Berkshire Hathaway Deep Dive

The Abel era begins.

Let’s Talk Berkshire!

Join us on Friday, March 6th, at 1 pm ET to discuss Berkshire and more. Paid subscribers have the link to join the private Google Meet. Don’t miss it!

Subscribers can access the live Google Sheet here.

Prior posts on BRK

Disclosures: Long BRK

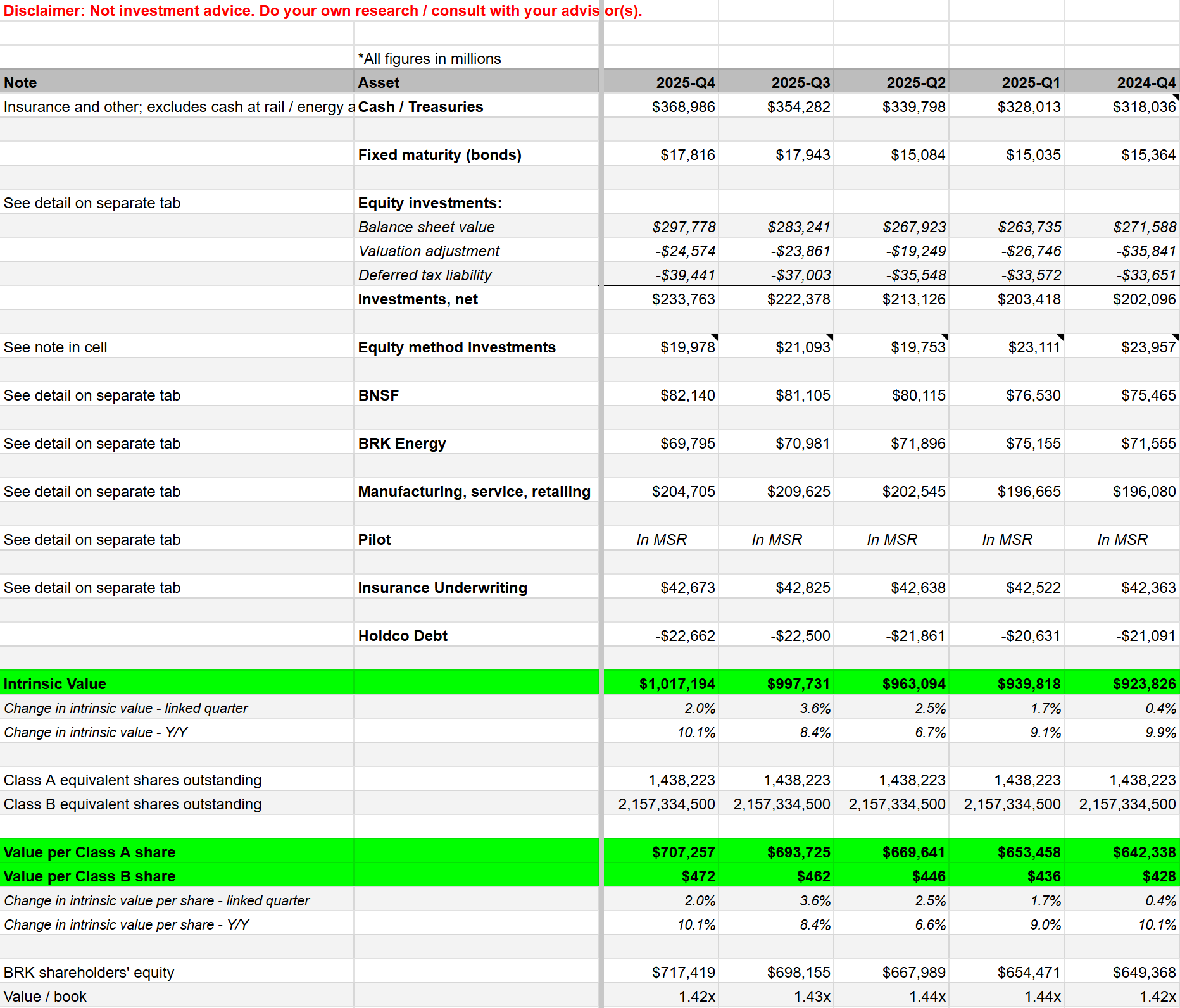

Sum-of-the-Parts Valuation

Berkshire is best valued using a sum-of-the-parts method. This approach hits the sweet spot between too much detail (you could just read the 154-page annual report for yourself) and the roughly right (but lacking) shorthand methods, such as applying a price-to-book multiple, or even Buffett’s own two-column method (see the 1995 Chairman’s letter), which adds per share investments to a multiple of per share operating earnings.

Berkshire is, of course, more than the sum of its parts, but that can be left as a qualitative factor. Berkshire’s stability demands less of a margin of safety, and the many reasons why it’s worth more together can be thought of as a margin of safety. It’s there, but you can’t put a precise figure on it. And that’s OK — welcome to the messy world of valuation.

Let’s dig in, considering Berkshire’s sources of value from its cash/treasuries, fixed maturity (bond) investments, marketable equity securities, its railroad, utilities, manufacturing and service businesses, and insurance. We’ll also adjust for debt at the holding company level and for a possible adjustment to BNSF’s valuation.

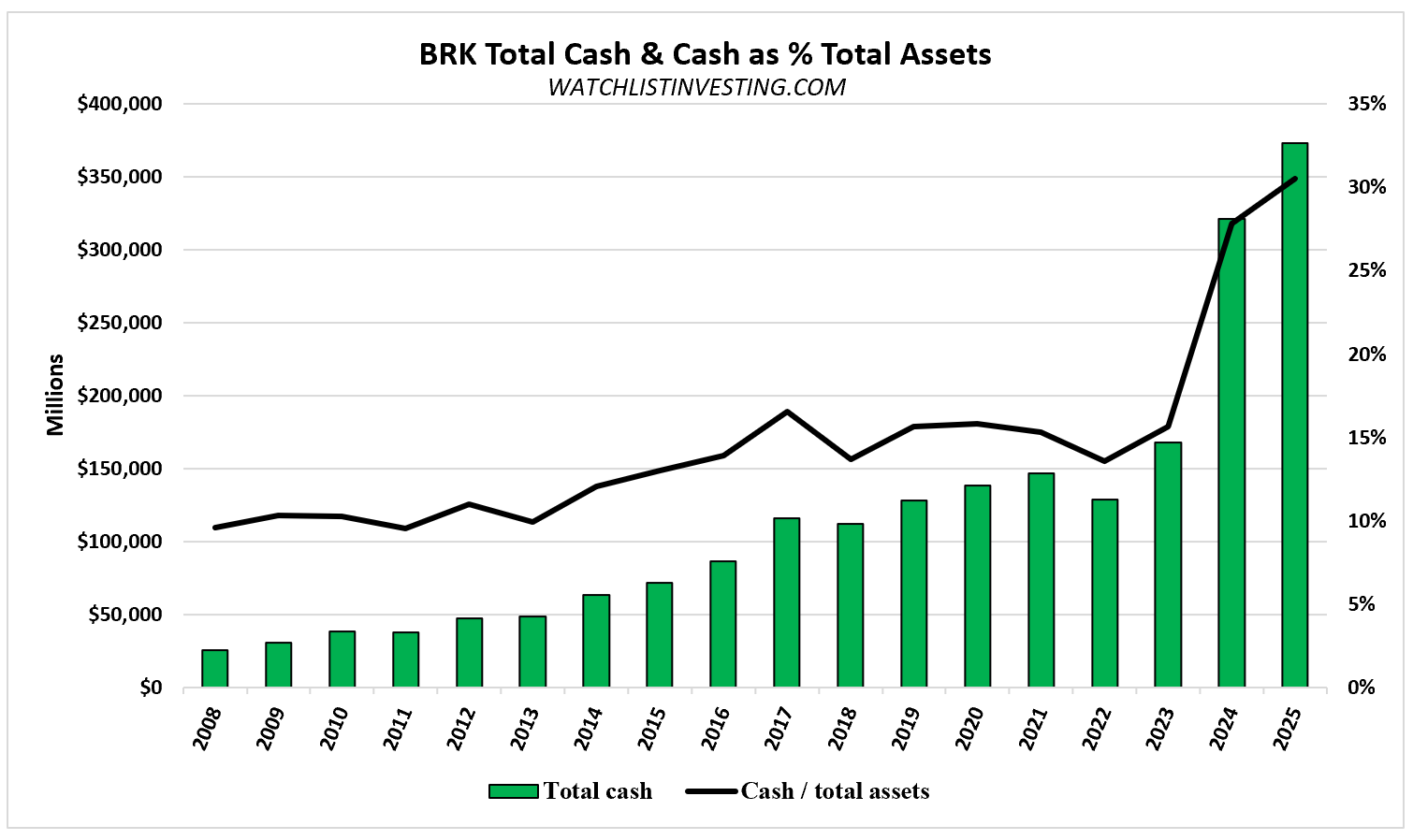

Cash

Simple, right? Not so fast.

Adding up ALL cash we get $373.1 billion. This is AFTER deducting $167 million payable for the purchase of US Treasuries. The figure is tiny now but amounted to almost $13 billion last year.

For valuation purposes, I use $368.99 billion, which excludes cash in the rail/utilities businesses. The rail sends its excess cash to Omaha ($4.4 billion last year) and needs what’s left, as do the utilities, which are continually investing in replacement and growth capex.

I consider all but about $50 billion real dry powder. That figure isn’t pulled from a hat. Rather, it’s the approximate amount of claims paid annually in the insurance business (see p. K-87). (One might argue the case that this should also be deducted from the value, as it’s permanently locked up.)

Fixed Maturity Investments

Berkshire keeps its maturities short and credit good, so this isn’t an area to spend much time (it’s also tiny in the grand scheme of things).

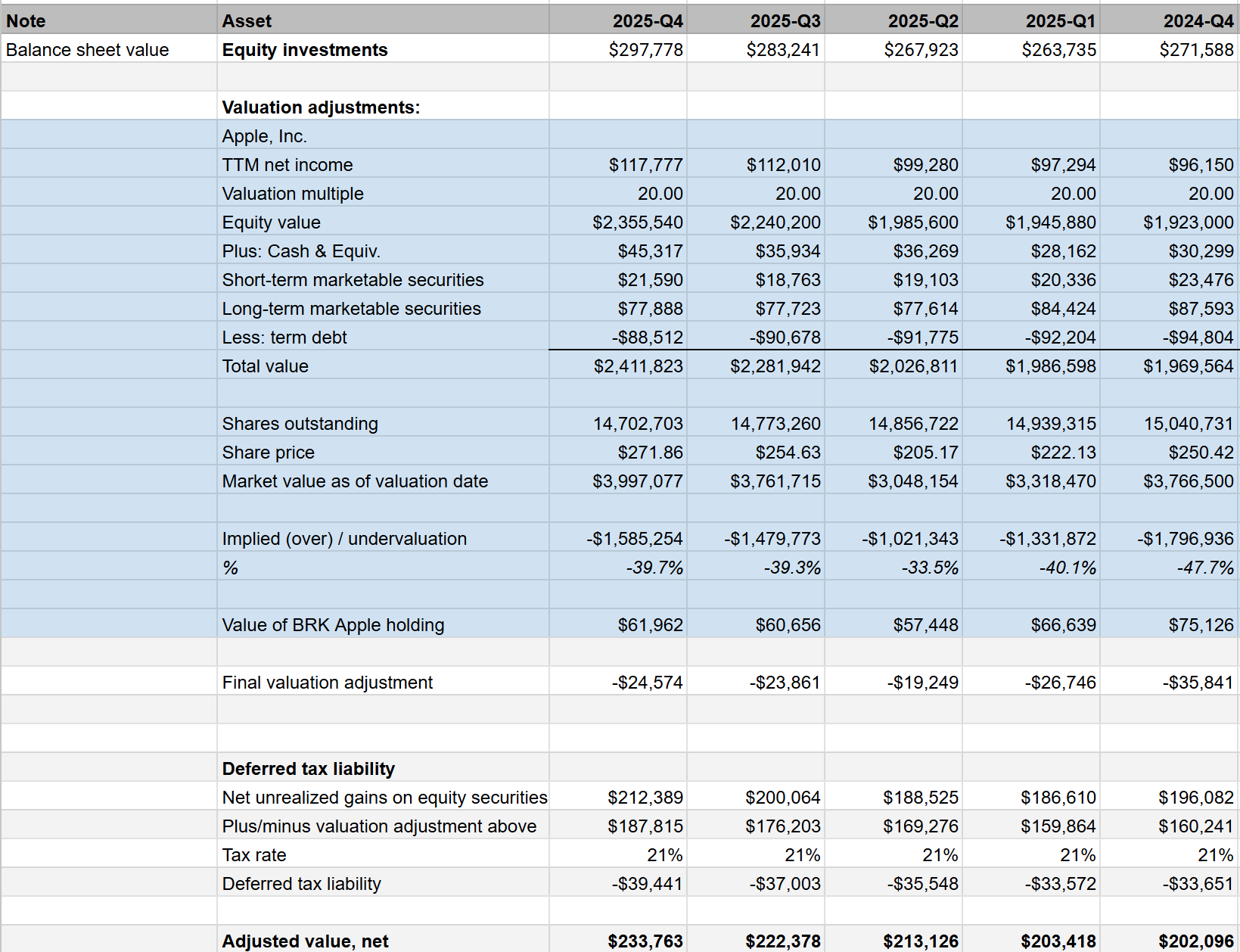

Equity Investments

I generally assume the equity portfolio is valued fairly unless an extreme case jumps out in one of the larger holdings. In recent years, that’s meant shaving something off for Apple’s apparent overvaluation.

I adjust Apple’s value to 20x earnings, add cash and marketable securities, and deduct debt.

I also deduct the deferred tax liability, which is adjusted to account for any valuation adjustments.

Berkshire was again a net seller of stocks in 2025.

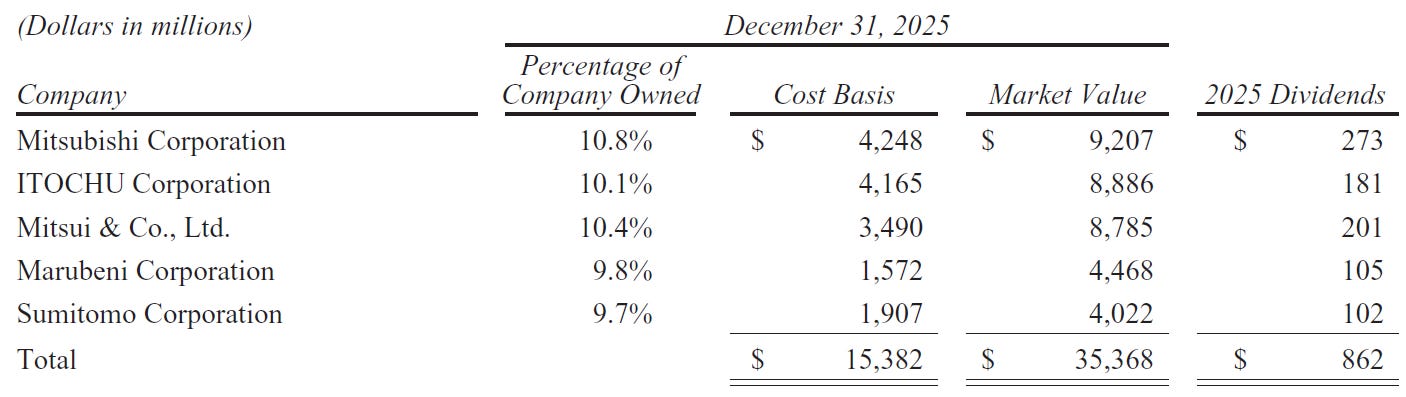

Greg Abel gave us a great snapshot of the Japanese equities portfolio, which is included above. Berkshire has funded these investments with $14.1 billion of Yen denominated debt at a mouthwatering 1.2% interest rate.

Equity Method Investments

Ownership between 20% and 50% requires equity method accounting, where the investee (BRK) must report a single line for its share of earnings and equity on its income statement and balance sheet, respectively.

The two major investments in this category are Kraft Heinz (27.5% ownership) with a fair value of $7.9 billion and Occidental Petroleum (26.9% excluding warrants) with a fair value of $10.9 billion. The third investment is a 50% ownership in Berkadia with a carrying value of $450 million.

For simplicity, I used the carrying values for all three. The difference between the carrying value and the fair value of KHC is $734 million. That’s primarily a result of a $5 billion pre-tax impairment charge taken in Q2 2025.

The Oxy carrying value matches the fair value on account of a $5.7 billion pre-tax impairment loss recorded at the end of Q4. Berkshire noted that the carrying value exceeded its share of Oxy’s shareholders’ equity by $3.4 billion — in other words, it’s trading at a premium to book value.

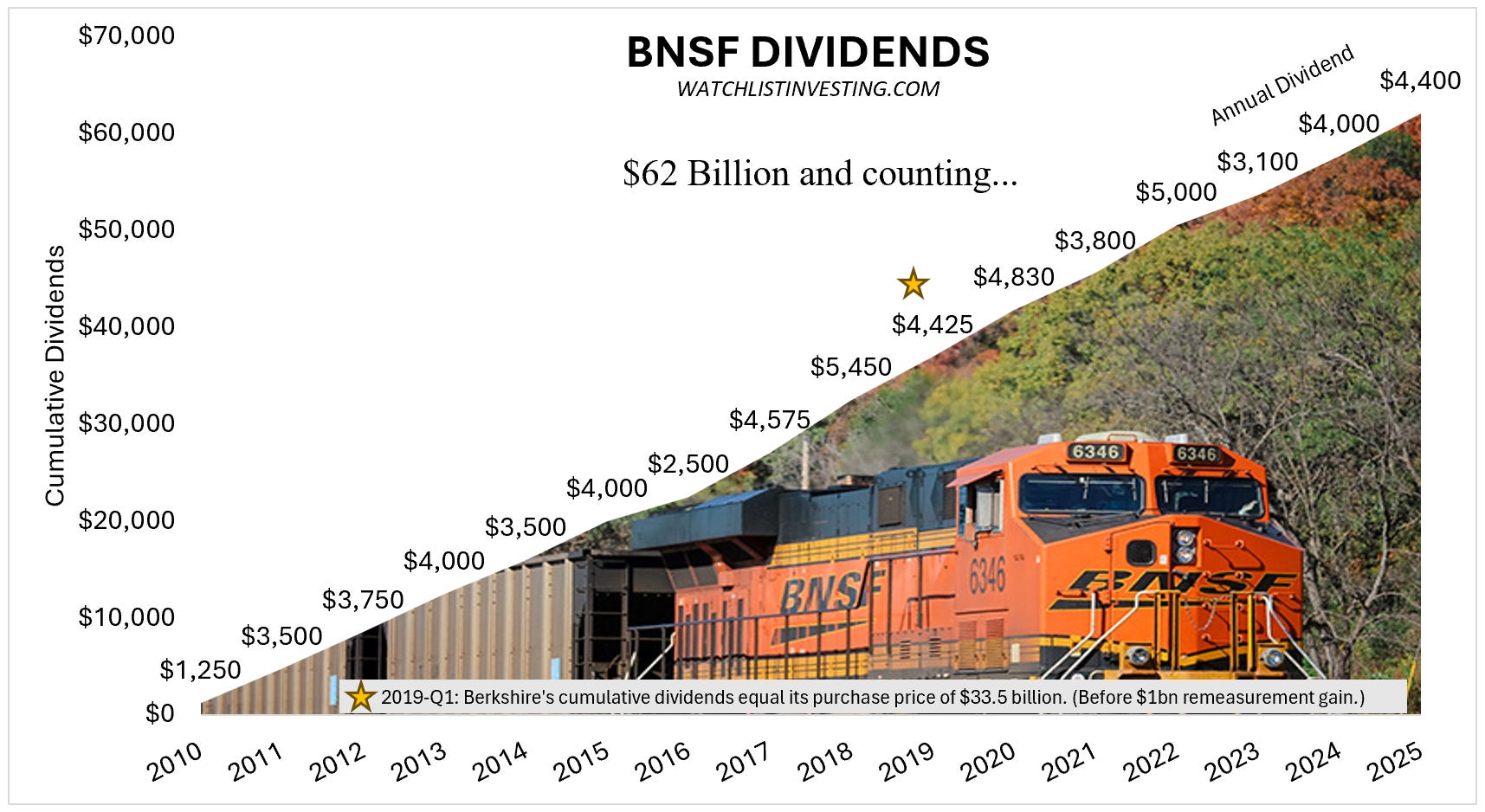

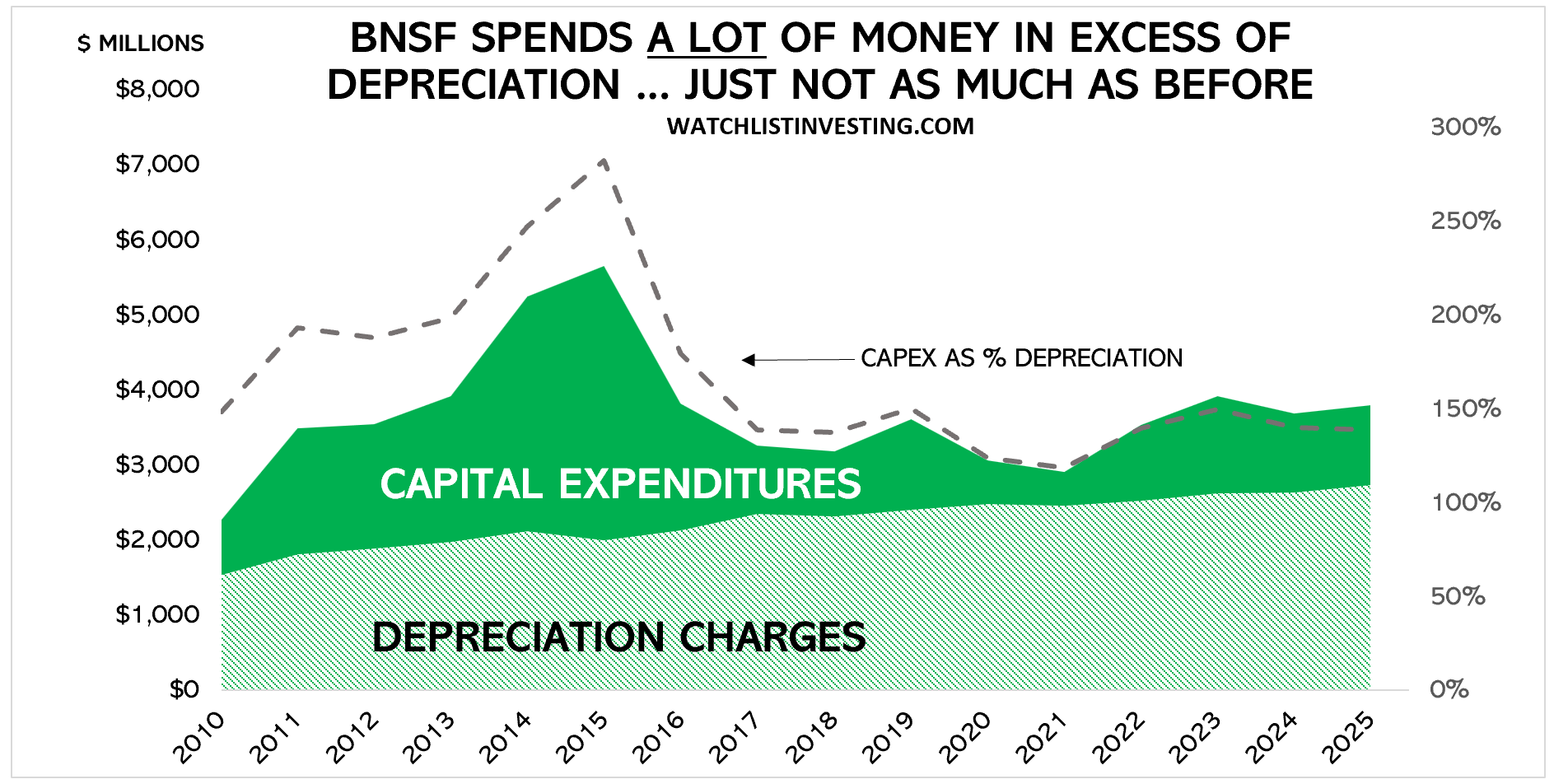

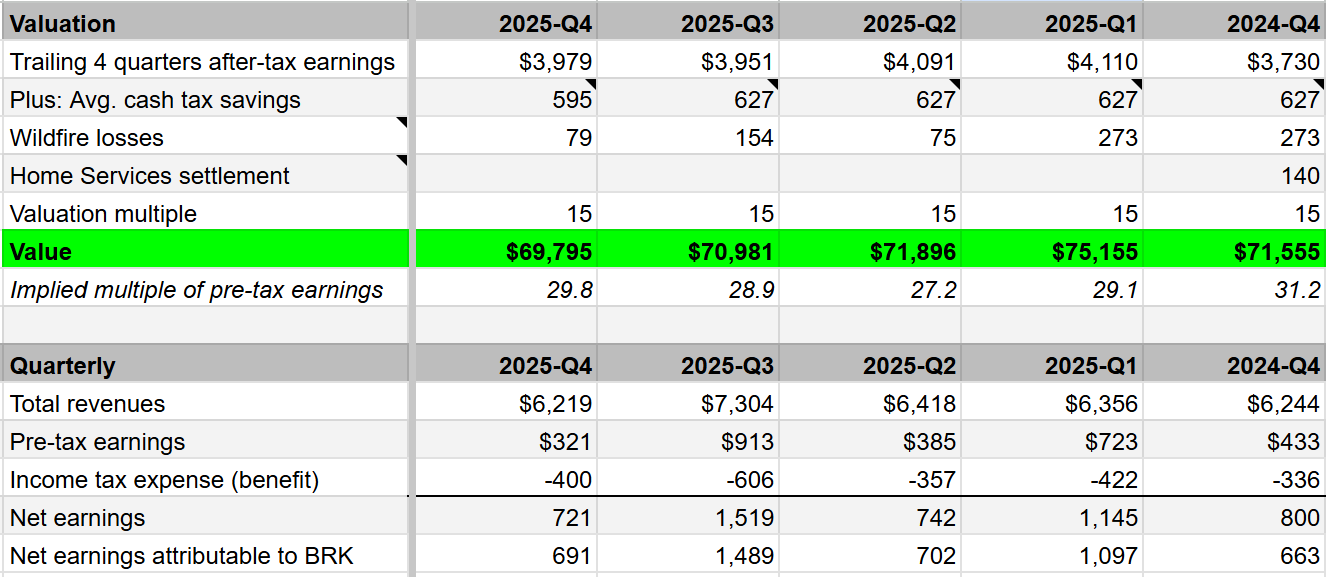

Burlington Northern Santa Fe

Berkshire Hathaway recouped its purchase price for BNSF in Q1 2019, nine years after purchasing the railroad for $33.5 billion. And the cash continues to pour in. $4.4 billion was sent to Omaha last year alone. This year (2026) should bring cumulative dividends to nearly 2x the purchase price.

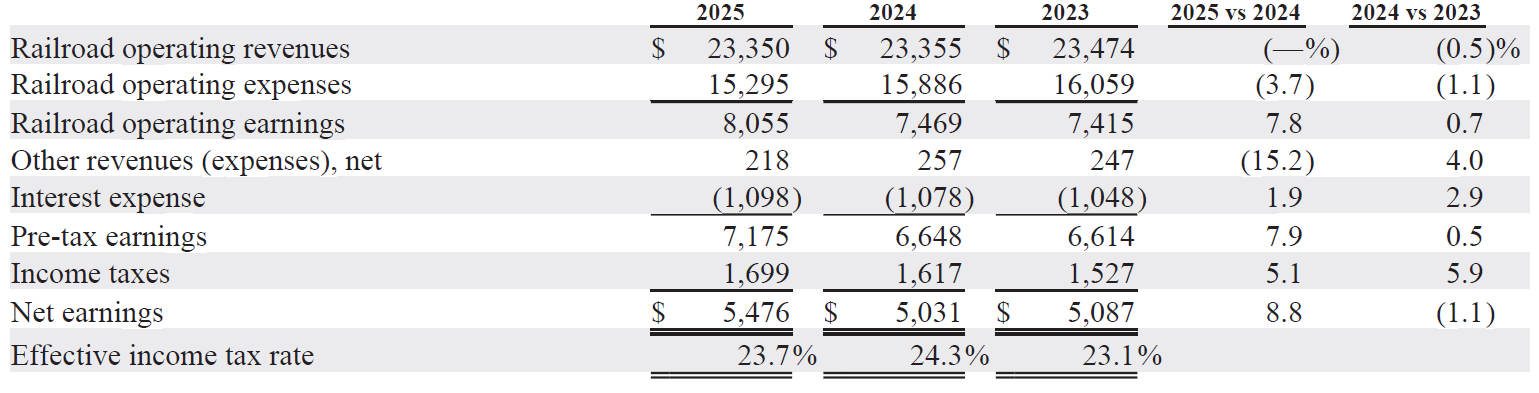

BNSF reported flat revenues on 30bps of higher volume and a half point decline in pricing.

Operating performance in 2025 improved compared to 2024, but BNSF still lags behind its main rival, Union Pacific. UNP’s operating margin (EBIT) was 40.2% in 2025 compared to BNSF’s of 34.5%. If BNSF achieved UNP’s margin, it would earn $1.3 bilion more, a fact noted by Greg Abel in his letter to shareholders.

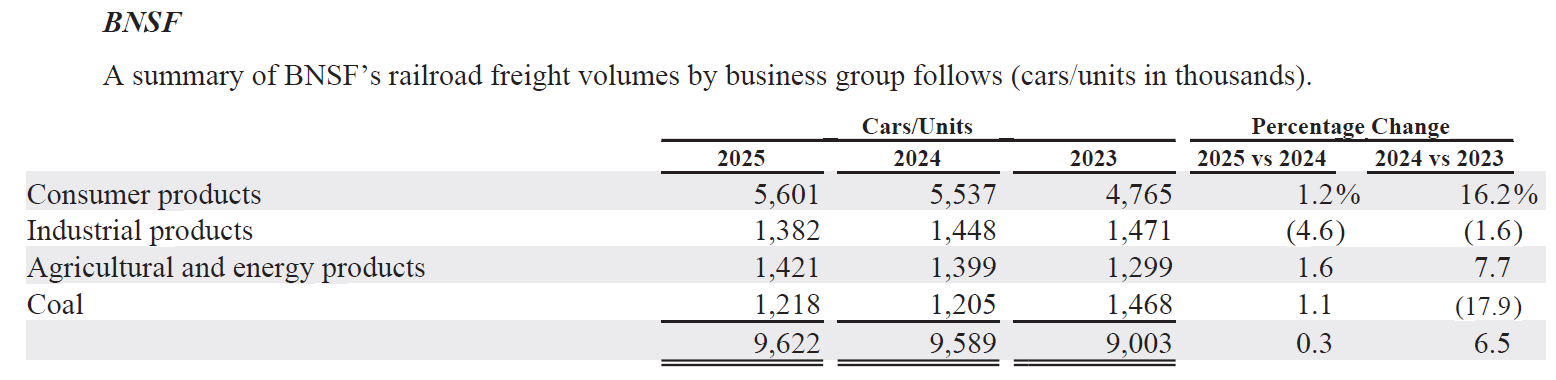

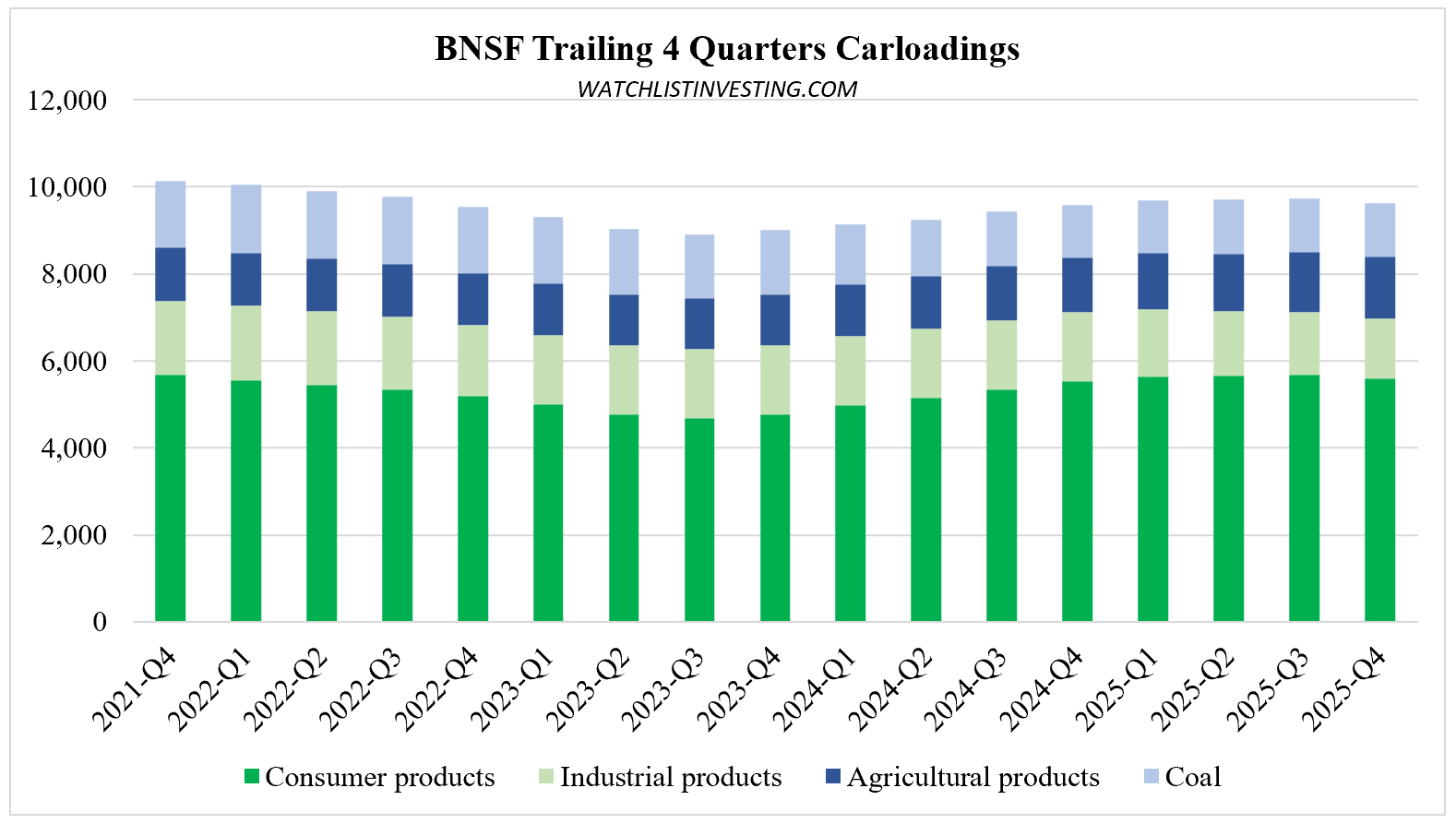

As seen in the table and chart below, volume is fairly flat and stable. BNSF should be able to right-size its expenses to this level of volume before long.

Coal volume was up 1.1% in 2025 but is down 20% from three years ago. Near-term demand may see this abate but the long-term decline is inevitable.

BNSF’s capex has averaged about 140% of depreciation over the past three years. Flat unit volume highlights the fact that BNSF must spend about $1 billion in excess of its depreciation charges just to maintain its business. This means true economic income was probably about $4.5 billion last year and emphasizes the need to get the operating ratio back to peer levels. (No surprise that dividends to BRK were $4.4 billion, about equal to economic earnings; BNSF preserved its levels of cash and debt.)

I think BNSF is probably worth between $80 billion and $90 billion. I put a 15x multiple on the $5,476 million of earnings. This feels fair, as earnings are overstated due to the capex/depreciation mismatch described above, but also considering that the rail is underearning its potential. Each factor, plus and minus, is about $1 billion and we don’t need to split hairs. Another very minor plus is a small boost from deferred taxes that’s probably worth a few hundred million a year.

A note on valuation: Just because UNP is trading at $155 billion doesn’t make BNSF automatically worth that much; I have to go where my reasoning leads.

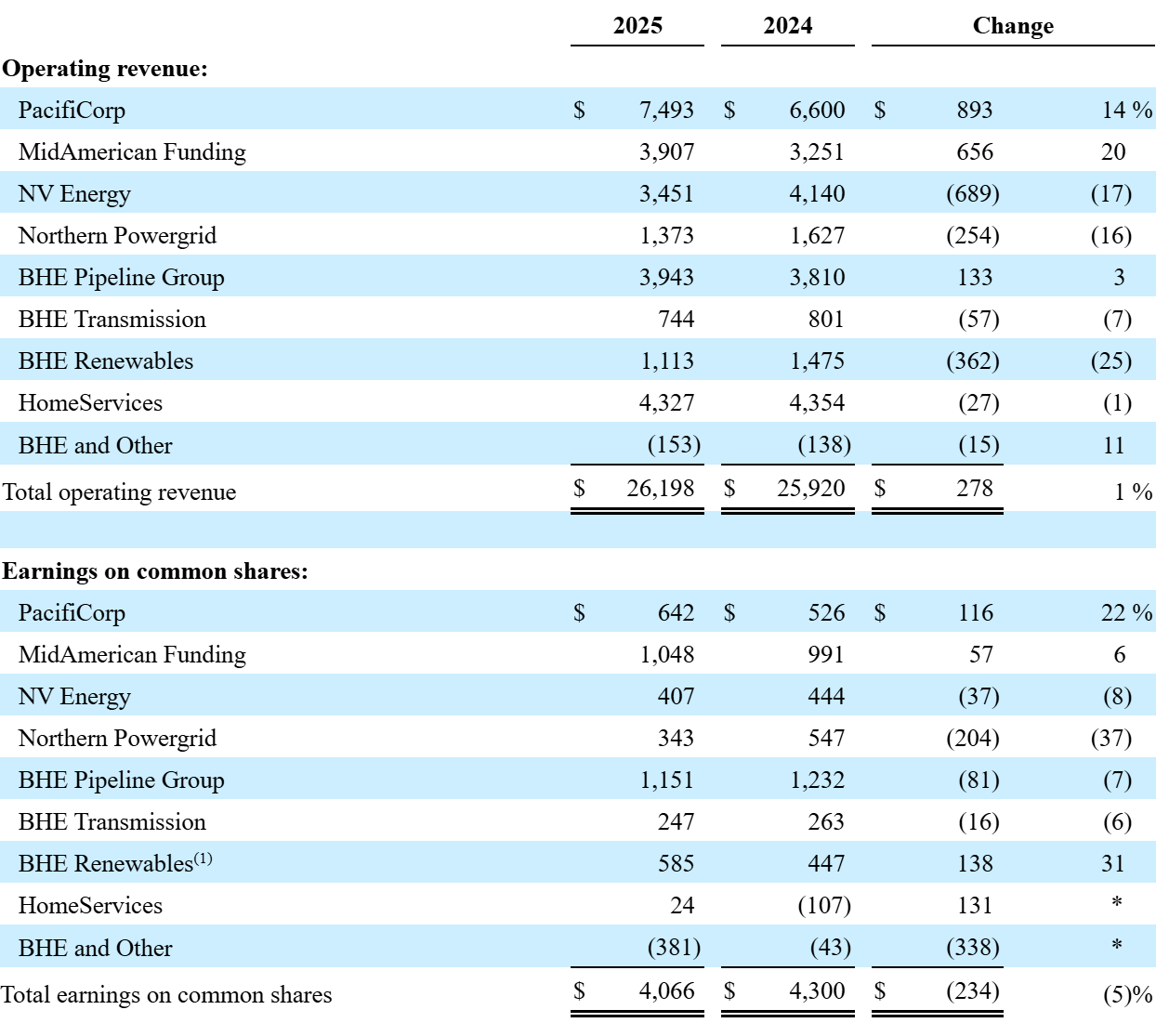

Berkshire Hathaway Energy

BHE has grown from a base in the Midwest to become one of the largest, most respected, and most efficient operators in the United States.

Here is an overview of the major segments of the company as they exist today:

MidAmerican Energy Company: Regulated electric and gas utility

PacifiCorp: Regulated electric utility

BHE US Transmission: Regulated electric transmission

NVEnergy: Holding company for:

Nevada Power Company: Regulated electric utility

Sierra Pacific Power Company: Regulated electric and gas utility

Northern Powergrid: Holding co. for two United Kingdom-based electric distributors

Altalink: Alberta, Canada-based regulated transmission

BHE Pipeline Group:

Kern River: Regulated natural gas transmission

Northern Natural Gas: Regulated natural gas transmission

BHE GT&S: Various natural gas assets acquired from Dominion Energy

BHE is in a unique position. On the one hand, it’s PacifiCorp subsidiary is mired in lawsuits and uncertainty, a result of several wildfires. On the other hand, data center demand, coupled with its low-cost position, is a truly enormous opportunity.

Wildfire accruals totaled just $100 million in 2025, down from $346 million in 2024, and $1.9 billion in 2023. While $1.7 billion has been paid, the ultimate liability remains unknown and the regulatory/political landscape is uncertain. In February 2026, PacifiCorp announced it entered an agreement to sell its Washington state electric utility to Portland General Electric for $1.9 billion. This seems to be the beginning of a strategy of reducing risk in unfavorable regulatory areas in favor of investment in other areas.

Data center demand is truly enormous. According to a BHE presentation, meeting current demand could result in 12% growth per year through 2030, truly unheard of growth rates.

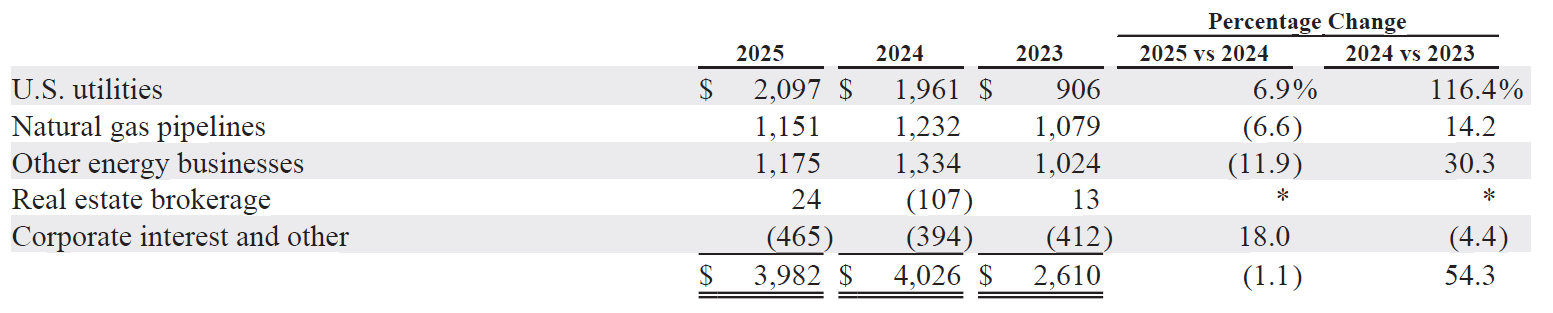

Viewing BHE through a few major categories, US utilities saw 2.2% higher volume and higher prices.

Lower margins on natural gas and higher expenses reduced earnings in the pipeline businesses.

Earnings at the other energy businesses, which include everything from the UK utility to renewables, declined almost 12%. Berkshire provides scant details, but luckily, BHE files its own 10K and we can find answers there. Northern Powergrid (the UK distribution business) saw earnings fall 37% primarily from lower rates and inflationary pressures. Meanwhile, the renewable business grew 31% mainly from higher wind, natural gas, and geothermal earnings.

BRK Home Services rebounded to a profit largely due to a $140 million charge taken in 2024 as part of its industry group settlement.

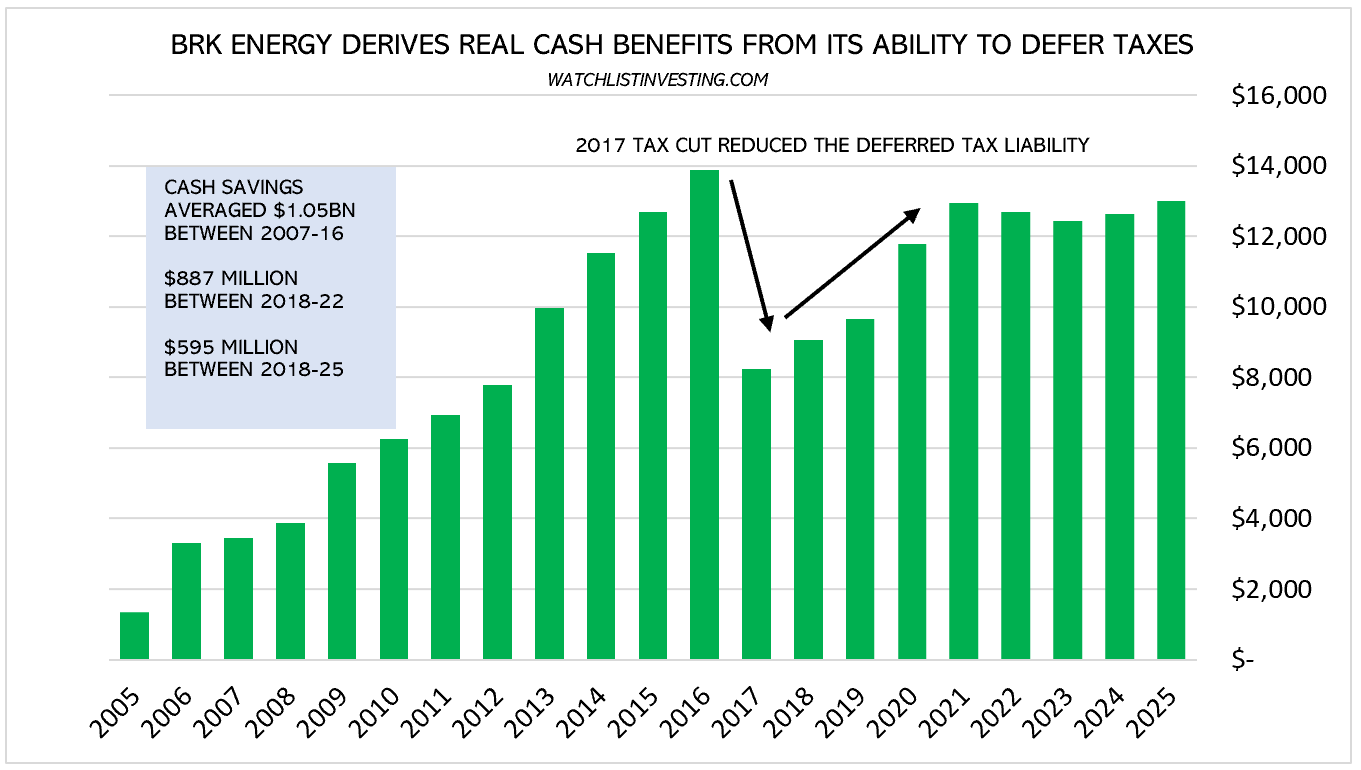

Like BNSF, BHE receives a boost from accelerated depreciation, though this benefit has moderated considerably in recent years.

Right now, I think a 15x multiple on the roughly $4 billion of after-tax earnings plus deferred tax savings is fair, leading to a value of $70 billion.

There are risks in the current wildfire litigation and in future regulatory/political uncertainty. Additionally, BHE has historically benefited from clean energy credits, which are under pressure.

These risks and headwinds are balanced against the significant demand coming from data centers.

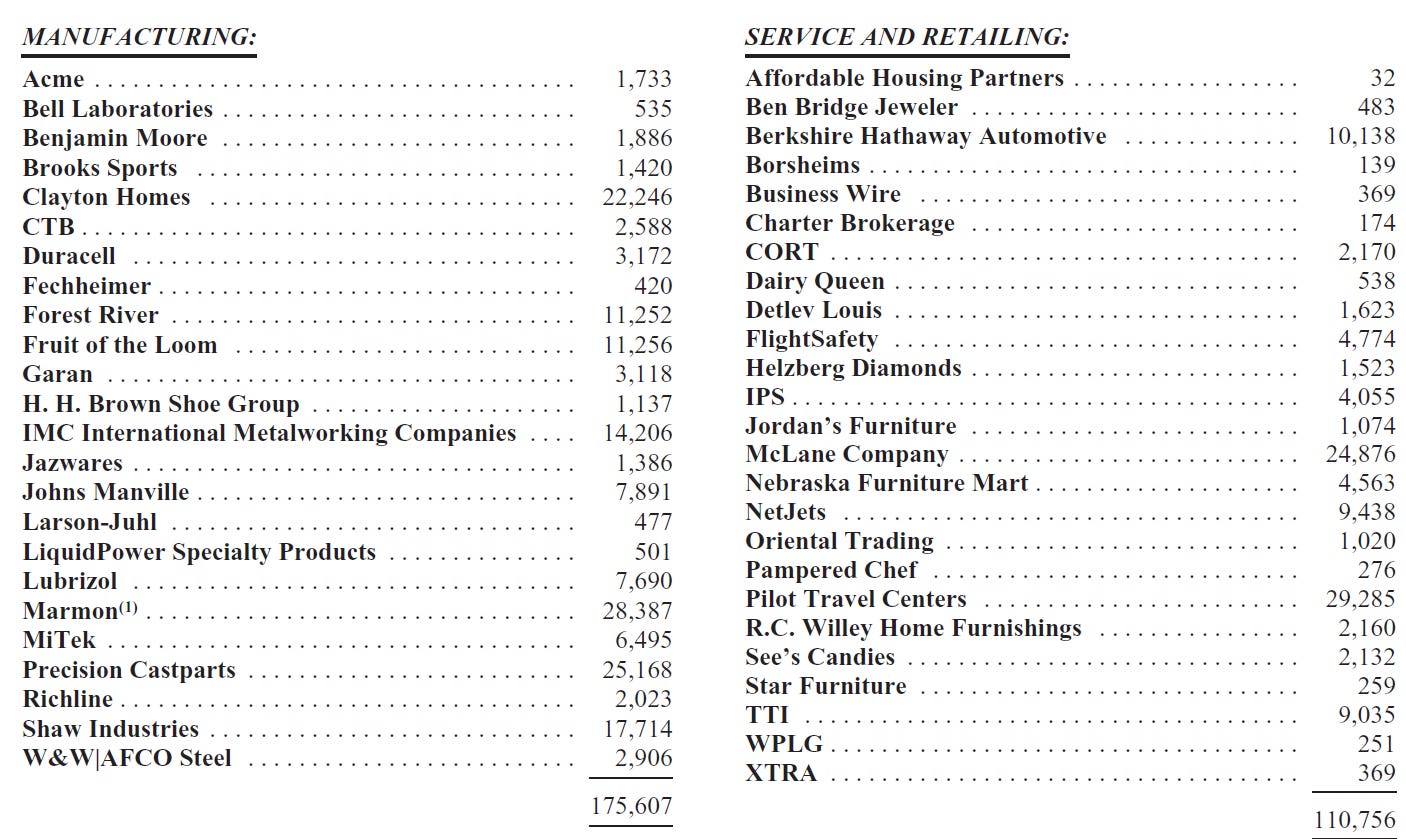

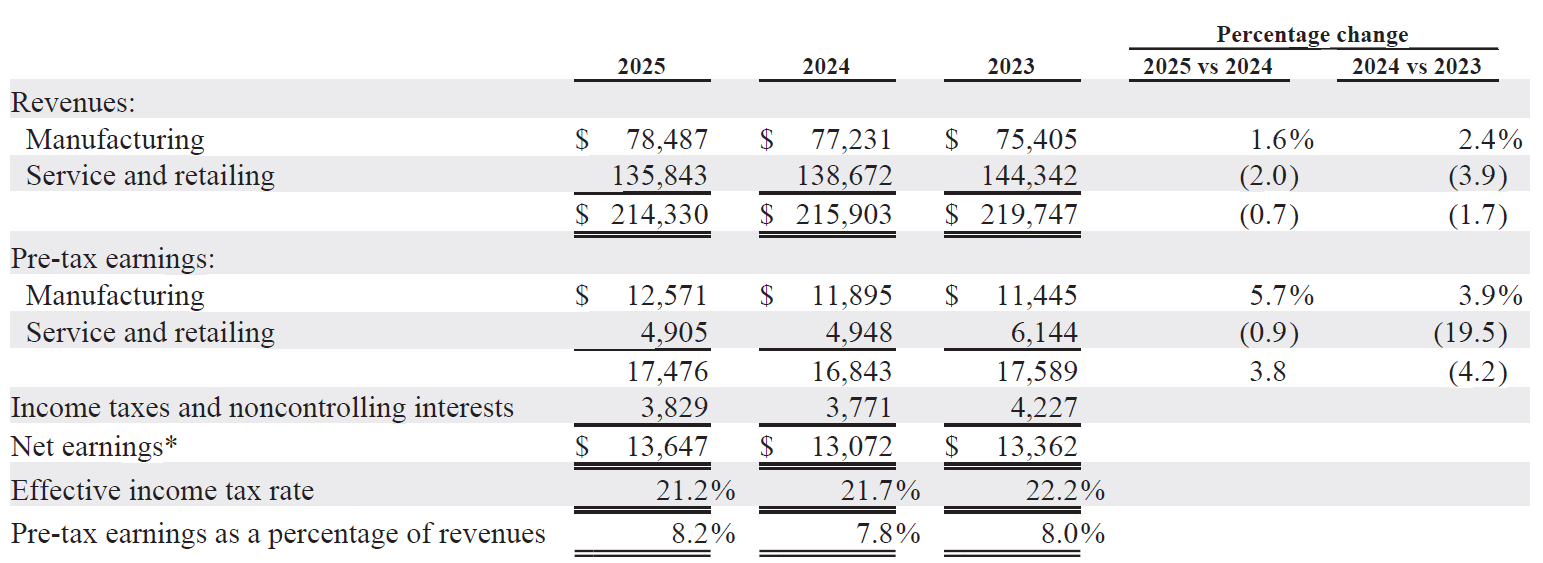

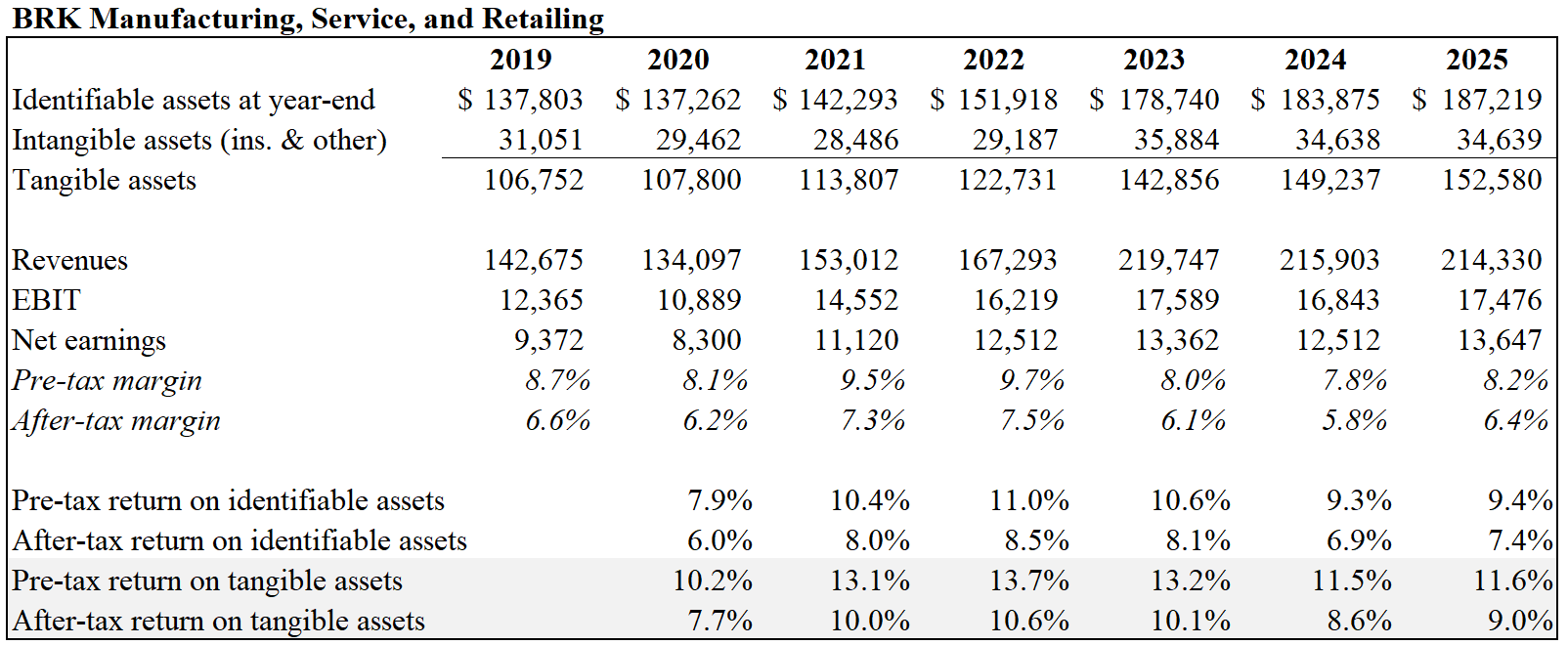

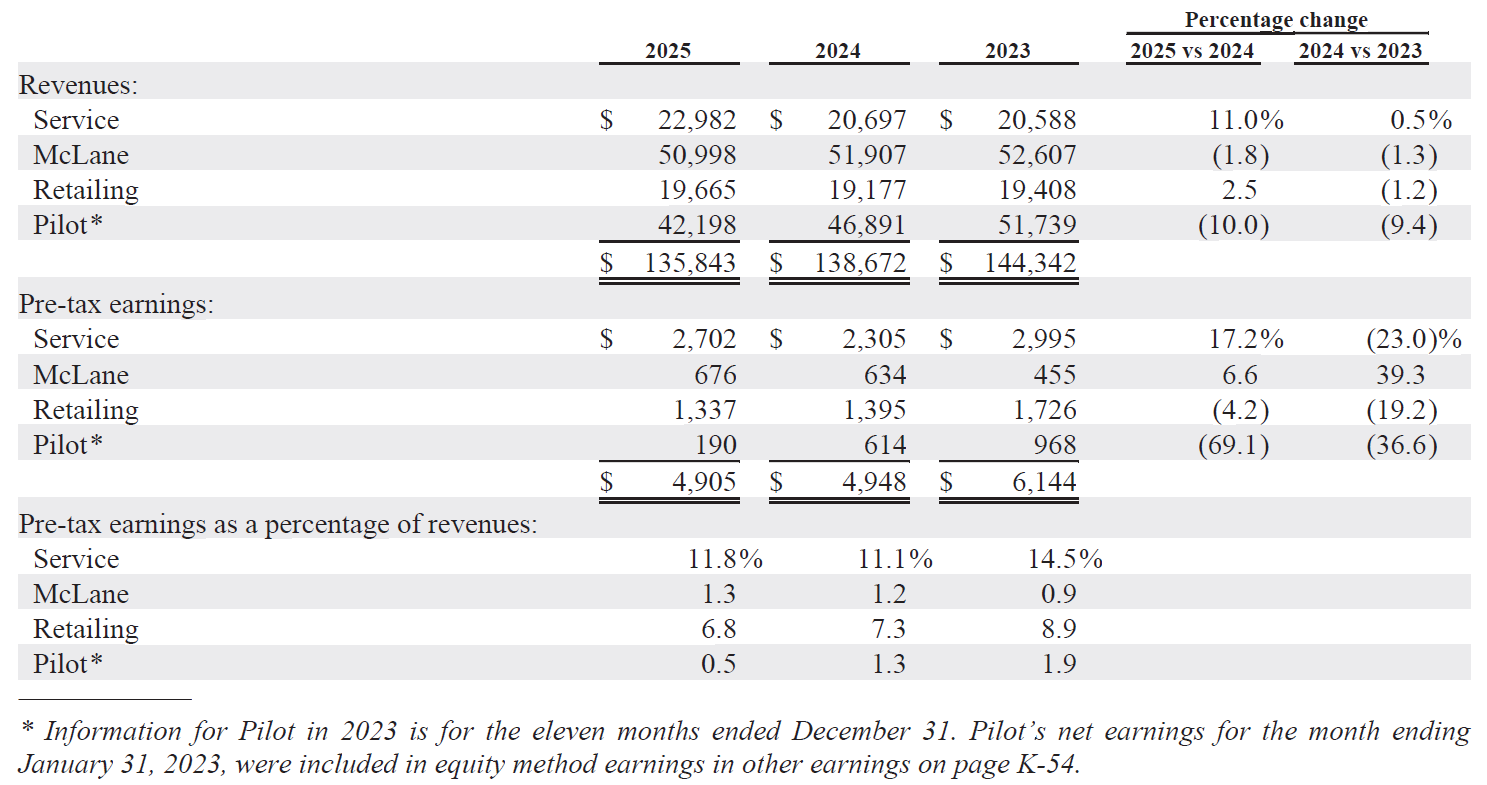

Manufacturing, Service, and Retail

With 110,000 employees, $214 billion of revenues, and net earnings of $13.6 billion, the MSR segment is a huge operation within Berkshire. Many of its businesses are large in their own right. The best example of this is Marmon, with 28,000 employees and 100 operating businesses of its own, one of which is Scott Fetzer, a mini-conglomerate of its own (we’re at the 3rd level of the nesting doll) with a dozen subsidiaries.

Results in 2025 were satisfactory, with a pre-tax margin of 8.2%, the highest in the last three years. We have scant detail on the composition of the balance sheet of this segment. We know it employed $185.5 billion of average “identifiable assets as year-end”. A straight calculation using net earnings puts return on assets at a respectable 7.3% (remember, we don’t know what payables + accruals amounted to, and we know there’s a modest amount of debt).

Of note, the inclusion of Pilot, with its low margin (but satisfactory return on capital) business skews the longer-term view of margins.

Combined, they spent $6.3 billion on capex compared to depreciation and amortization of $5.4 billion.

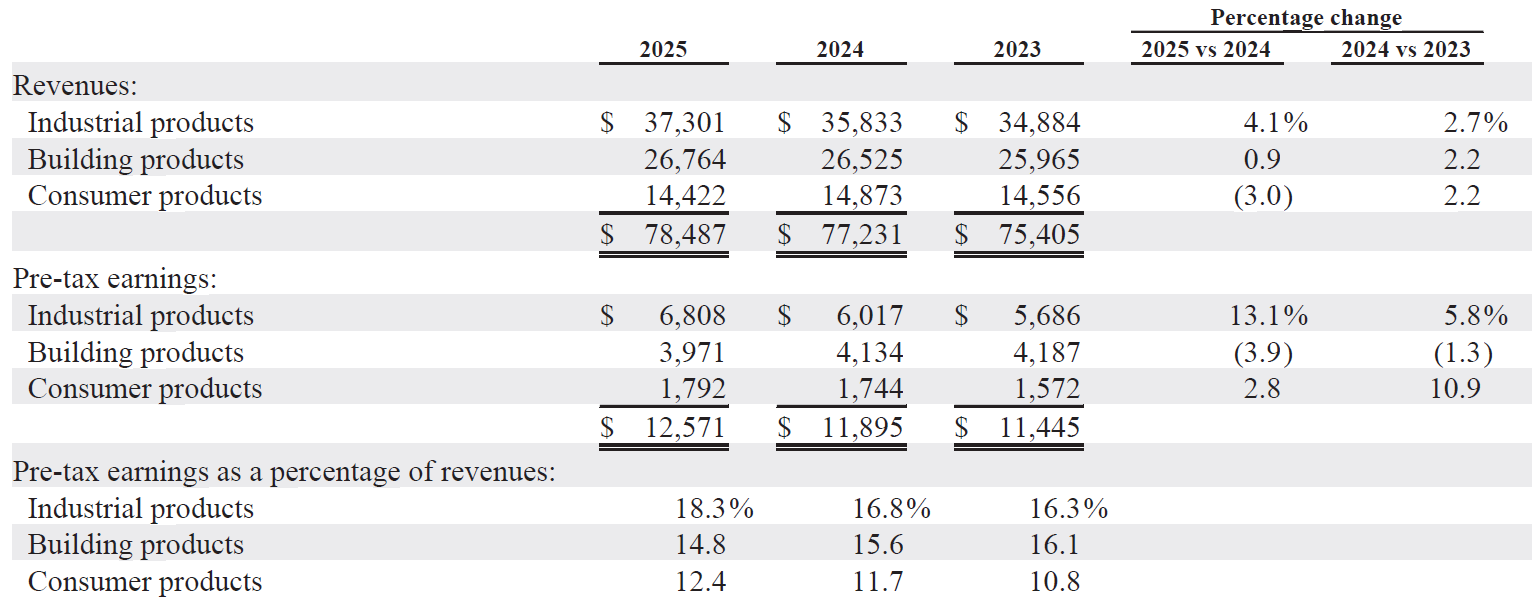

Manufacturing

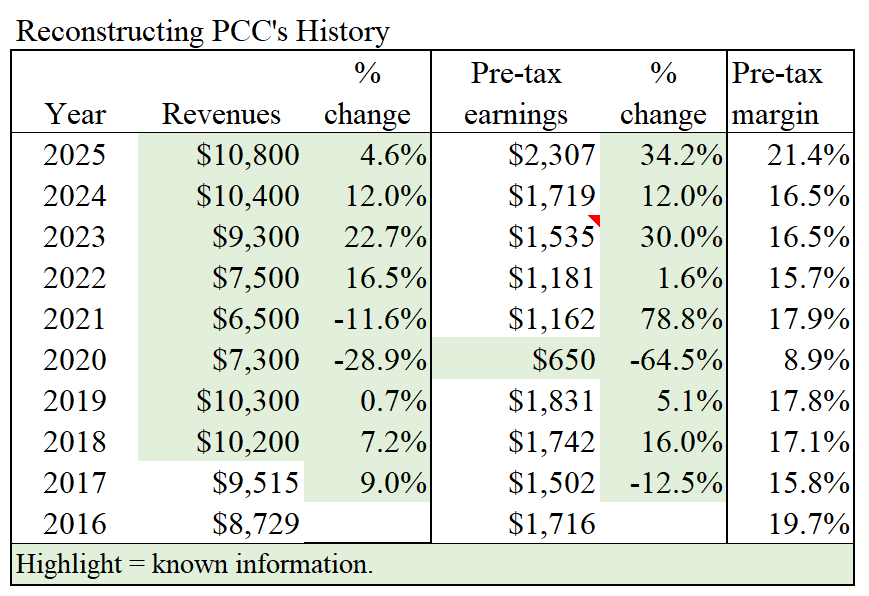

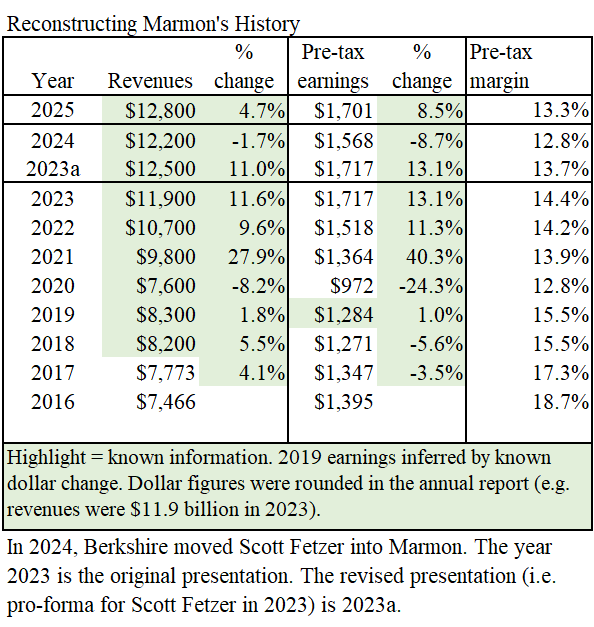

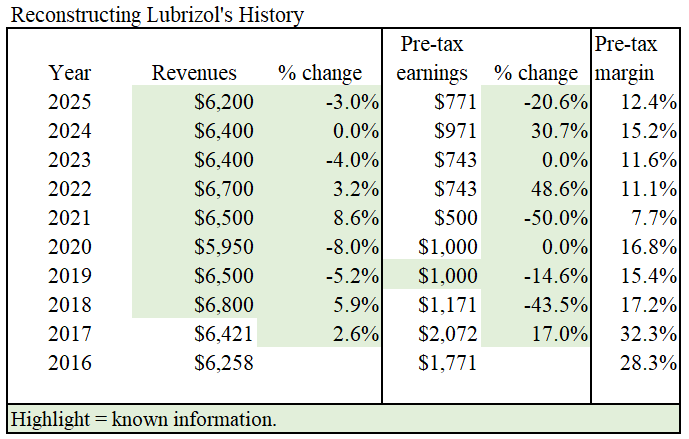

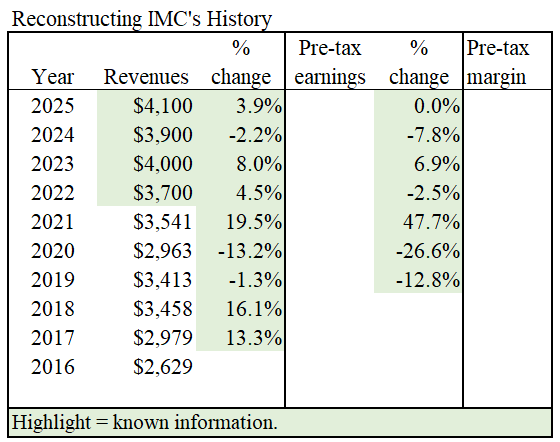

Industrial products were the star in 2025 with a record pre-tax margin of 18.3%. Thank Precision Castparts, whose pre-tax earnings swelled 34% on strong aerospace demand. Lubrizol’s earnings slid 20.6% on end market weakness as well as restructuring costs and litigation. Marmon had a good year with earnings up 8.5%, including strength in Plumbing and Refrigeration (revenues +11.7%), though Crane Services fell 12.6% from price competition and fewer wind projects. IMC looks to have had a middle-of-the-road year.

Annoyingly, Berkshire only gives us the percentage changes this year. Below, I’ve reconstructed the history of pre-tax earnings based on known disclosures throughout the years.

Clayton Homes leads the Building Products segment with about half of its revenues. Nothing too exciting from Clayton. Ditto with the other building products companies, whose revenues slid 2.1% and pre-tax earnings fell 8.1% due to slowing housing markets.

Consumer Products results were flat in 2025. Sales were off 3%, but pre-tax earnings grew a like amount, which looks to be largely the result of Duracell booking refundable tax credits for 2023-25 in 2025.

Service and Retailing

The Service businesses had a great year in 2025. Revenues were up in aviation services (9.9%), IPS (24.2%), and TTI (12.3%). Berkshire attributed the 17.3% increase in pre-tax earnings to aviation services and TTI.

Sluggish demand resulted in lower earnings from the Retailing businesses, although Nebraska Furniture Mart was singled out as the sole exception.

Pilot continues to struggle amid a rebranding effort, lower margins, and higher costs.

McLane long struggled with brutal competition and has been back in the mix the last few years. Results in 2025 continued the trend, with a margin of 1.3% (small, but it has a huge turnover; the margin had been as low as 0.5%).

MSR Valuation

I continue with my 15x multiple on net earnings. That produces a value of $205 billion, up about 4.5% from 2024. I think that’s fair for a few exceptions, many very good, and a bunch of average businesses.

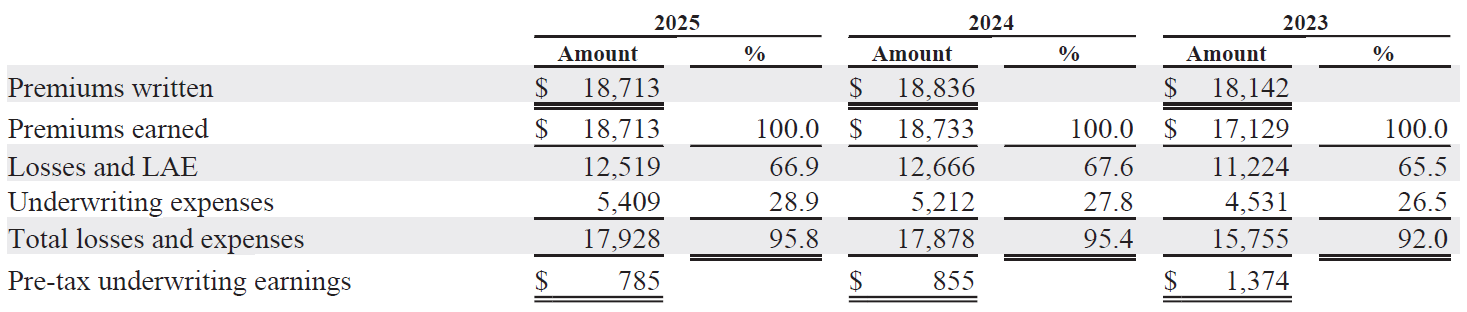

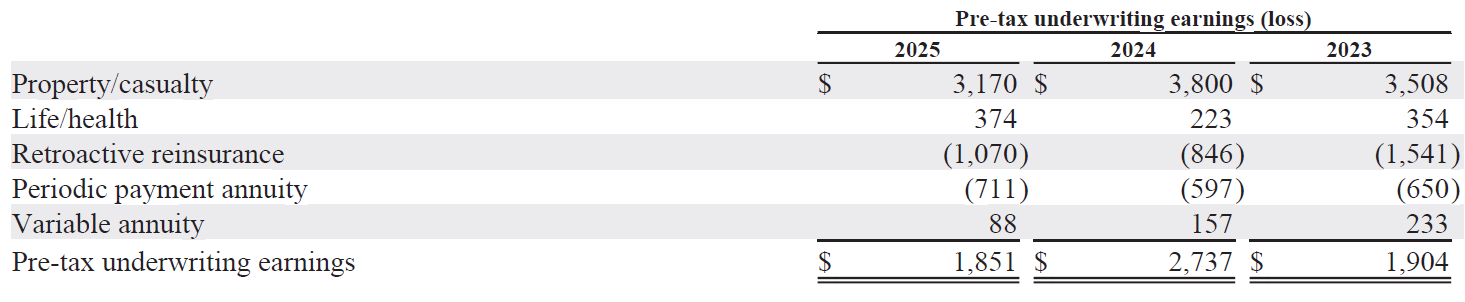

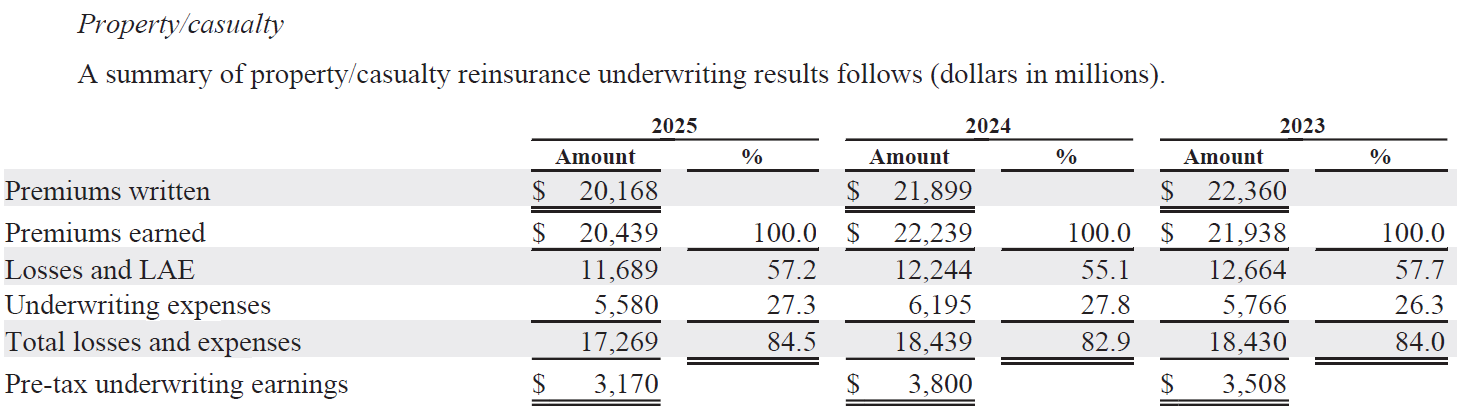

Insurance

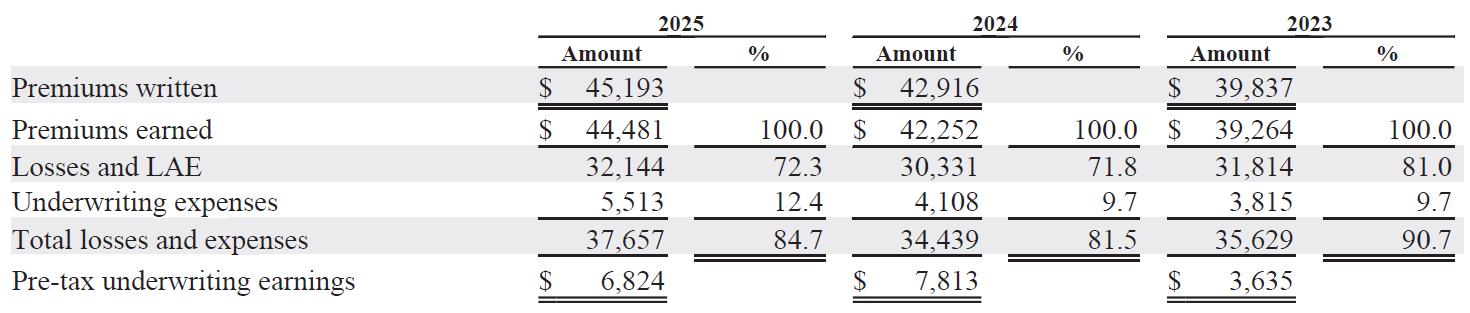

The insurance segment is simply printing money. Strength at GEICO and low storm activity in reinsurance have produced stellar results.

Berkshire earned a 10.64% margin on $88.9 billion of premiums in 2025. Flipped around, that’s a 89% combined ratio, which isn’t sustainable.

I think it’s fair to adjust the margin to 4% (96% combined) and put a 12x multiple on the resulting $3.56 billion of pre-tax earnings. (12x pre-tax = 15x after-tax @ 21%).

Retroactive reinsurance and periodic payment annuity lines have been on run-off for many years now. Some day, Berkshire will write another large retro policy (perhaps on capped cyber risk???) and will benefit from its patience.

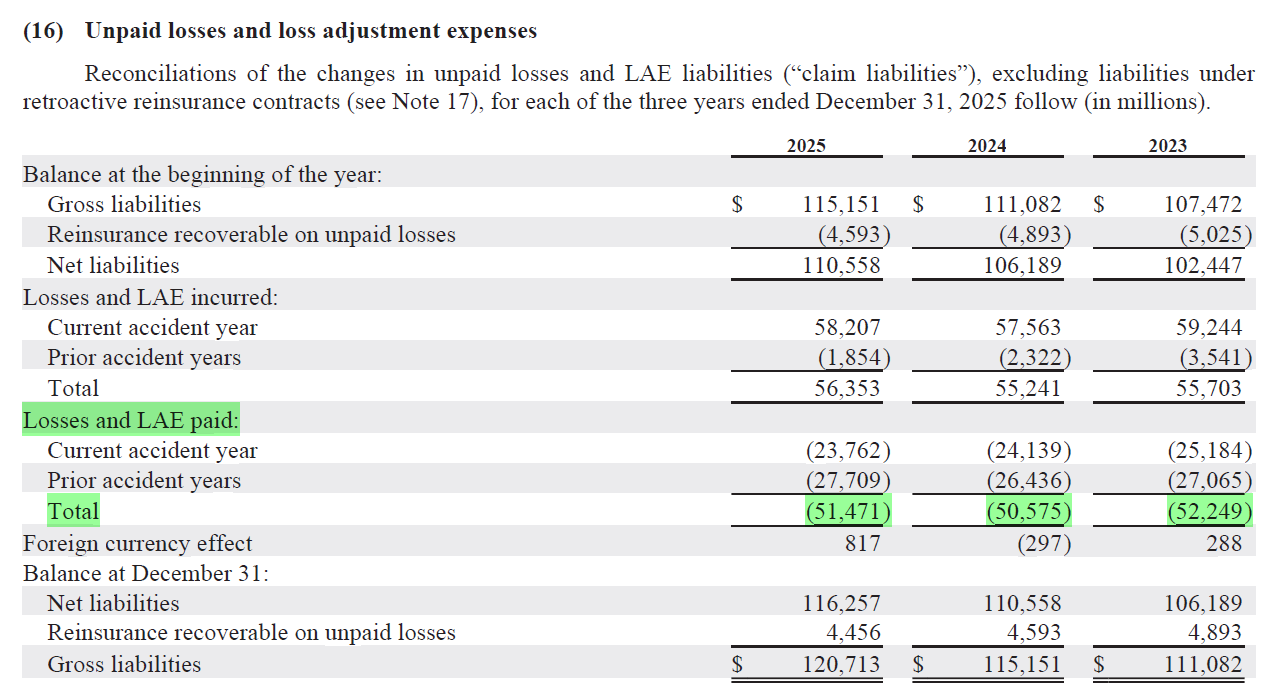

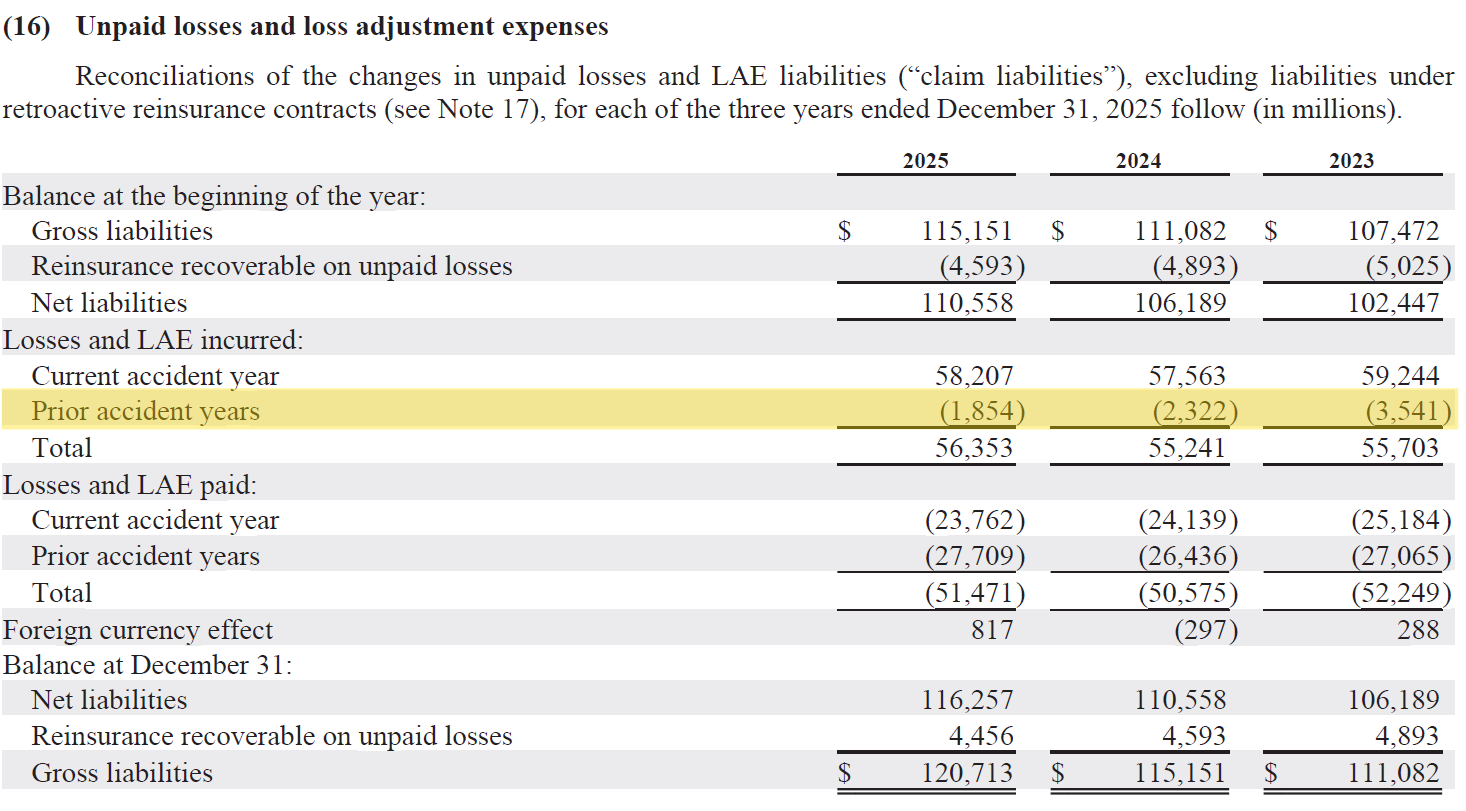

One of my favorite tables… this shows Berkshire’s conservatism. The highlighted line is what’s known as reserve development. Negative figures are called favorable development, which means Berkshire overestimated its losses in prior years (read: underestimated its profit). It’s one of the key items to keep track of.

Holding Company

Finally, we have to adjust for debt at the holding company level. Berkshire had borrowings of $22.6 billion. Including, remarkably, $14.9 billion of yen-denominated debt with an average rate of 1.2% used to fund the cost basis of the Japanese trading company investments.

Valuation Conclusion

I think Berkshire is worth about $1 trillion today, or roughly 1.4x book. The conglomerate is a remarkable collection of assets, many of which are simply not replicable. Berkshire has many advantages being under one umbrella and should compound at a decent but by no means exceptional rate.

Greg Abel’s first letter to shareholders was well written and reiterated his buy-in to the Berkshire way. I have no doubt that Greg will “keep the culture”, and I’m excited to see the next chapter under his leadership.

Stay Rational!

Adam

What do you think? Hit reply or leave a comment below.

Pre-Order the 2nd Edition Now!

Amazon, Barnes & Noble, or directly from Harriman House, and at other major bookstores, for delivery in April 2026.

Praise for the 2nd Edition

I’m incredibly grateful for the people who took the time to review early drafts of the new material and provided feedback, as well as praise for both editions:

“If you want to understand how Warren Buffett built Berkshire Hathaway into one of the most valuable businesses in the world, you have to read this book. This is your opportunity to stand beside Picasso as he paints each brush stroke. A must read for all Buffett and Berkshire groupies.”

- Bill Ackman, Founder and CEO of Pershing Square

“I and my teammates at the Gabelli Organization have been tracking Warren’s success for some 50 years. Adam’s book captures the work and highlights the history of Berkshire and the hard and diligent work of Buffett and Munger, Jain and Abel, and Combs and Weschler.”

- Mario Gabelli, Chairman and CEO, Gabelli Funds

“Adam Mead’s discussion of the values and virtues which have shaped Berkshire Hathaway over 50 years is a must read for those investors in search of the forces that have delivered such investment value over time.” – Thomas A. Russo, Gardner Russo & Quinn LLC

“Few activities can be more rewarding for any value investor than studying the history and evolution of Warren Buffett and Berkshire Hathaway. Adam has done us a huge favor with his yeoman efforts in producing this treatise. Since it is chronologically ordered, it is an invaluable reference guide for all things Berkshire.” — Mohnish Pabrai

“Adam continues to deliver a resource very valuable to both Berkshire fans and the investor community as a whole, his depth of knowledge is clearly demonstrated here again. I thoroughly enjoyed this latest addition.” - Dan Calkins, Chairman & CEO, Benjamin Moore

“The question must be asked, ‘Why another Berkshire book?’ When you read this monumental effort by Adam Mead, the answer will be obvious. Read cover to cover, both the uninitiated to Berkshire and its most ardent followers will derive enormous utility and satisfaction from it. I learned so many new and important things about Berkshire and its history. It is my pleasure to encourage you to enjoy this gem.”

- Christopher P. Bloomstran

“Whatever Adam writes is always first-class - guaranteed.

-Andy Kilpatrick, Author, Of Permanent Value: The Story of Warren Buffett

“With this project, Adam has done a wonderful job extending the Berkshire Classroom by providing a comprehensive analysis of the rich corporate history and unique entrepreneurial leadership.” — Mac Sykes, Gabelli Funds

“Adam Mead’s The Complete Financial History of Berkshire Hathaway is the definitive history of Berkshire. While there have been countless books written about Warren Buffett’s investment approach, none have so meticulously documented Berkshire’s capital allocation decisions from the very beginning. The depth of research is staggering, transforming the complex and sometimes chaotic story of how a small textile mill became a financial conglomerate into a clear, year-by-year narrative of every significant investment and acquisition. In this updated edition, Adam carries the narrative through Berkshire’s sixth decade and the methodically planned leadership transition to Greg Abel. For students of business history, this is an indispensable resource.”

-Patrick Gaughen, President and Chief Operating Officer, Hingham Institution for Savings

“The definitive story of Berkshire Hathaway—how Buffett and Munger turned a failing textile mill into one of history’s greatest wealth-creating enterprises, with timeless lessons in business, investing, and leadership.”

-Vitaliy Katsenelson, CEO of IMA, Author of Soul in the Game

“Berkshire Hathaway is a company with few, if any, parallels in business history. Under the leadership of Warren Buffett, it was transformed from a New England textile mill that would ultimately be shuttered to a sprawling conglomerate with a market valuation of more than $1 trillion. With this updated edition of “The Complete Financial History of Berkshire Hathaway”, Adam provides a thorough review of the key decisions that created the modern Berkshire Hathaway, an outcome inextricably tied to the investment and business wisdom of Warren Buffett and his business partner, Charlie Munger. In a few hundred pages, Adam adeptly runs through six decades of Berkshire’s history. For Buffett and Munger fans who want to truly understand how Berkshire was created, this book is a must read.”

- Alex Morris, Founder of TSOH Investment Research and the Author of Buffett & Munger Unscripted

“A meticulous chronicle of Berkshire Hathaway’s remarkable final act under Buffett’s leadership. Mead’s granular analysis of Buffett’s capital allocation decisions—from the $78 billion in share repurchases to the masterful Apple investment—provides unmatched insight into how the world’s most successful conglomerate navigated unprecedented scale and succession challenges.”

-Tobias Carlisle, Portfolio Manager, Acquirers Funds®

“This exceptional history of Berkshire Hathaway will appeal to history buffs, finance enthusiasts, and investing professionals alike. Mead combines rigorous research with remarkably clear storytelling, tracing the company’s ascent from a struggling textile mill to one of the world’s most admired conglomerates. The book is impressively detailed yet fully accessible—equally valuable for students learning the foundations of investing and for seasoned professionals looking to deepen their understanding of Berkshire’s evolution.”

-Gillian Zoe Segal

“With his ability to make complex things seem simple, Warren Buffett made the difficult work of building Berkshire Hathaway look easy. With this excellent history, Adam Mead takes us behind the scenes to see the details of how that work happened and was so successful. For anyone interested in Berkshire Hathaway, or the development of American capitalism, this is essential reading.”

- Bryan Lawrence, Founder, Oakcliff Capital

“There is simply no book that details the economic lore of Berkshire Hathaway better. A true exposé that every intelligent investor should read.”

- Gwen Hofmeyr, Founder, Maiden Financial

“The most comprehensive book on Berkshire Hathaway that has ever been written. It belongs on the shelf of every business enthusiast!”

-Andrew Wagner, Author of the Economics of Online Gaming and Founder & Chief Investment Officer of Wagner Road Capital Management

“Adam’s accounting of the Financial History of Berkshire is like candy for Finance and Business Junkies alike. It’s a must read if you’re interested in studying the greats.”

- Carter Johnson, Managing Partner, Singleton Valuations

“I thought nothing else of value could be written about Warren Buffett. I was wrong. Adam’s detailed chronology of Berkshire’s evolution reveals the successes and failures of Warren in a unique and digestible way. A worthwhile read for every Buffett scholar, amateur and professional alike.” — Drew Estes, Banyan Capital

“Mead has done the Berkshire faithful an incredible service by stitching together the narrative and numbers so tightly, you can see the compounding in action—updated and genuinely useful.”

-Jacob Taylor, CEO of Baserate

“Adam Mead’s work reminds us that true value is found not just in numbers, but in the lasting quality where few care to linger. By doing exceptional due diligence his book clones the lessons of Warren and Charlie.”

-Jeff Gilbert

Adam Mead’s updated “Complete Financial History of Berkshire Hathaway” is a book like no other—chronicling six decades of evolution while reminding us that Berkshire, though Buffett’s masterpiece, remains subject to constant change—an indispensable addition to any serious investor’s bookshelf.

-Bogumil Baranowski, Founder of Blue Infinitas Capital, Author of “Money, Life, Family”, Host of Talking Billions Podcast

A rigorous and useful summary of Berkshire’s vast empire. Many will be grateful to you for drinking from the fire hydrant, so they don’t have to. I tend to agree with an intrinsic value, that may seem conservative, compared to some of the other areas of the market based on narratives about a future that may disappoint. Highlighting the BNSF Capex in excess of depreciation charges; wildfire liability risks and the unusually favourable insurance combined ratio, is exactly the type of rational discussion I enjoy. Builds trust and manages expectations and is a reflection of the culture at Berkshire.

The underwriting profits are perhaps even more noteworthy given the higher interest rates being earned on the float. Will be interesting to see how that develops over the coming years. There is certainly a huge skill factor at play but it does look unusually profitable for a commodity business.

While Berkshire may be fairly valued currently and management clearly agree, given the extremely low buy back activity at these prices, relative to other valuations, it’s an extremely attractive hold. Optionally, conservative accounting, capital allocation discipline and shareholder friendly management. For me the most attractive part of owning Berkshire currently, is how it’s positioned to negotiate difficult waters ahead. Cash, essential infrastructure, insurance, U.S. oil, consumer goods equities (Apple, Coke) and a diversified stable of wholly owned cash gushing businesses, makes Berkshire an incredibly attractive way to remain invested whatever the economic and market gods may unleash upon us. And as you pointed out, exposure to all kinds of large high growth areas.

Personally I would like to see Greg Abel buy back a large amount of shares at a discount to IV, that does happens from time to time (2020, 2009 for recent examples). It would be disappointing if he was doing it at current prices.

Thank you for a great article Adam! Much appreciated by your fellow shareholders.

The article's calculation of intrinsic value left me somewhat puzzled. If the current intrinsic value is only $1 trillion, Greg Abel would definitely not announce a buyback plan at this time, as it clearly contradicts Berkshire's definition of the right timing for buybacks. Yet, the author concludes by affirming that Greg Abel will adhere to Berkshire's principles, which is utterly contradictory and baffling.