.

How much earnings must we give up for that growth? It depends on the return on capital.

A company earning 10% ROC must retain 50% to grow at 5% (5% / 10%)

A company earning 20% ROC must retain 25% to grow at 5% (5% / 20%)

A company earning 25% ROC must retain 20% to grow at 5% (5% / 25%)

At 50% ROC, a company only needs to retain 10% of earnings to grow at 5%

Now invert these figures. It’s obvious but not discussed enough: The higher the return on capital, the more earnings can be distributed while growing.

The Crucial Questions for the Analyst

How much capital can be reinvested in the business?

For how long?

Will the return on capital change along the way?

Assume:

Capital employed of $1,000

Return on capital of 25%

Earnings are then $250

How much is this company worth (at 10%)?

No growth scenario = $250 / 10% = $2,500

5% perpetual growth = $1,000 capital x 5% = $50 retained.

$250 earnings less $50 = $200 distributable earnings.

$200 / (10% - 5%) = $4,000.

Growth has added $1,500 of value. But that value is not free. It required retaining $50 of annual earnings, or 20% of earnings, because the business earns 25% on capital.

10% growth for 10 years, then no growth = 10%/25% = 40% retention required.

$250 x 60% = $150 distributable earnings

Using a simplified convention, because distributions grow at the same rate as the discount rate, each year’s distribution contributes roughly the same present value. So ten years of distributions contribute about $1,500.

Terminal value = $250 at 10% growth, discounted at 10% means Y10 earnings in present value terms will be $250 / 10% = $2,500.

$1,500 + $2,500 = $4,000. Growth has added $1,500 of value.

Scenarios 2 and 3 illustrate that the value of growth depends on both rate and duration. In this simplified example, a ten-year burst of 10% growth produces the same value as 5% perpetual growth.

The analyst’s job is to determine how much capital can be reinvested, what return that reinvestment can earn, and how long the opportunity can last. High-return growth is powerful because it consumes less cash. Low-return growth may consume all the earnings and add little or no value.

Growth creates value when capital can be reinvested above the cost of capital, in meaningful amounts, for a meaningful period of time.

The analyst’s job is to “print the coupons,” to quote Buffett.

More thoughts? Let me know in a private message or leave a comment.

Stay Rational!

Adam

Pre-Order the 2nd Edition Now!

Amazon, Barnes & Noble, or directly from Harriman House, and at other major bookstores, for delivery in April 2026.

Praise for the 2nd Edition

I’m incredibly grateful for the people who took the time to review early drafts of the new material and provided feedback, as well as praise for both editions:

“If you want to understand how Warren Buffett built Berkshire Hathaway into one of the most valuable businesses in the world, you have to read this book. This is your opportunity to stand beside Picasso as he paints each brush stroke. A must read for all Buffett and Berkshire groupies.”

- Bill Ackman, Founder and CEO of Pershing Square

“I and my teammates at the Gabelli Organization have been tracking Warren’s success for some 50 years. Adam’s book captures the work and highlights the history of Berkshire and the hard and diligent work of Buffett and Munger, Jain and Abel, and Combs and Weschler.”

- Mario Gabelli, Chairman and CEO, Gabelli Funds

“Adam Mead’s discussion of the values and virtues which have shaped Berkshire Hathaway over 50 years is a must read for those investors in search of the forces that have delivered such investment value over time.” – Thomas A. Russo, Gardner Russo & Quinn LLC

“Few activities can be more rewarding for any value investor than studying the history and evolution of Warren Buffett and Berkshire Hathaway. Adam has done us a huge favor with his yeoman efforts in producing this treatise. Since it is chronologically ordered, it is an invaluable reference guide for all things Berkshire.” — Mohnish Pabrai

“Adam continues to deliver a resource very valuable to both Berkshire fans and the investor community as a whole, his depth of knowledge is clearly demonstrated here again. I thoroughly enjoyed this latest addition.” - Dan Calkins, Chairman & CEO, Benjamin Moore

“The question must be asked, ‘Why another Berkshire book?’ When you read this monumental effort by Adam Mead, the answer will be obvious. Read cover to cover, both the uninitiated to Berkshire and its most ardent followers will derive enormous utility and satisfaction from it. I learned so many new and important things about Berkshire and its history. It is my pleasure to encourage you to enjoy this gem.”

- Christopher P. Bloomstran

“Whatever Adam writes is always first-class - guaranteed.

-Andy Kilpatrick, Author, Of Permanent Value: The Story of Warren Buffett

“With this project, Adam has done a wonderful job extending the Berkshire Classroom by providing a comprehensive analysis of the rich corporate history and unique entrepreneurial leadership.” — Mac Sykes, Gabelli Funds

“Adam Mead’s The Complete Financial History of Berkshire Hathaway is the definitive history of Berkshire. While there have been countless books written about Warren Buffett’s investment approach, none have so meticulously documented Berkshire’s capital allocation decisions from the very beginning. The depth of research is staggering, transforming the complex and sometimes chaotic story of how a small textile mill became a financial conglomerate into a clear, year-by-year narrative of every significant investment and acquisition. In this updated edition, Adam carries the narrative through Berkshire’s sixth decade and the methodically planned leadership transition to Greg Abel. For students of business history, this is an indispensable resource.”

-Patrick Gaughen, President and Chief Operating Officer, Hingham Institution for Savings

“The definitive story of Berkshire Hathaway—how Buffett and Munger turned a failing textile mill into one of history’s greatest wealth-creating enterprises, with timeless lessons in business, investing, and leadership.”

-Vitaliy Katsenelson, CEO of IMA, Author of Soul in the Game

“Berkshire Hathaway is a company with few, if any, parallels in business history. Under the leadership of Warren Buffett, it was transformed from a New England textile mill that would ultimately be shuttered to a sprawling conglomerate with a market valuation of more than $1 trillion. With this updated edition of “The Complete Financial History of Berkshire Hathaway”, Adam provides a thorough review of the key decisions that created the modern Berkshire Hathaway, an outcome inextricably tied to the investment and business wisdom of Warren Buffett and his business partner, Charlie Munger. In a few hundred pages, Adam adeptly runs through six decades of Berkshire’s history. For Buffett and Munger fans who want to truly understand how Berkshire was created, this book is a must read.”

- Alex Morris, Founder of TSOH Investment Research and the Author of Buffett & Munger Unscripted

“A meticulous chronicle of Berkshire Hathaway’s remarkable final act under Buffett’s leadership. Mead’s granular analysis of Buffett’s capital allocation decisions—from the $78 billion in share repurchases to the masterful Apple investment—provides unmatched insight into how the world’s most successful conglomerate navigated unprecedented scale and succession challenges.”

-Tobias Carlisle, Portfolio Manager, Acquirers Funds®

“This exceptional history of Berkshire Hathaway will appeal to history buffs, finance enthusiasts, and investing professionals alike. Mead combines rigorous research with remarkably clear storytelling, tracing the company’s ascent from a struggling textile mill to one of the world’s most admired conglomerates. The book is impressively detailed yet fully accessible—equally valuable for students learning the foundations of investing and for seasoned professionals looking to deepen their understanding of Berkshire’s evolution.”

-Gillian Zoe Segal

“With his ability to make complex things seem simple, Warren Buffett made the difficult work of building Berkshire Hathaway look easy. With this excellent history, Adam Mead takes us behind the scenes to see the details of how that work happened and was so successful. For anyone interested in Berkshire Hathaway, or the development of American capitalism, this is essential reading.”

- Bryan Lawrence, Founder, Oakcliff Capital

“There is simply no book that details the economic lore of Berkshire Hathaway better. A true exposé that every intelligent investor should read.”

- Gwen Hofmeyr, Founder, Maiden Financial

“The most comprehensive book on Berkshire Hathaway that has ever been written. It belongs on the shelf of every business enthusiast!”

-Andrew Wagner, Author of the Economics of Online Gaming and Founder & Chief Investment Officer of Wagner Road Capital Management

“Adam’s accounting of the Financial History of Berkshire is like candy for Finance and Business Junkies alike. It’s a must read if you’re interested in studying the greats.”

- Carter Johnson, Managing Partner, Singleton Valuations

“I thought nothing else of value could be written about Warren Buffett. I was wrong. Adam’s detailed chronology of Berkshire’s evolution reveals the successes and failures of Warren in a unique and digestible way. A worthwhile read for every Buffett scholar, amateur and professional alike.” — Drew Estes, Banyan Capital

“Mead has done the Berkshire faithful an incredible service by stitching together the narrative and numbers so tightly, you can see the compounding in action—updated and genuinely useful.”

-Jacob Taylor, CEO of Baserate

“Adam Mead’s work reminds us that true value is found not just in numbers, but in the lasting quality where few care to linger. By doing exceptional due diligence his book clones the lessons of Warren and Charlie.”

-Jeff Gilbert

Adam Mead’s updated “Complete Financial History of Berkshire Hathaway” is a book like no other—chronicling six decades of evolution while reminding us that Berkshire, though Buffett’s masterpiece, remains subject to constant change—an indispensable addition to any serious investor’s bookshelf.

-Bogumil Baranowski, Founder of Blue Infinitas Capital, Author of “Money, Life, Family”, Host of Talking Billions Podcast

Great article.