The Value Bridge: Zooming In on Copart's Growth

Getting beyond a simple framework using Copart as a real-world example

Going Deeper On Growth

In a prior post, I examined growth as a concept: How it adds value, and the different ways companies can grow (i.e., margin expansion and/or reinvestment via retained earnings).

Here, I go deeper and present a framework for thinking about the sources of growth embedded in our assumptions using a real-world example of Copart (Disclosure: Long).

The “Standard” Approach

The typical approach of taking the current earnings yield + growth = holding return isn’t wrong. It’s just consolidating a whole bunch of assumptions. I want to take apart those assumptions and examine them in greater detail.

Copart

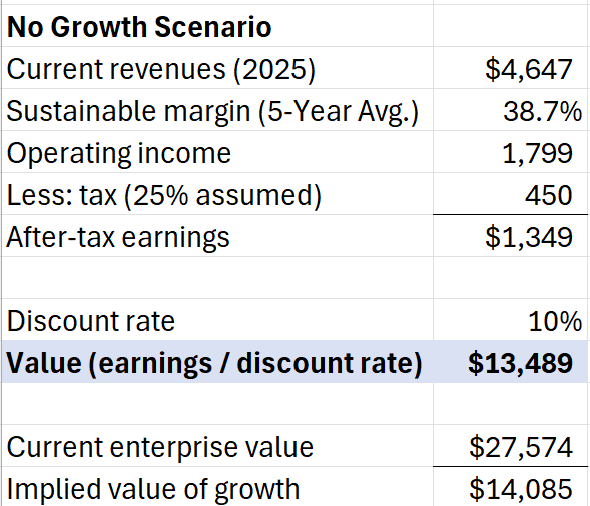

No Growth Scenario

The Base scenario is no growth.

I’m making certain assumptions, which you can agree or disagree with, but the basic logic is sound.

Here we arrive at a sustainable level of earnings, which are assumed to be distributable and distributed. At a 10% discount rate, it’s worth $13.5 billion.

We can say, then, that the market is pricing in $14 billion of additional value. But how, and when, does that value happen?

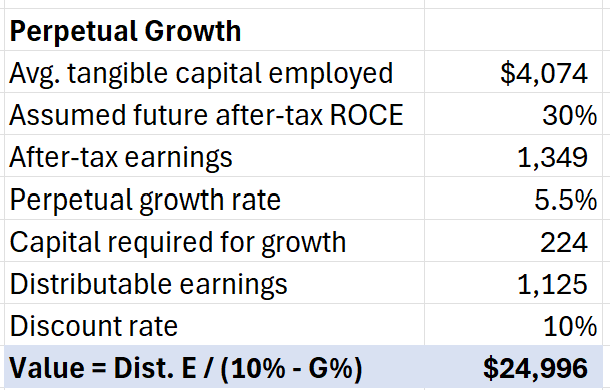

Perpetual Growth

This analysis shows that Copart must grow 5.5% forever to justify its current price. Note that the model deducts the capital required for that growth.

You can’t have your cake (growth) and eat it (distribute it) too!

The problem is that companies don’t grow at a linear rate forever. A typical growth pattern has a period of growth followed by slowing or sustained growth thereafter, perhaps (gasp!) followed by a period of decline.

Disaggregated Growth

I think it’s worth going deeper and thinking about the components of growth. Here I’m guided by the excellent work of Bruce Greenwald in Value Investing: From Graham to Buffett and Beyond, 2nd Ed.

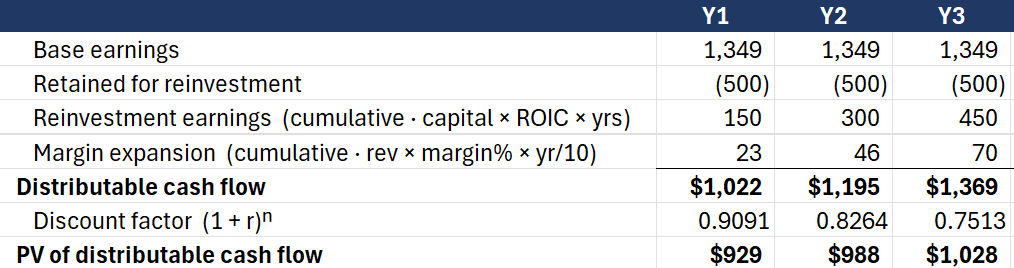

A few things are going on here, so I’ll break them down:

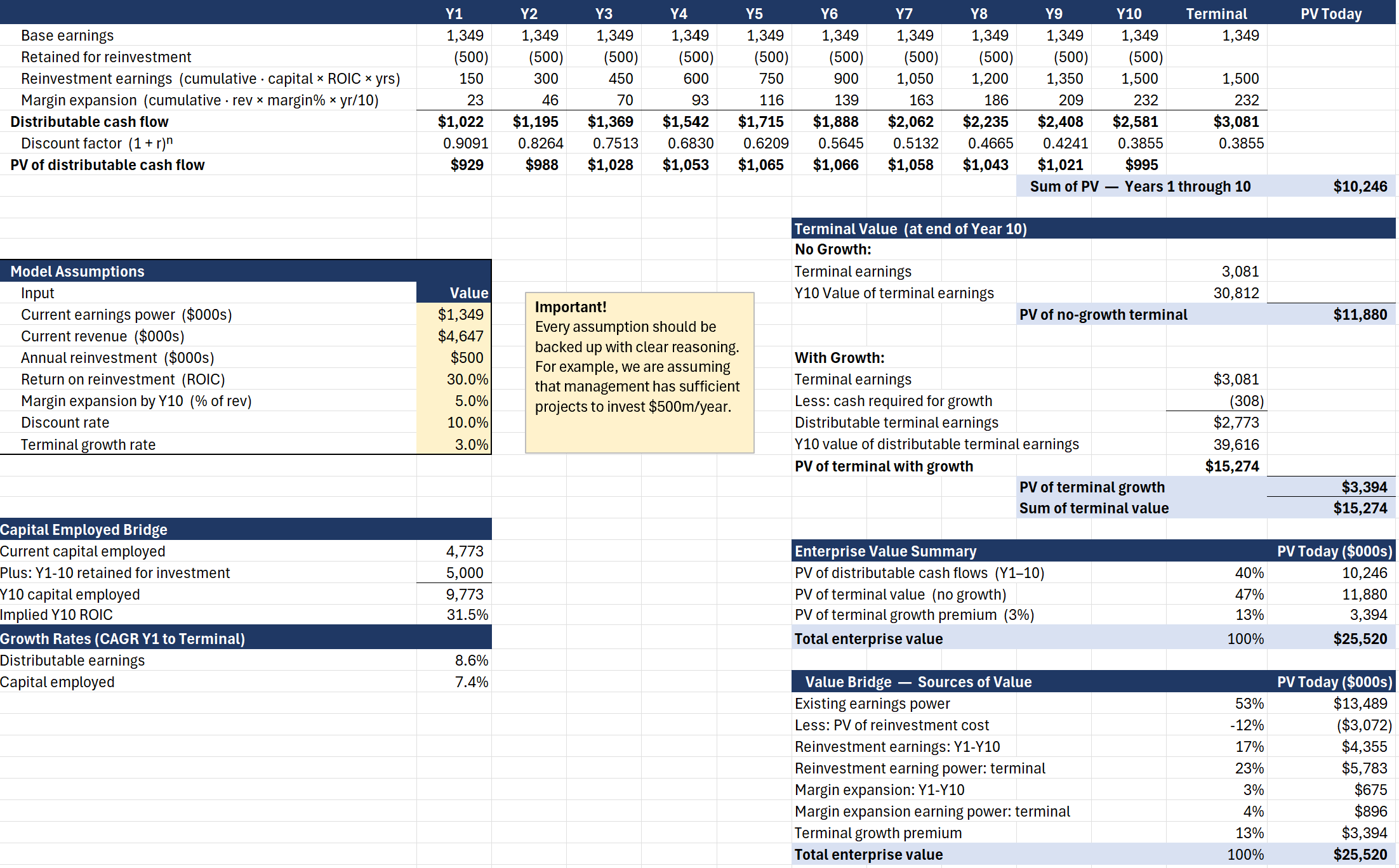

We start with the base earnings, the same $1,349 million from above.

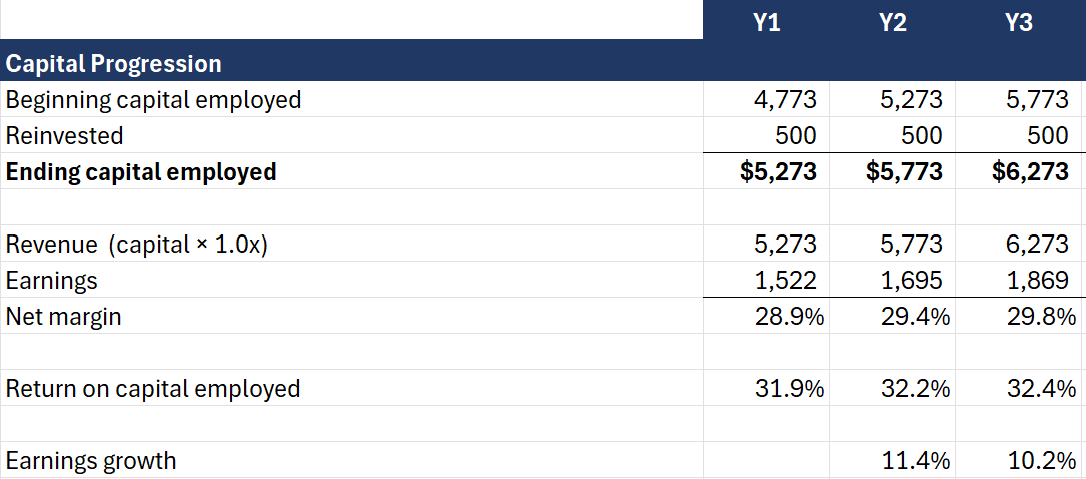

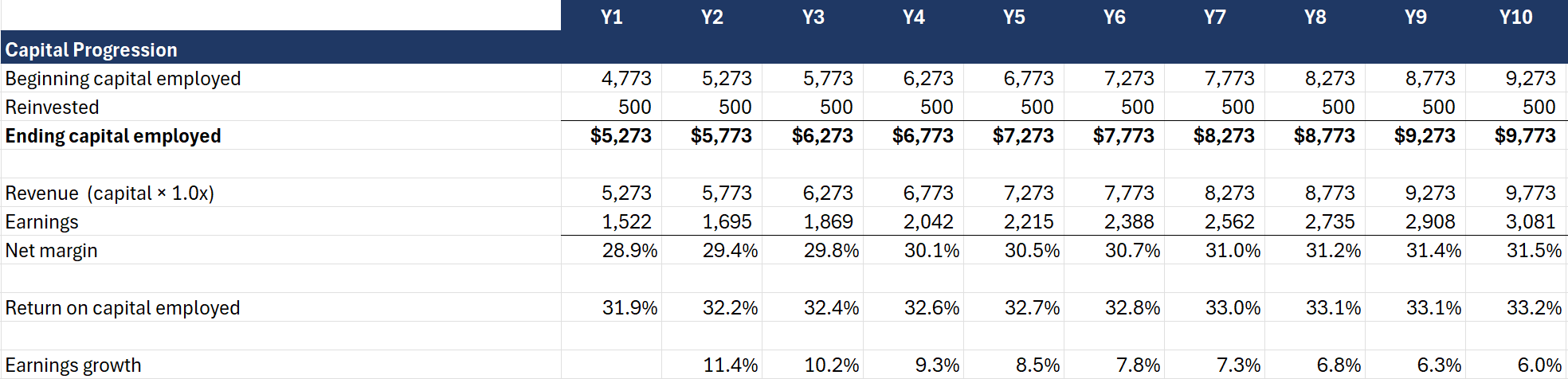

I’m assuming the company can retain $500 million a year in growth capex (depreciation = maintenance capex is already in earnings). See the capital progression table below to follow the effect on capital employed.

From that investment, I’m assuming the company can earn 30% after-tax, which is based on historical performance.

Finally, I’m also assuming the company will expand its operating margin by 5 percentage points over ten years, or 50bps/year. This assumption is rooted in continued economies of scale in G&A expense in the US (again, proven by historical figures), and improvements in international margins.

The whole 10 year progression looks like this:

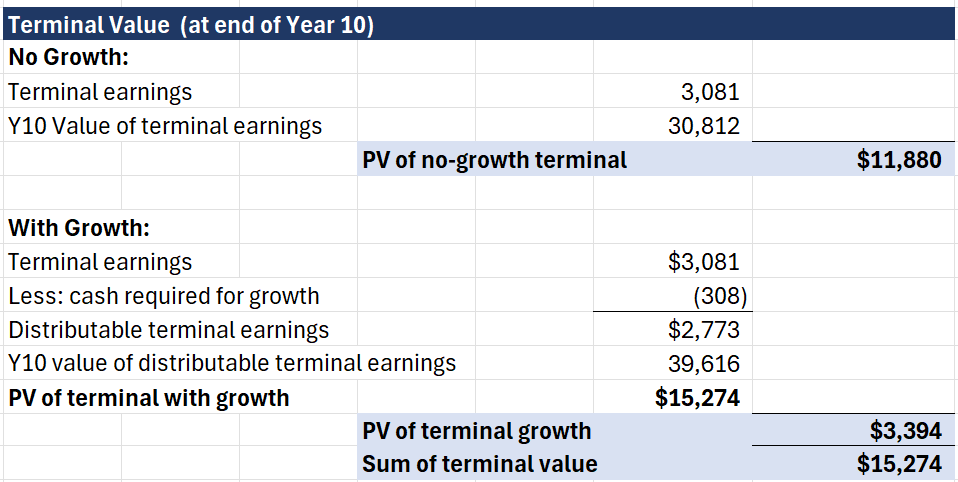

We then have to decide what to do with the terminal value. We can either assume no growth or some sort of Y11-forever perpetual growth. With this model, we can see what that looks like.

No growth: Adds $11.9 billion to the present value, resulting in a value of $10.2b + $11.9b = $22.1b.

Perpetual 3% growth: Adds $3.4b for $15.3b total terminal value or $25.5b total.

The summary looks like this:

Taking It Apart Further:

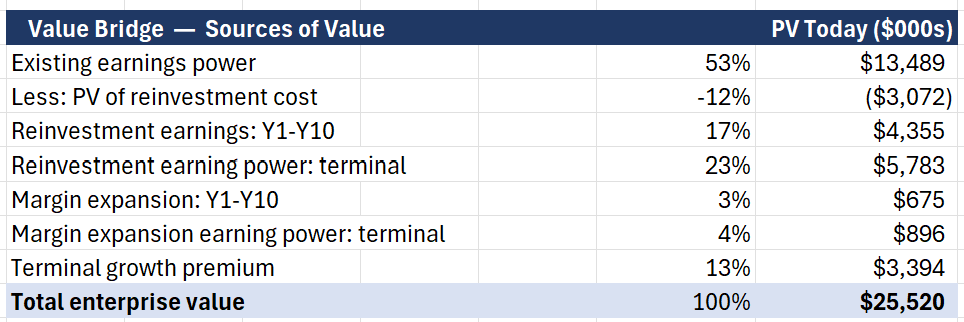

But we can go deeper and examine all of the sources of value in what I’m calling a value bridge.

The value bridge shows you exactly where growth adds value.

Existing earnings power is about half of the value

Growth requires investment, and that comes in the form of deferred current distributions totalling almost $3.1b on a present value basis.

However, Reinvestment adds $4.3b of present value.

Then another $5.8b of reinvestment value comes from the terminal value

We can also see the effect of margins, not only on the Y1-Y10 cash flows but also on the terminal value.

Finally, the impact of the terminal growth rate is shown, here $3.4b.

A Work In Progress

While I agree with Greenwald that DCF models, in general, do more harm than good (combining good current info with poor future info), the mechanics of growth require an expansion of assumptions to view each component in its proper context. You can call it a DCF model if you like; I don’t think it’s quite what Wall Street considers one.

The real value isn’t in having a high-powered calculator to spit out a number. Instead, it’s thinking through each part, reasoning based on what you’ve learned about the company and what seems reasonable, and considering the magnitude of each component and the risks of it getting disrupted.

Even if imperfect, at the very least, we’re able to take apart the growth equation and move beyond “grow at an average of 5.5% forever” to a more robust view of the parts and their timing.

Let me know what you think about this approach. Is it clear enough? What’s not so clear? What did I get wrong?

Hit reply, leave a comment, or shoot me an email.

Here’s the full model:

More thoughts? Let me know in a private message or leave a comment.

Stay Rational!

Adam

Pre-Order the 2nd Edition Now!

Amazon, Barnes & Noble, or directly from Harriman House, and at other major bookstores, for delivery in April 2026.

Praise for the 2nd Edition

I’m incredibly grateful for the people who took the time to review early drafts of the new material and provided feedback, as well as praise for both editions:

“If you want to understand how Warren Buffett built Berkshire Hathaway into one of the most valuable businesses in the world, you have to read this book. This is your opportunity to stand beside Picasso as he paints each brush stroke. A must read for all Buffett and Berkshire groupies.”

- Bill Ackman, Founder and CEO of Pershing Square

“I and my teammates at the Gabelli Organization have been tracking Warren’s success for some 50 years. Adam’s book captures the work and highlights the history of Berkshire and the hard and diligent work of Buffett and Munger, Jain and Abel, and Combs and Weschler.”

- Mario Gabelli, Chairman and CEO, Gabelli Funds

“Adam Mead’s discussion of the values and virtues which have shaped Berkshire Hathaway over 50 years is a must read for those investors in search of the forces that have delivered such investment value over time.” – Thomas A. Russo, Gardner Russo & Quinn LLC

“Few activities can be more rewarding for any value investor than studying the history and evolution of Warren Buffett and Berkshire Hathaway. Adam has done us a huge favor with his yeoman efforts in producing this treatise. Since it is chronologically ordered, it is an invaluable reference guide for all things Berkshire.” — Mohnish Pabrai

“Adam continues to deliver a resource very valuable to both Berkshire fans and the investor community as a whole, his depth of knowledge is clearly demonstrated here again. I thoroughly enjoyed this latest addition.” - Dan Calkins, Chairman & CEO, Benjamin Moore

“The question must be asked, ‘Why another Berkshire book?’ When you read this monumental effort by Adam Mead, the answer will be obvious. Read cover to cover, both the uninitiated to Berkshire and its most ardent followers will derive enormous utility and satisfaction from it. I learned so many new and important things about Berkshire and its history. It is my pleasure to encourage you to enjoy this gem.”

- Christopher P. Bloomstran

“Whatever Adam writes is always first-class - guaranteed.

-Andy Kilpatrick, Author, Of Permanent Value: The Story of Warren Buffett

much thx for this breakdown. as a big fan of chris mayar, i hate these long periods where he is quiet.

some questions :

- why not use some statistical growth estimate, as you are using estimates based on past for other variables?

(if the 5.5% growth is expectations based on current shareprice, i missed that)

- have you considered the verdad framework where growth estimates are a coinflip, so they use less volatile statistical profits in modeling?