Your Margin of Safety Might Not Be What You Think It Is

Lessons from Benjamin Graham and Bruce Greenwald

Imagine you find a company with $80 million in net operating profit after taxes (NOPAT), $50 million in cash, and $700 million in debt.

At a reasonable 10x multiple of NOPAT, the company is worth $800 million.

$800 million value less $650 million in net debt = $150 million of equity value.

To your great delight, the market value of equity is $75 million.

You’ve just found yourself a stock with a 50% margin of safety.

Not So Fast…

As you might expect from the title of this post, caution is warranted.

The setup above comes from Bruce Greenwald’s excellent book, Value Investing: From Graham to Buffett and Beyond, 2nd Edition.

As Greenwald notes on page 120, the margin of safety analysis above is incorrect.

The right way to think about the margin of safety is at the enterprise level.

Earnings power is tied to enterprise value, which includes debt. What happens if sustainable NOPAT is really 10% less, or $72 million? Now the enterprise value is $720 million, and the value of equity is $720 million - $650 million = $70 million.1

To our horror, we’re now stuck with a negative margin of safety (a margin of risk? peril?) of -7%. A 19% decline in enterprise value would wipe out equity entirely!

A Leveraged Enterprise

What’s laid out above isn’t a surprise. Debt increases risk. Most investors understand that.

Just as return on capital employed (or invested capital; pick your metric) cuts across financing choices, the enterprise value margin of safety similarly allows us to view margin of safety in its proper light.

Graham’s Coverage Ratio

In Security Analysis2, Ben Graham discusses a similar concept in coverage ratios. He notes how some analysts then (and I assume some do now) calculate the coverage of fixed charges for a preferred stock issue or junior bond after that of the more senior security, instead of together. To illustrate:

Earnings before interest: $3,978,000

Interest charges: $1,628,000

Preferred dividends: $160,000

The coverage ratio for the interest charges on the debt is simple enough: $3,978,000 divided by $1,628,000 or 2.4 times.

But what about the preferred?

After paying interest, there’s $2,350,000 leftover, which covers the preferred 14.7 times.

Hold on a minute…

If the preferreds have coverage of nearly 15x compared to the bonds at just 2.4x, then the preferreds are safer, right? Yet they’re junior securities. How can that be the case?

The answer is that the analysis is incorrect.

The right way to calculate the preferred coverage is to add $160,000 to $1,628,000 or $1,788,000. That amount is covered 2.2 times by the $3,978,000 available for debt service.

Thus, by framing the problem appropriately, we arrive at a slightly lower (and therefore slightly riskier) 2.2x for the preferreds vs 2.4x for the senior debt.

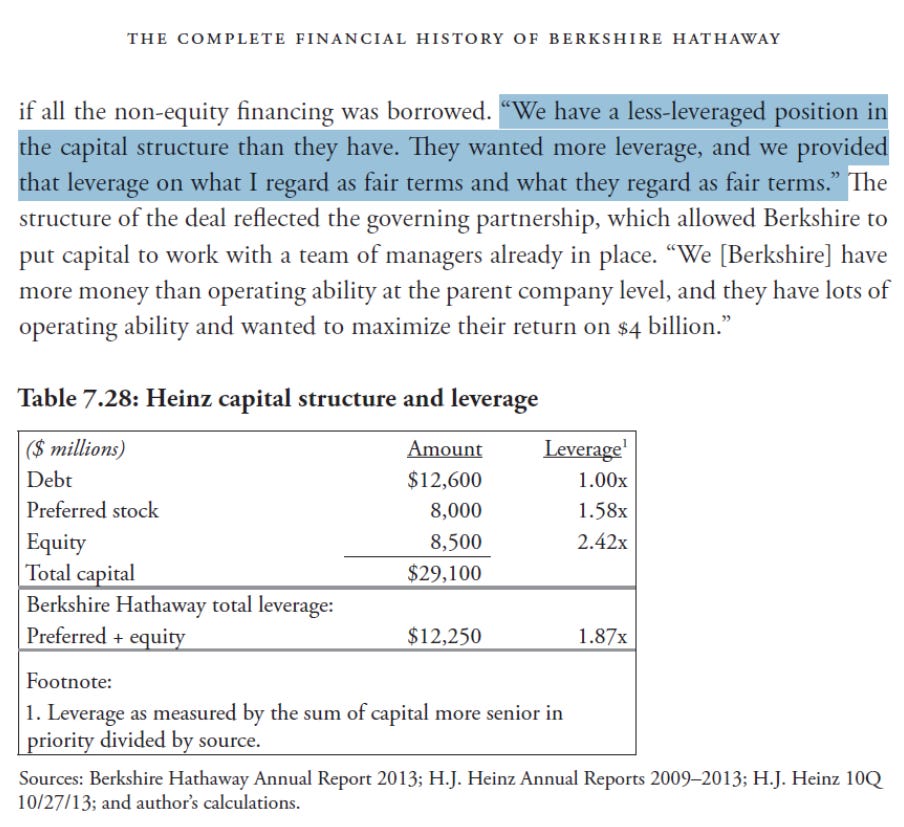

Berkshire Provides Leverage to Heinz

A final example of this analysis at work comes from Berkshire. When Berkshire bought Heinz with 3G Capital, Buffett described his partners as desiring more leverage. By providing the debt (as well as preferred and equity), Berkshire gave 3G the leverage it wanted, and maintained a sensible leverage profile for itself higher in the capital structure.

Conclusion

The bottom line here is simple: beware of the negative effects of leverage, both in its raw form and in your calculations of margin of safety.

More thoughts? Let me know in a private message or leave a comment.

Stay Rational!

Adam

Pre-Order the 2nd Edition Now!

Amazon, Barnes & Noble, or directly from Harriman House, and at other major bookstores, for delivery in April 2026.

Praise for the 2nd Edition

I’m incredibly grateful for the people who took the time to review early drafts of the new material and provided feedback, as well as praise for both editions:

“If you want to understand how Warren Buffett built Berkshire Hathaway into one of the most valuable businesses in the world, you have to read this book. This is your opportunity to stand beside Picasso as he paints each brush stroke. A must read for all Buffett and Berkshire groupies.”

- Bill Ackman, Founder and CEO of Pershing Square

“I and my teammates at the Gabelli Organization have been tracking Warren’s success for some 50 years. Adam’s book captures the work and highlights the history of Berkshire and the hard and diligent work of Buffett and Munger, Jain and Abel, and Combs and Weschler.”

- Mario Gabelli, Chairman and CEO, Gabelli Funds

“Adam Mead’s discussion of the values and virtues which have shaped Berkshire Hathaway over 50 years is a must read for those investors in search of the forces that have delivered such investment value over time.” – Thomas A. Russo, Gardner Russo & Quinn LLC

“Few activities can be more rewarding for any value investor than studying the history and evolution of Warren Buffett and Berkshire Hathaway. Adam has done us a huge favor with his yeoman efforts in producing this treatise. Since it is chronologically ordered, it is an invaluable reference guide for all things Berkshire.” — Mohnish Pabrai

“Adam continues to deliver a resource very valuable to both Berkshire fans and the investor community as a whole, his depth of knowledge is clearly demonstrated here again. I thoroughly enjoyed this latest addition.” - Dan Calkins, Chairman & CEO, Benjamin Moore

“The question must be asked, ‘Why another Berkshire book?’ When you read this monumental effort by Adam Mead, the answer will be obvious. Read cover to cover, both the uninitiated to Berkshire and its most ardent followers will derive enormous utility and satisfaction from it. I learned so many new and important things about Berkshire and its history. It is my pleasure to encourage you to enjoy this gem.”

- Christopher P. Bloomstran

“Whatever Adam writes is always first-class - guaranteed.

-Andy Kilpatrick, Author, Of Permanent Value: The Story of Warren Buffett

I’ve deviated from Greenwald’s example slightly. He used a 15% decline in EV, which reduced equity to $30 million.