Pool Corporation (POOL)

A first look at a distribution business in which Berkshire Hathaway has a 9.2% stake.

Disclosure: None

Diving In

I thought it was about time to take a look at Pool Corporation. Berkshire Hathaway first disclosed a stake in the pool products distribution business in Q3 2024, and upped it to a 9.2% stake in August 2025. Shares currently trade at $231 compared to Berkshire’s estimated average cost of $320.

Said differently, Berkshire’s average price implies a market cap of about $12 billion compared to today’s $8.1 billion, a drop of about a third.

What’s In A Name?

Pool Corporation distributes … pool supplies. Well, mostly. Its primary business is that of distributing swimming pool supplies, equipment, and related products, with a smaller (~8% revenues) portion derived from its landscaping and irrigation business.

The company operates 456 sales centers and distributes its products through five networks: SCP Distributors, Superior Pool Products, Horizon Distributors (irrigation/landscaping), National Pool Tile, and Sun Wholesale Supply.

Pool Corp sits between 120,000 wholesale customers (pool service contractors, builders, retailers, etc.) and 3,500 suppliers, although its three largest suppliers accounted for 43% of COGS (20%, 12%, and 11%).

Some stats about Pools’ pool business and the industry:

Pool Corp Product Breakdown:

64% recurring maintenance and repair of existing installed pools

22% pool remodeling, renovations, and upgrades

14% from new pool construction

Pool Corp Geographic Breakdown:

95% of sales in the US

57% of 2025 sales in the sunbelt states of California, Florida, Texas, and Arizona

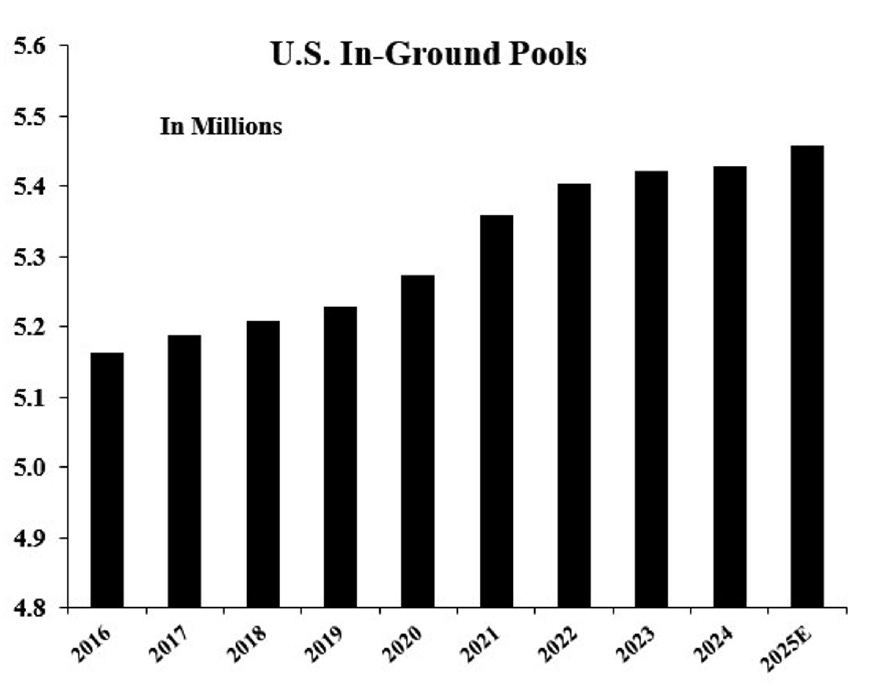

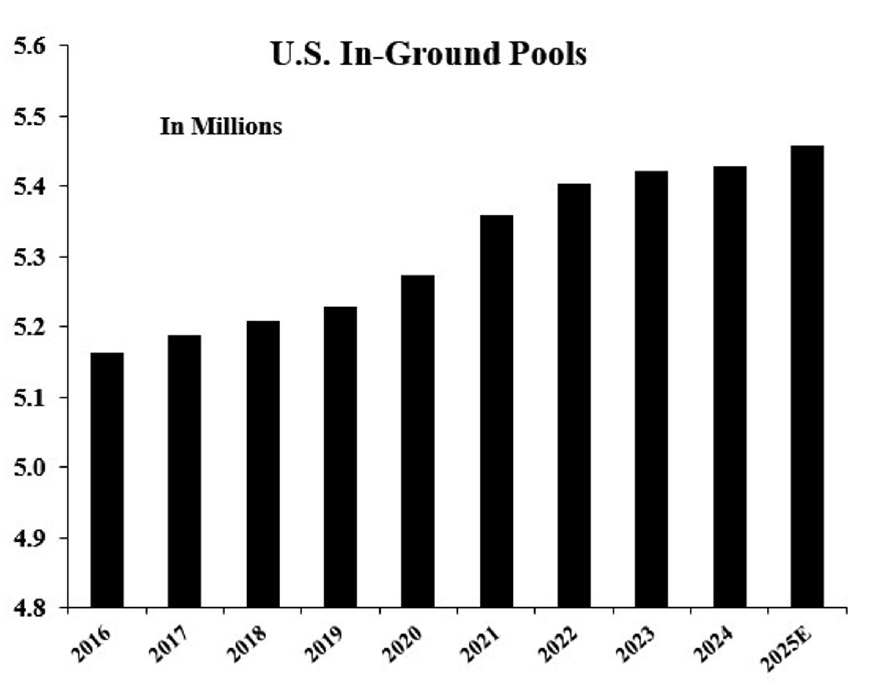

There are 14 million swimming pools and hot tubs in the US, including 5.5 million in-ground pools

The pandemic led to a surge in installations, rising from about 60,000 new installs per year to 100,000 at the peak. The pandemic surge increased the installed base by about 5%

Source: 2025 Pool Corp Annual Report Pool Corp is the largest wholesale distributor of pool supplies in the world. It doesn’t disclose market share; however, it is thought to have a market share of between 25% and 35% of between $15 and $20 billion of industry sales.

A Short History of Pool Corp

1981: Founded by Frank St. Romain and Richard Smith in New Orleans, Louisiana

1993: Partnered with private equity to form SCP Pool Corporation

1995: IPO

1999: Manuel “Manny” Perez de la Mesa named CEO

2005: Entered the irrigation and landscaping business with the acquisition of Automatic Rain Company aka Horizon for $87 million

2008: Acquired National Pool Tile for $28.9 million

2019: Manny steps down as CEO and is replaced by Peter Arvan who joined the company in 2017

2021: Acquisition of Porpoise Pool & Patio for $788.7 million brought Sun Wholesale Supply servicing Pinch A Penny franchise locations, significantly expanding the company’s distribution and retail support capabilities.

Management / Ownership

Peter Arvan: As noted above, Arvan joined Pool Corp in 2017. Previously, he was the CEO of BrightSpring Health Services. He was tapped as CEO in 2019. Arvan was paid a base salary of $900,000 and earned $6.6 million of total compensation in 2025.

Directors earn total fees of about $250,000 per year.

Former CEO, Manuel Perez de la Mesa owns about 3% of the company.

As of the 2026 proxy:

Berkshire Hathaway owned 8%

Kayne Anderson Rudnick Investment Management owned a 5% stake

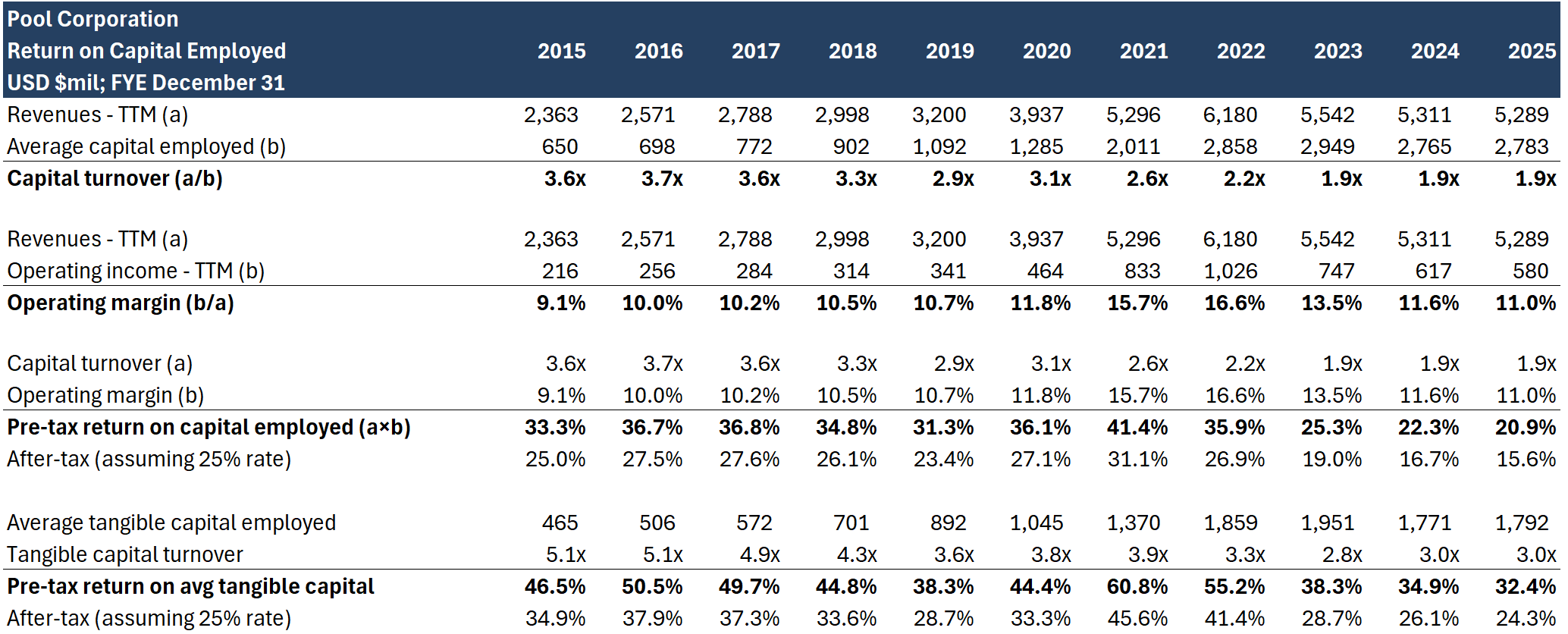

Financial Analysis

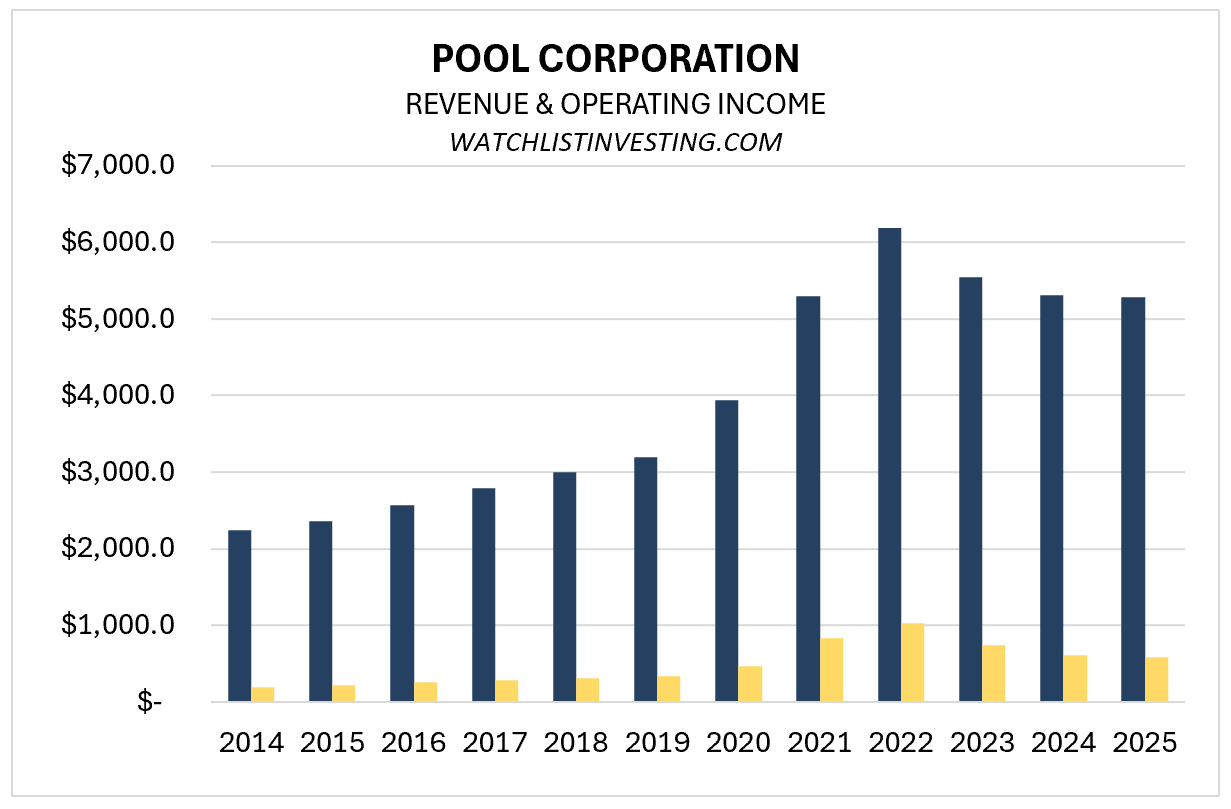

One glance at the income statement and it’s clear that Pool has grown tremendously.

Sales grew from $2.25 billion in 2014 to $3.2 billion in 2019 (a 7% CAGR) before nearly doubling to $6.2 billion in 2022.

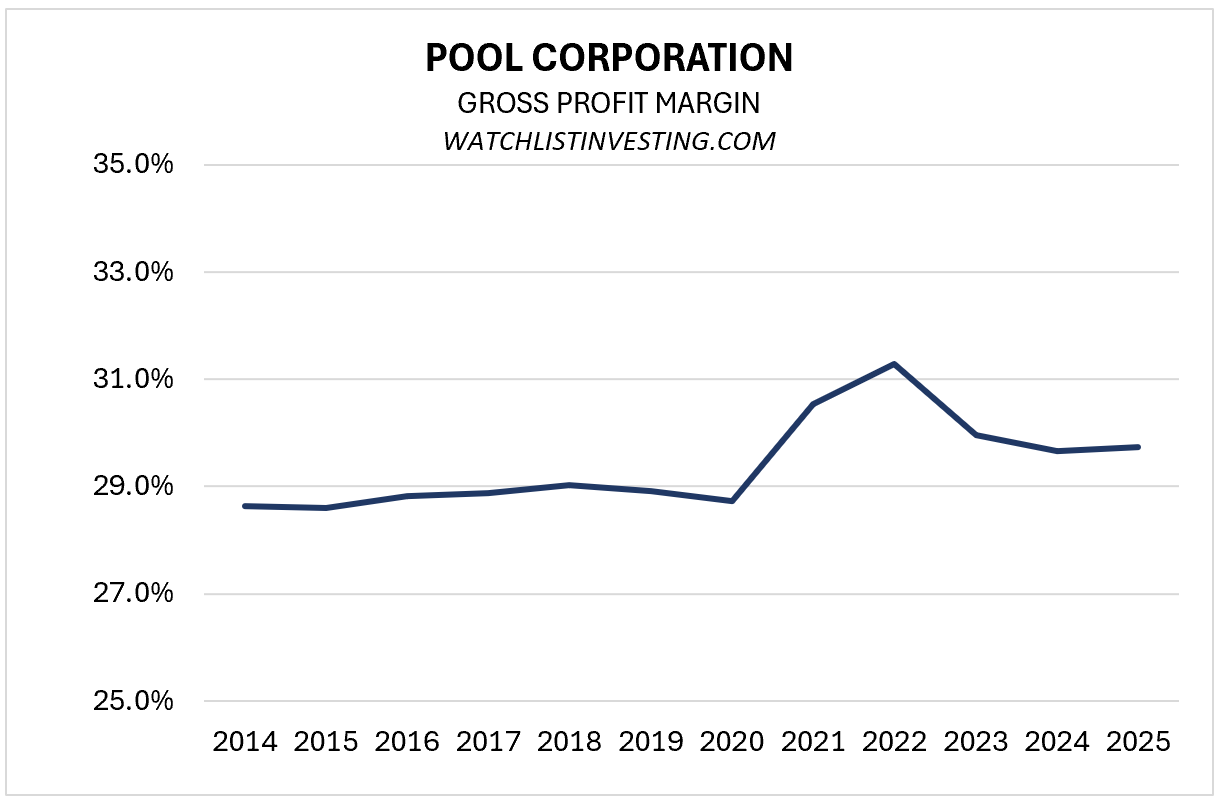

Thank the pandemic for the surge in at-home spending and the related product shortages that allowed a temporary surge in margins (just look at that bump in the second chart below).

Additionally, Pool acquired Porpoise/Sun Wholesale in December 2021, resulting in a structural increase in its distribution capabilities.

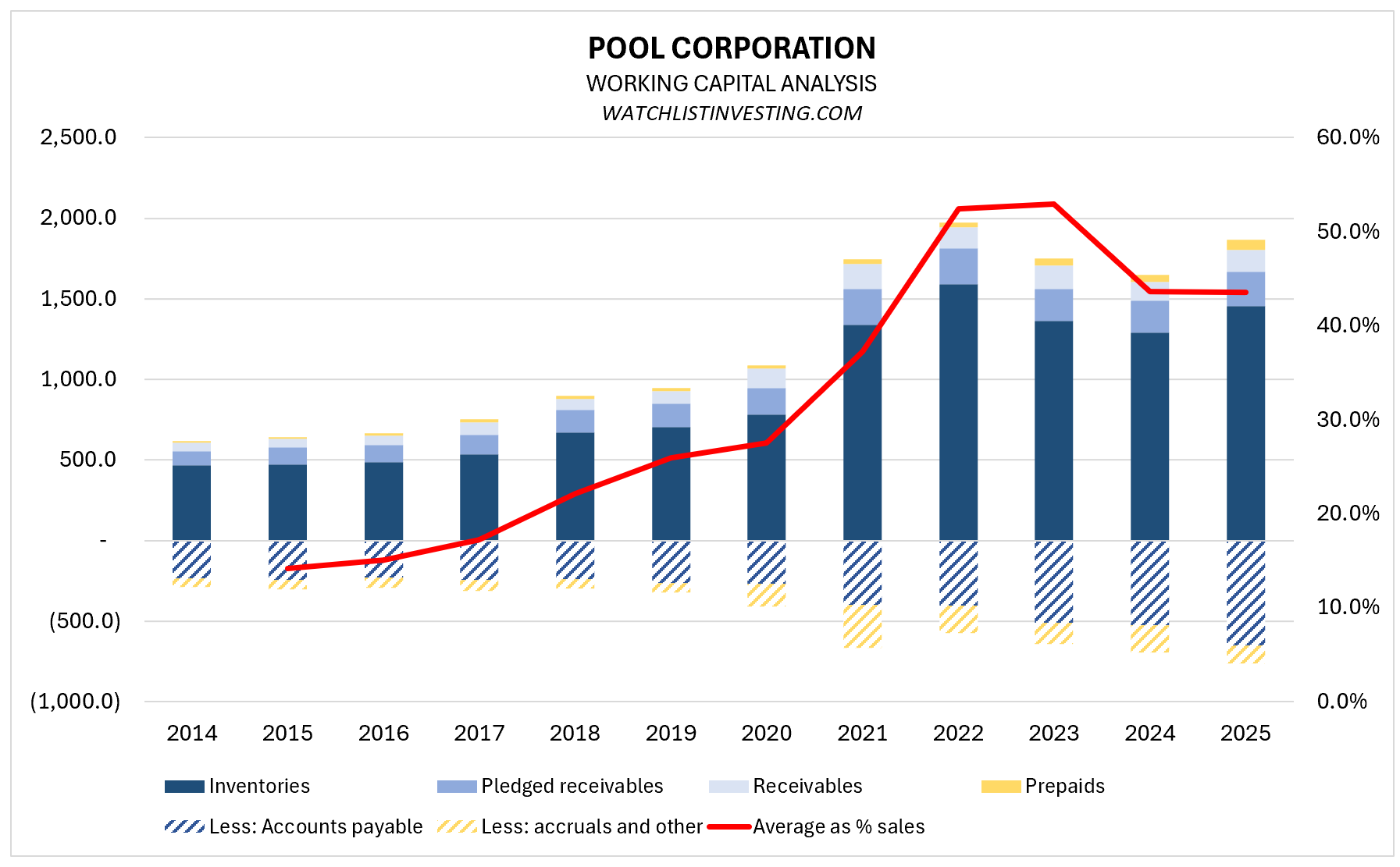

Working Capital

Pool Corp’s working capital structure is a function of its distribution model. The company carries significant inventory (purchased from manufacturers, including early-buy pre-season inventory) financed in part by accounts payable to those manufacturers.

The structural shift toward more working capital as a percentage of sales is a function of a few things:

Pre-pandemic increase in SKUs, sales center growth, and early buy program (where Pool buys inventory ahead of time from suppliers at a discount)

Product shift toward equipment/building products

Pandemic spike

Drawdown to a post-pandemic plateau reflecting the above factors (more SKUs and broader geographic footprint), in part from the Porpoise acquisition in late 2021.

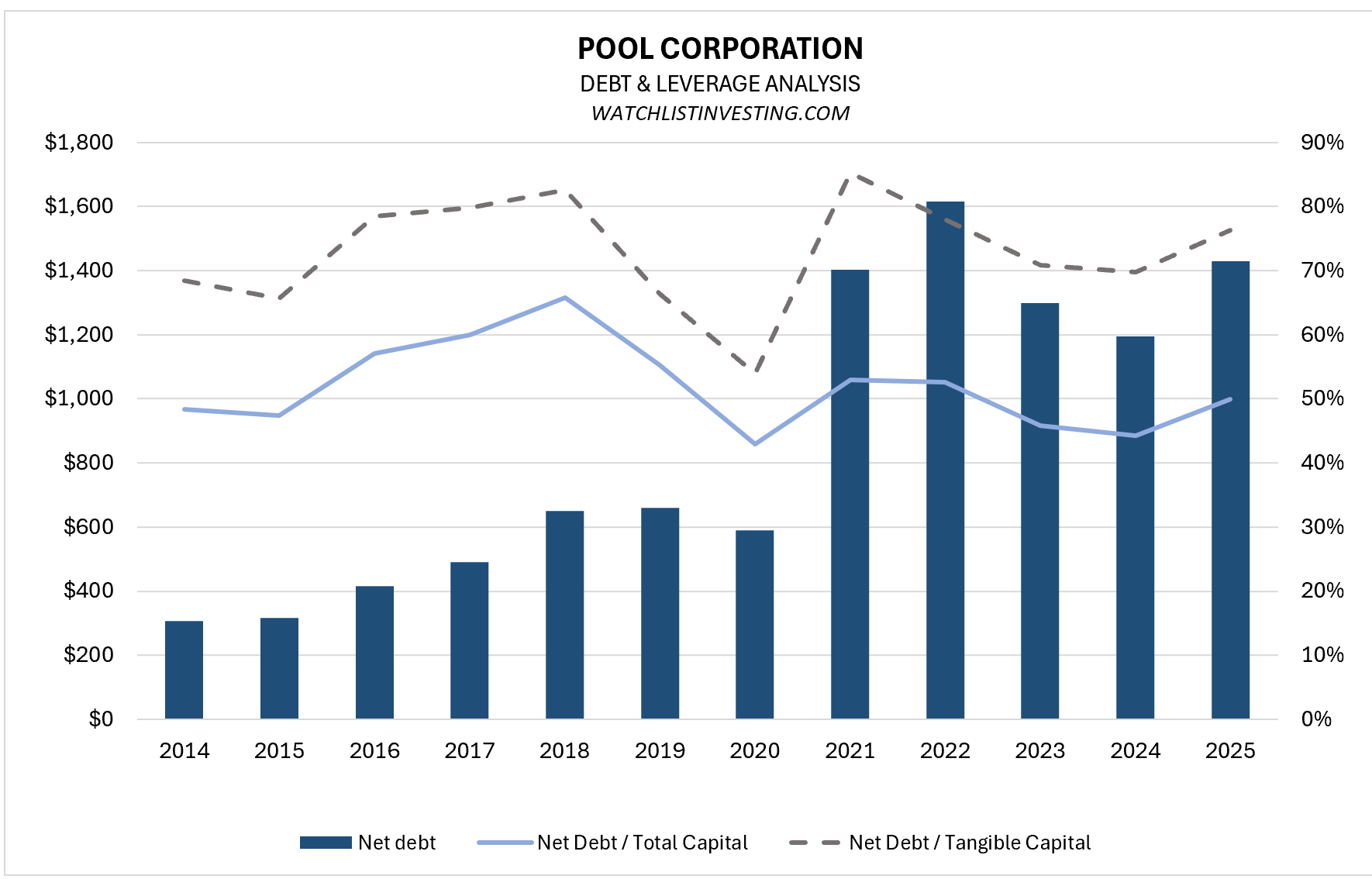

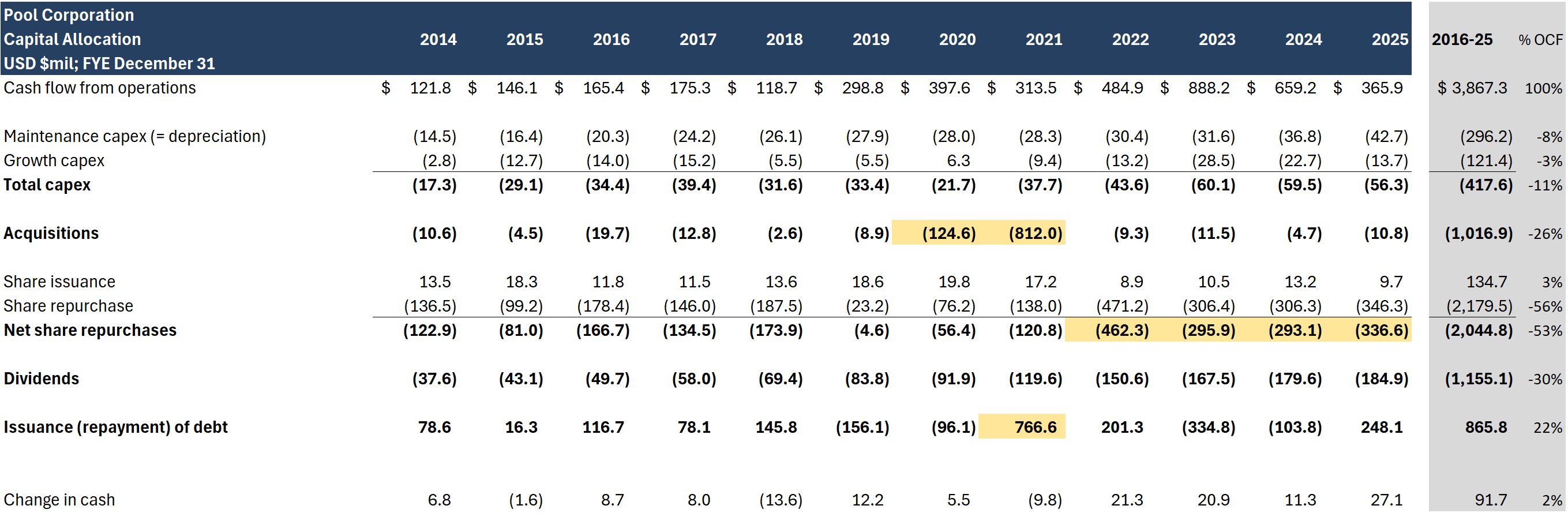

Balance Sheet & Capital Allocation

Pool took on debt to fund the Porpoise acquisition in 2021. From a traditional debt to equity/capital/tangible capital, leverage has remained flat. However, debt now stands at a somewhat worrisome 7.5x EBIT.

Over the last 10 years (2016-25), Pool:

Spent 11% of cash flow from operations on capex, including 3% on growth

26% spent 26% on acquisitions, with the largest being Porpoise ($788.7MM) and four tuck-in acquisitions in 2020

53% on net share repurchases

30% on dividends

Funded by $866 million (22% OCF) of new debt

I’m wary of management taking on debt to fund big share repurchases when the balance sheet is already moderately encumbered.

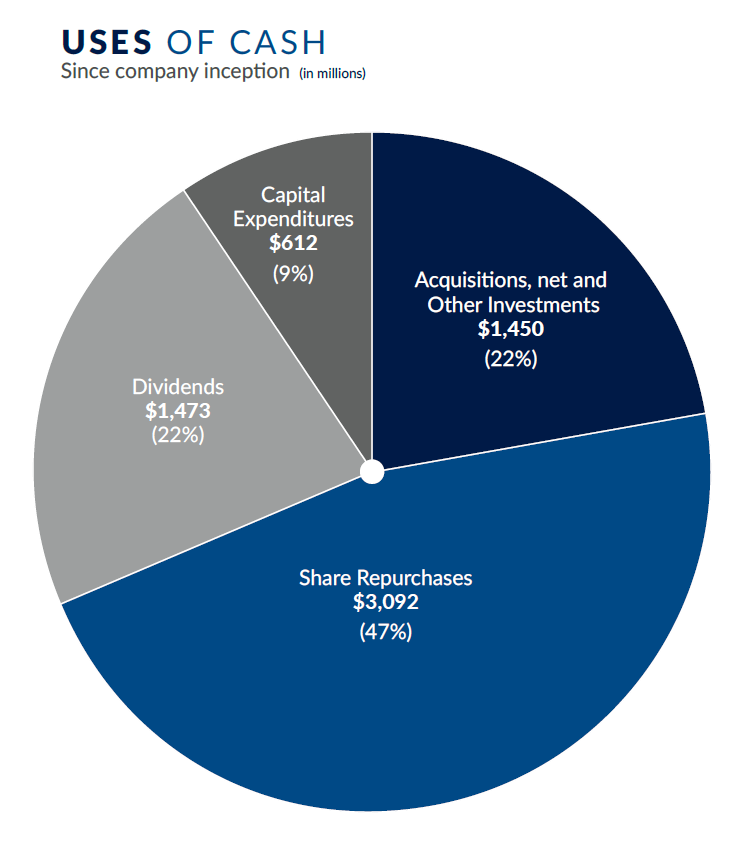

Here’s an interesting chart from the 2025 annual report showing the company’s uses of cash since inception.

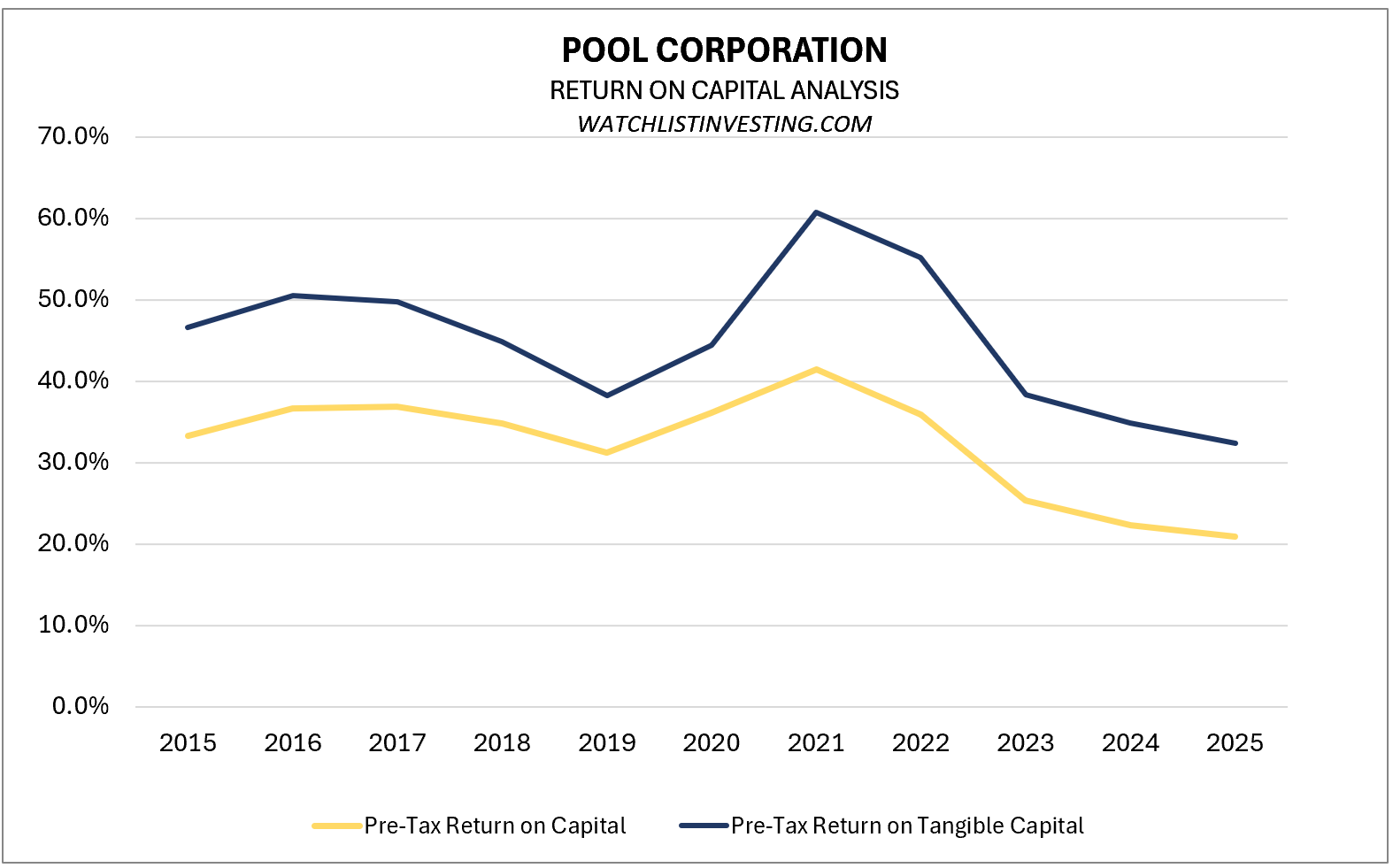

Return on Capital

Pool generates very strong returns on total and tangible capital, although those returns have come down from their post-pandemic peaks.

In the working capital section, I noted that Pool’s capital investment appeared structurally higher. I wonder if that means capital turnover will cap at about 2.0x. Similarly, margins would appear to be normalizing around 11%. If those two factors hold, then pre-tax return on total capital will stabilize around 20%. At 3.0x for tangible capital turnover, pre-tax return on capital would be 30%.