BrightView Holdings (BV)

A first look into a landscaping services play

Disclosure: None

Note: This first look is not intended to be exhaustive. This is my first time looking at the company. This post is intended to share my findings, both positive and negative. The overarching goal is to learn about a new company and put it on both our radar screens.

Overview

BrightView is the largest provider of commercial landscaping services in the United States. Such language evokes a behemoth, but BV is a relatively small company in absolute terms.

For its fiscal year ended September 30, 2025, the company reported revenue of $2.7 billion. Its market cap is just $1.25 billion.

BV operates in an extremely fragmented industry. Its “largest provider” status was achieved with a 1.7% market share of a $113 billion commercial market that includes landscape maintenance ($88 billion) and snow removal ($25 billion). This is to say nothing of the residential market.

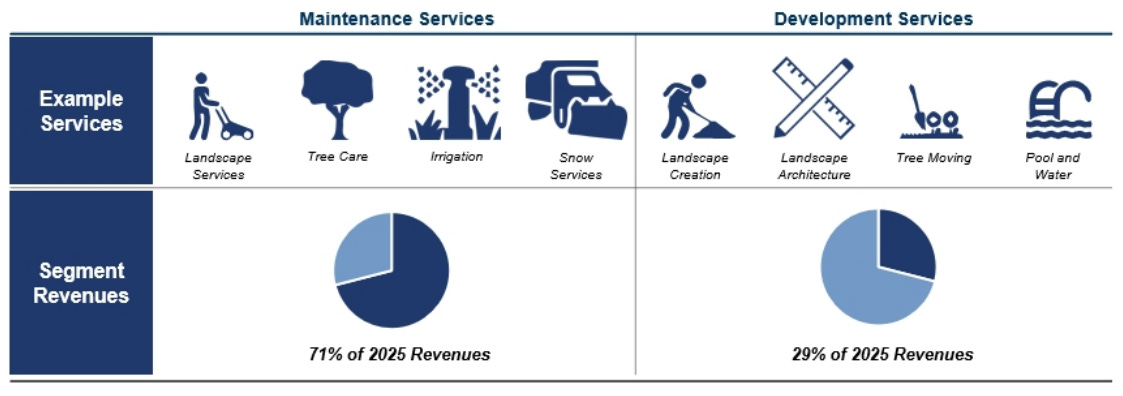

The company operates in two segments: maintenance services and development services, as detailed in this snapshot from the 2024 annual report:

Focusing on the commercial segment allows BV to leverage its sales force to acquire larger customers (lower CAC) and develop recurring revenue.

The company is executing a fairly standard consolidation playbook of centralizing certain functions and standardizing equipment across the enterprise.

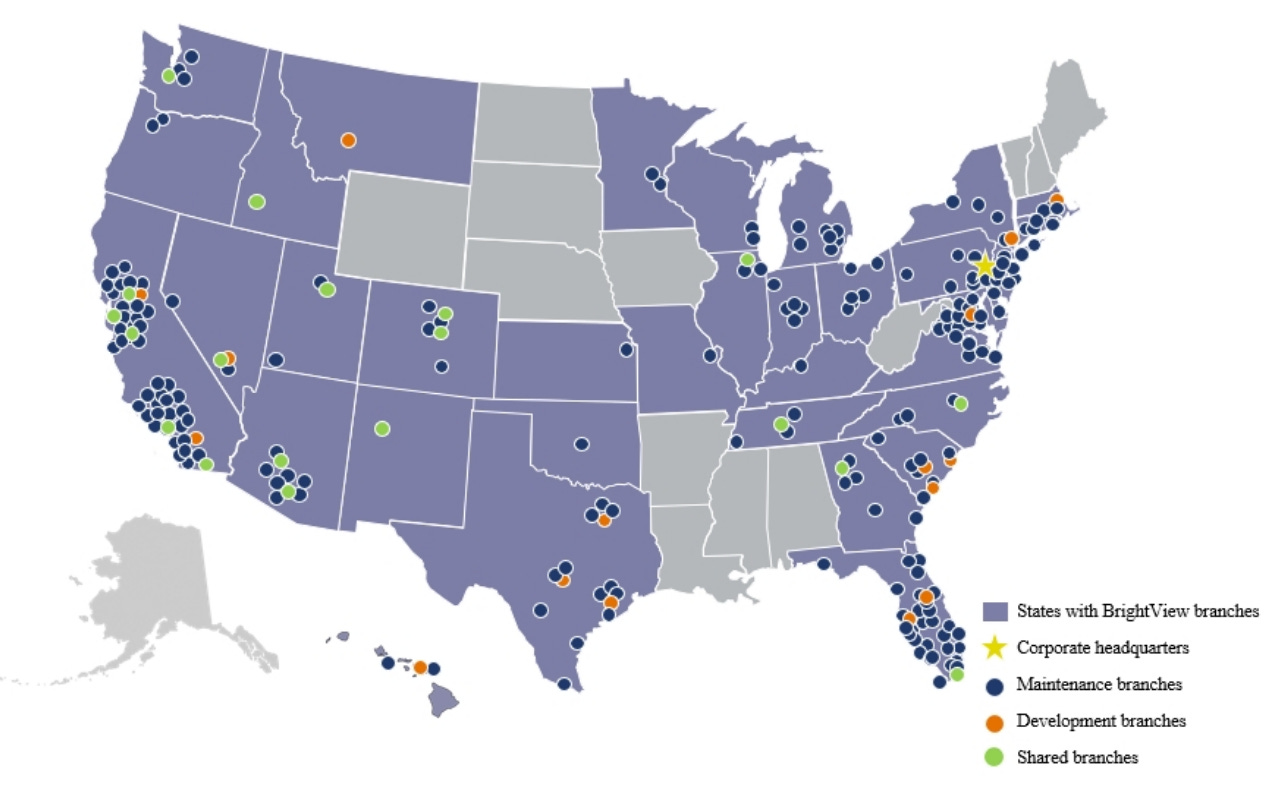

As seen below, its footprint remains sparse, highlighting an opportunity for future expansion and consolidation.

Northern markets are classified as seasonal markets that typically include snow removal, while southern markets are “evergreen” requiring landscape maintenance all year.

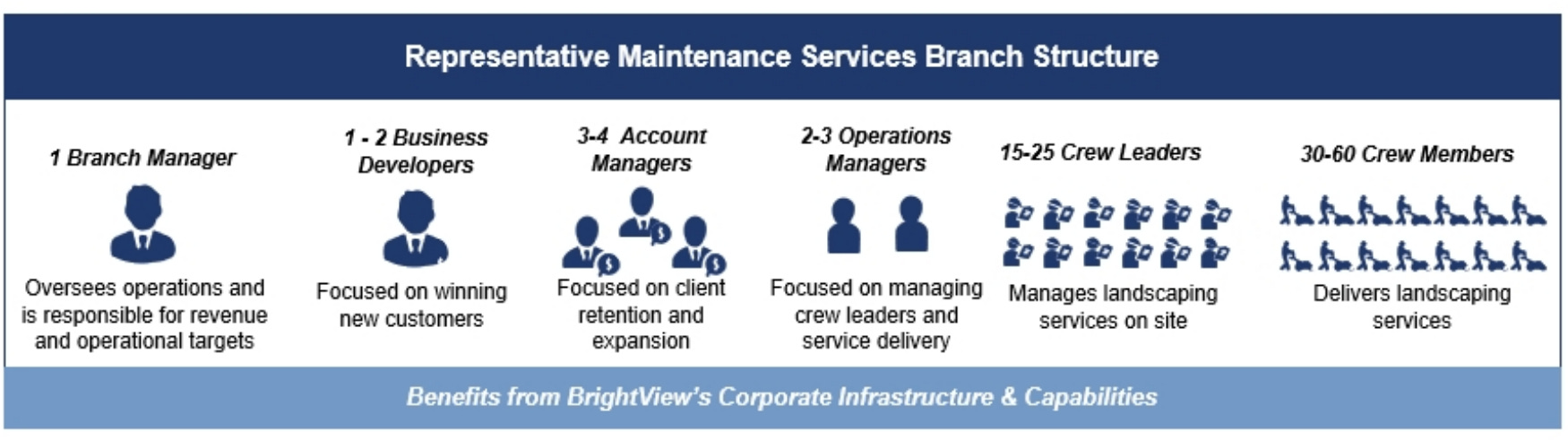

Branch Model

BV’s branch model delivers services to corporate and commercial customers, HOAs, public parks, hotels and resorts, hospitals, educational institutions, retail establishments, golf courses, and more, through its 280 branch network.

The company boasts 11,700 office parks and corporate campuses, 10,000 residential communities, and 700 educational institutions, and serves as the "Official Field Consultant” for Major League Baseball (whatever that means).

Branches serve both maintenance and development customers. Each branch services between 25 to 100 customers across 50 to 250 sites and generates between $2 and $22 million of annual revenue.

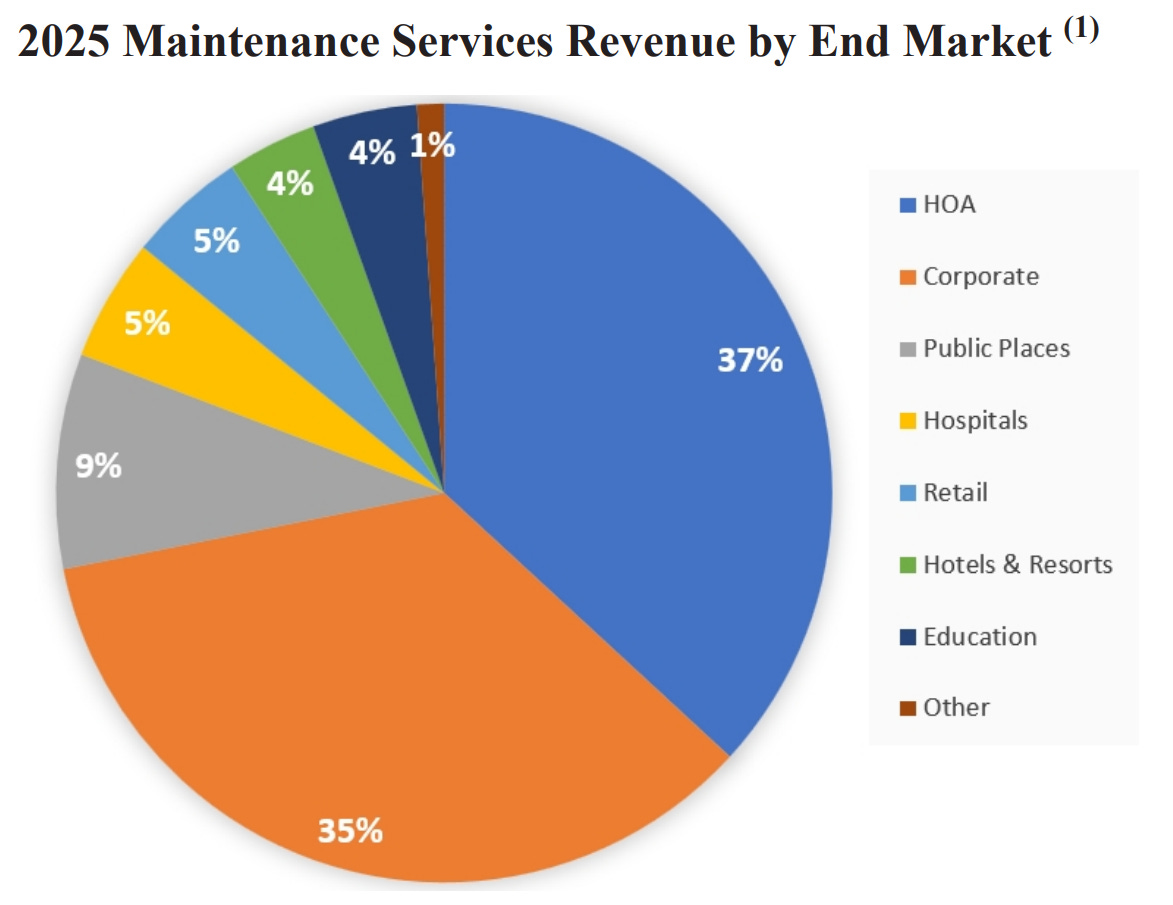

Here’s 2024 maintenance services broken down into end market:

The company’s development services segment is more project-based. Projects can range from $100,000 up to $10 million, with an average size (2024) of $1.3 million. BrightView may be hired by a general contractor on larger jobs, and on these and other projects, it manages downstream services providers such as fencing installation.

A Short History of BrightView

2013; Affiliates of KKR acquire Brickman Holding Group, an entity with roots dating to 1939.

2014: Acquisition of ValleyCrest (founded in 1949), which doubled the size of the company. Changed its name to BrightView.

2018: July initial public offering.

2023:

August: $500 million preferred equity investment by One Rock Capital Partners to support deleveraging and expansion.

October: Dale Asplund becomes president and CEO (Oct. 1).

November: The company launches One BrightView to transform the business.

2024: Divested its US Lawns subsidiary for $51 million cash

2025: Board initiates $100 million share repurchase program

As of September 2024, the company had 19,100 employees with 15,750 in maintenance services, 2,950 in development, and 400 corporate.

Management / Ownership

CEO and President, Dale Asplund has been in his role since October 2023. He served as COO of United Rentals since 2019 and was with that company since 1998. In 2024, Asplund earned a base salary of $950,000 and a bonus of $1.235 million. He was granted $4 million worth of RSUs and PRSUs in November 2024.

Chairman of the Board is Paul Raether, a senior partner at KKR.

Directors earn about $100,000 in cash compensation plus $120,000 in stock awards.

Ownership is as follows:

Investment funds affiliated with KKR: 22.1%

Investment funds affiliated with One Rock: 36.2%

Directors and officers: 2.2%

The Series A Preferred Stock held by One Rock is convertible into common shares at a rate of 105.9 common per preferred share at a price of $9.44.

Financial Analysis

Note: September 30 Fiscal Year End

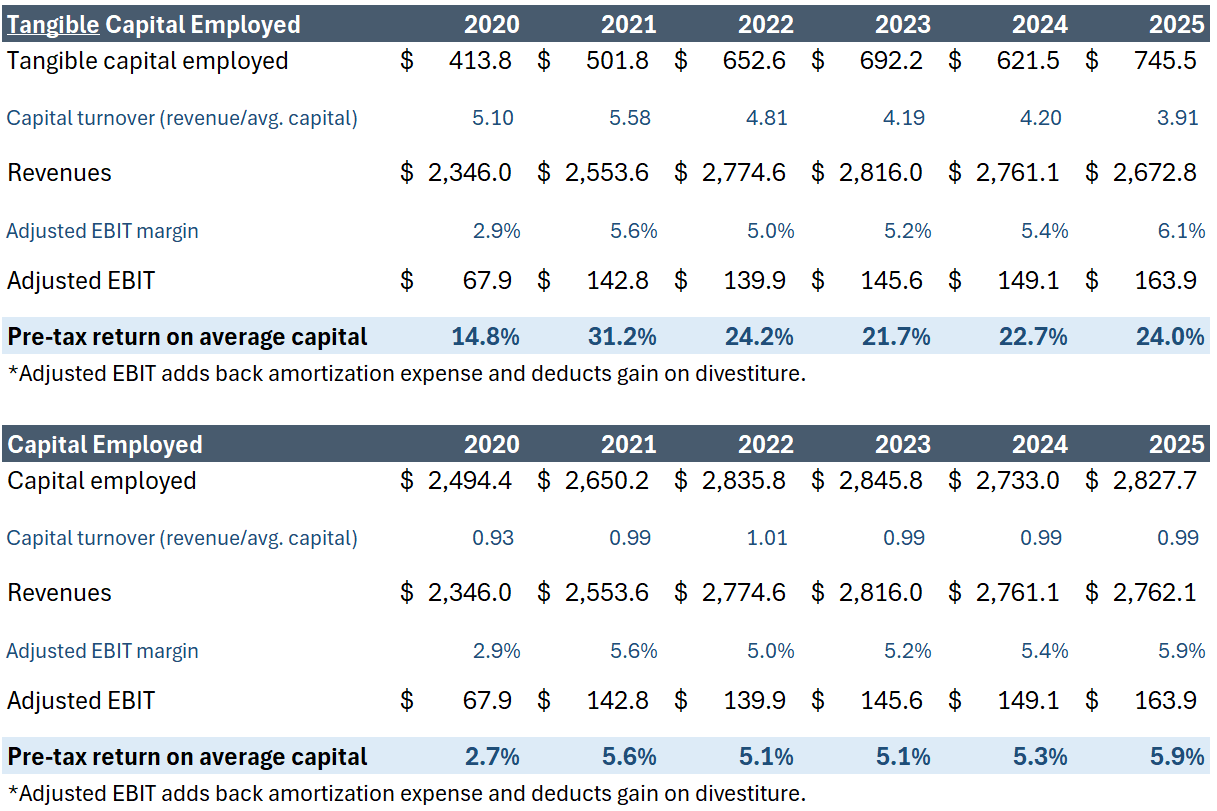

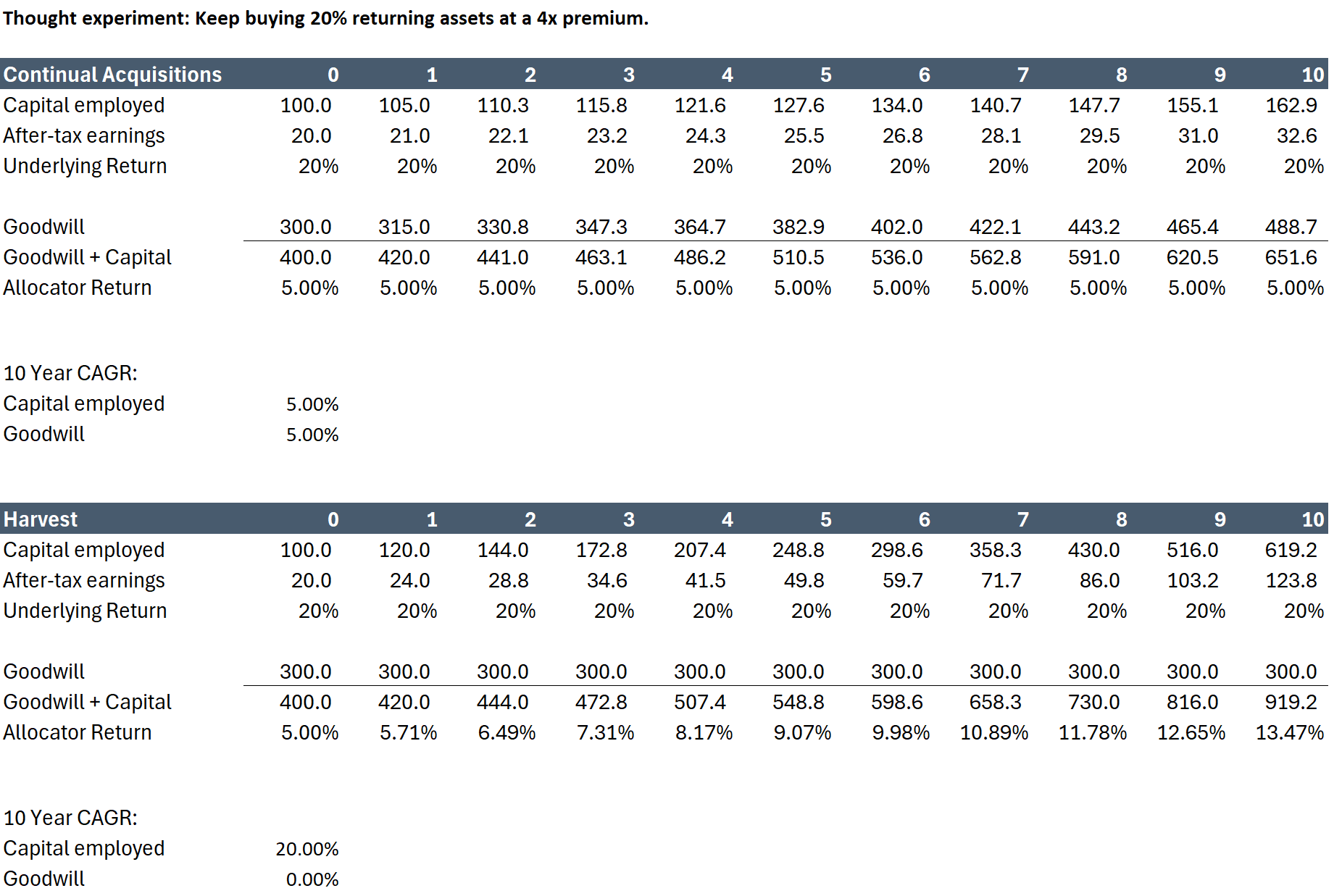

Right from the start, we have a dilemma of sorts. BrightView has grown through acquisition and has a huge amount of goodwill and intangibles on the books. At the end of FY 2025, goodwill was over $2 billion, and intangibles amounted to $66 million.

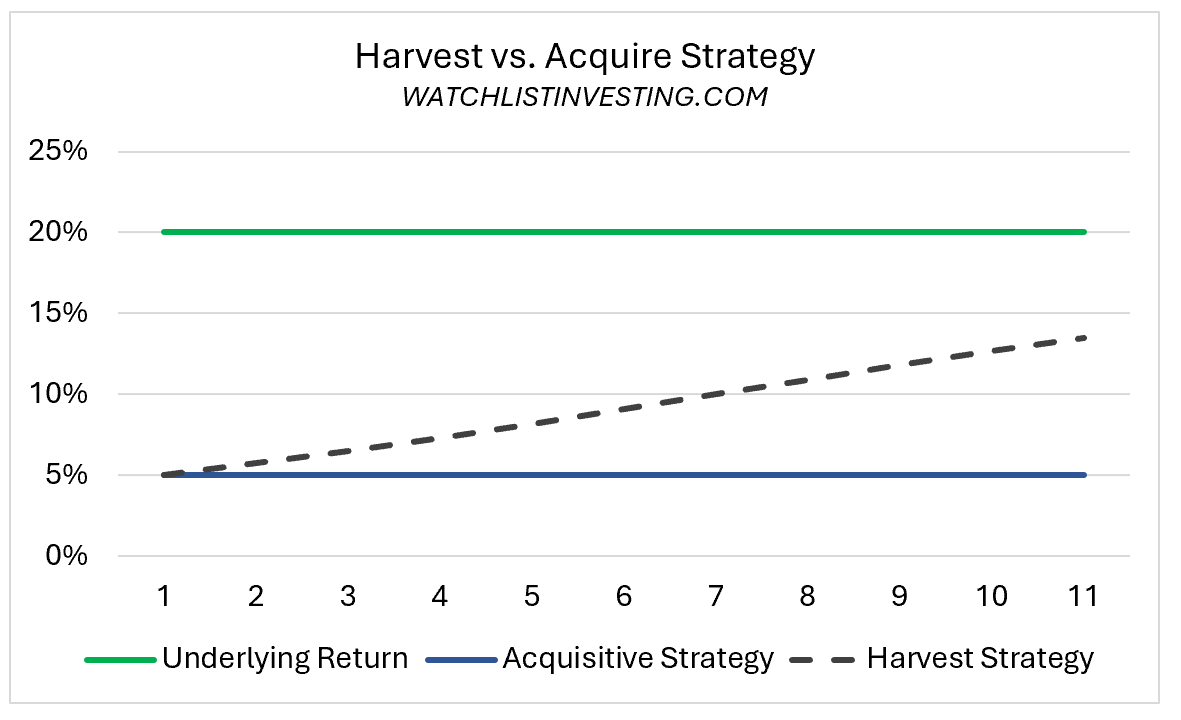

This dynamic is the result of a highly acquisitive company paying a premium for good properties. This is how I square that circle…

Tangible capital tells us the quality of the underlying business. In this case, it appears the operating assets BV is working with produce solid returns in the low-to-mid 20s.

Including goodwill gives us the capital allocator score. In this case, in the mid-single digits.

In short, management found good assets but paid a premium for them. That lawnmower mows the same amount of lawn whether you paid book value or 2x book value for it.

Strategy plays a big part in my thinking on this front. If the playbook is to continue to acquire assets at a premium, well, I’m probably out at this point. That’s real cash going out the door.

But (and this appears to be the case here) if you slow/stop acquiring and either harvest cash and/or grow organically, the total capital employed figure begins to approach the tangible figure as high incremental returns are achieved.

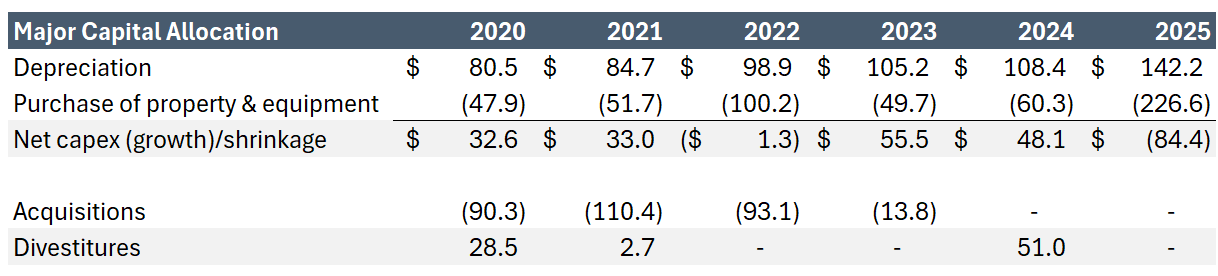

Take a look at BV’s capital spending. From 2020 to 2024, the company shrank its investment in PP&E as acquisitions brought assets onto the balance sheet. (Note the similarities to Heartland.) Then, in FY 2025, the company ramped up organic spending, primarily on operating equipment and vehicles.

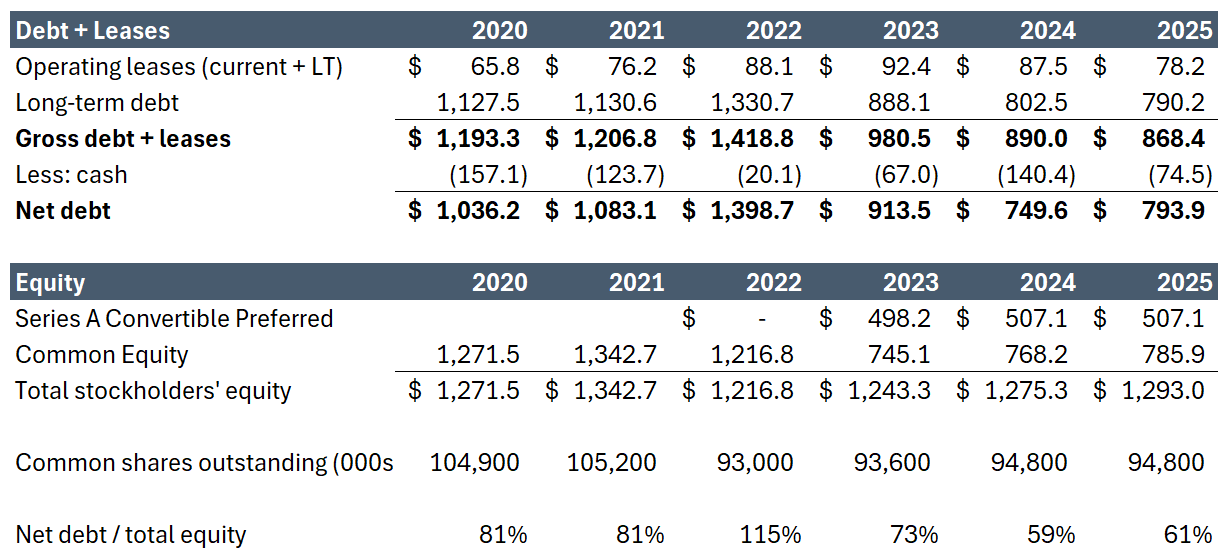

Capital structure is important, and BrightView has a few things going on here. For starters, it has and continues to carry a fair amount of debt.

In August 2023, One Rock Capital injected $495 million via a Series A Convertible Preferred issue, with 90% of the proceeds used to repay debt.

Of importance, BrightView maintains a $325 million receivables financing facility. In FY 2025, it borrowed $14.5 million and repaid $29.1 million. The FYE 2025 balance of $61.6 million is included in long-term debt.

Valuation

In my view, BrightView’s acquisition strategy determines if valuing it even makes sense. If it’s going to continue buying assets at a premium that results in a mid-single digit return, then that’s the return shareholders can expect.

However, if it begins to reinvest capital organically at the same return as the existing underlying return, then the upward drift could make the investment attractive.

Here’s how that looks graphically, with the numerical backup below.

Let’s assume management isn’t going to resume expensive acquisitions. Let’s also assume that FY 2025 EBIT of $164 million is a good estimate of current earning power. This considers recent margin expansion but doesn’t give credit for any future gains in efficiencies, but we have to draw the line somewhere.

With EBIT at $164 million and assuming a tax rate of 25%, earnings (NOPAT) would be $123 million. At a straight 10% discount rate, that’s worth $1.23 billion.

What about growth? Let’s use round numbers and assume the underlying return on capital is 25%. To grow at 5% would require $37 million ($746 million tangible capital x 5%), leaving $123 million - $37 million = $86 million distributable cash flow. At 5% (10% - 5% growth) that’s worth $1.72 billion.

Ok, so much for the value part, what about the price?

At $13/share as of this writing and 94.8 million shares outstanding, the common equity has a market value of $1,232 million. Then there’s $500 million in preferred plus about $800 million in net debt.

$1,232 million common equity market value

$500 million preferred

$800 million debt

$2,532 million enterprise value

Deconstructing the value equation above, the $2.5 billion enterprise value implies that the company would need to grow at 7% organically forever. Again, margin improvement directly impacts the bottom line, so your assumptions in this area matter.

Reality, of course, will be different. The company may pay down debt (increasing equity value), and/or it might make some acquisitions. And it may find operating efficiencies that accrue to the bottom line.

Note that management considers shares undervalued at current levels. The company spent about $25 million on buybacks in FY 2025.

Conclusion

To wrap this up, I’m intrigued. Here’s the market leader with less than a 2% market share in a fragmented industry. Underlying returns on tangible capital appear very attractive. But the company’s history of acquisitions, while perhaps justified to provide scale, could mute returns to shareholders.

There’s also the fact that KKR and One Rock control the business, a fact that should be weighed carefully.

BrightView is a pass for me right now, but I intend to check in from time to time to see how the story develops.

If you’ve made it this far, I’d be very grateful to you for your feedback on this post. It’s just two questions and will go a long way toward helping me improve Watchlist Investing. Thank you!

Stay Rational!

Adam

Pre-Order the 2nd Edition Now!

Amazon, Barnes & Noble, or directly from Harriman House, and at other major bookstores, for delivery in April 2026.

Praise for the 2nd Edition

I’m incredibly grateful for the people who took the time to review early drafts of the new material and provided feedback, as well as praise for both editions:

“If you want to understand how Warren Buffett built Berkshire Hathaway into one of the most valuable businesses in the world, you have to read this book. This is your opportunity to stand beside Picasso as he paints each brush stroke. A must read for all Buffett and Berkshire groupies.”

- Bill Ackman, Founder and CEO of Pershing Square

“I and my teammates at the Gabelli Organization have been tracking Warren’s success for some 50 years. Adam’s book captures the work and highlights the history of Berkshire and the hard and diligent work of Buffett and Munger, Jain and Abel, and Combs and Weschler.”

- Mario Gabelli, Chairman and CEO, Gabelli Funds

“Adam Mead’s discussion of the values and virtues which have shaped Berkshire Hathaway over 50 years is a must read for those investors in search of the forces that have delivered such investment value over time.” – Thomas A. Russo, Gardner Russo & Quinn LLC

“Few activities can be more rewarding for any value investor than studying the history and evolution of Warren Buffett and Berkshire Hathaway. Adam has done us a huge favor with his yeoman efforts in producing this treatise. Since it is chronologically ordered, it is an invaluable reference guide for all things Berkshire.” — Mohnish Pabrai

“Adam continues to deliver a resource very valuable to both Berkshire fans and the investor community as a whole, his depth of knowledge is clearly demonstrated here again. I thoroughly enjoyed this latest addition.” - Dan Calkins, Chairman & CEO, Benjamin Moore

“The question must be asked, ‘Why another Berkshire book?’ When you read this monumental effort by Adam Mead, the answer will be obvious. Read cover to cover, both the uninitiated to Berkshire and its most ardent followers will derive enormous utility and satisfaction from it. I learned so many new and important things about Berkshire and its history. It is my pleasure to encourage you to enjoy this gem.”

- Christopher P. Bloomstran

“Whatever Adam writes is always first-class - guaranteed.

-Andy Kilpatrick, Author, Of Permanent Value: The Story of Warren Buffett

“With this project, Adam has done a wonderful job extending the Berkshire Classroom by providing a comprehensive analysis of the rich corporate history and unique entrepreneurial leadership.” — Mac Sykes, Gabelli Funds

“Adam Mead’s The Complete Financial History of Berkshire Hathaway is the definitive history of Berkshire. While there have been countless books written about Warren Buffett’s investment approach, none have so meticulously documented Berkshire’s capital allocation decisions from the very beginning. The depth of research is staggering, transforming the complex and sometimes chaotic story of how a small textile mill became a financial conglomerate into a clear, year-by-year narrative of every significant investment and acquisition. In this updated edition, Adam carries the narrative through Berkshire’s sixth decade and the methodically planned leadership transition to Greg Abel. For students of business history, this is an indispensable resource.”

-Patrick Gaughen, President and Chief Operating Officer, Hingham Institution for Savings

“The definitive story of Berkshire Hathaway—how Buffett and Munger turned a failing textile mill into one of history’s greatest wealth-creating enterprises, with timeless lessons in business, investing, and leadership.”

-Vitaliy Katsenelson, CEO of IMA, Author of Soul in the Game

“Berkshire Hathaway is a company with few, if any, parallels in business history. Under the leadership of Warren Buffett, it was transformed from a New England textile mill that would ultimately be shuttered to a sprawling conglomerate with a market valuation of more than $1 trillion. With this updated edition of “The Complete Financial History of Berkshire Hathaway”, Adam provides a thorough review of the key decisions that created the modern Berkshire Hathaway, an outcome inextricably tied to the investment and business wisdom of Warren Buffett and his business partner, Charlie Munger. In a few hundred pages, Adam adeptly runs through six decades of Berkshire’s history. For Buffett and Munger fans who want to truly understand how Berkshire was created, this book is a must read.”

- Alex Morris, Founder of TSOH Investment Research and the Author of Buffett & Munger Unscripted

“A meticulous chronicle of Berkshire Hathaway’s remarkable final act under Buffett’s leadership. Mead’s granular analysis of Buffett’s capital allocation decisions—from the $78 billion in share repurchases to the masterful Apple investment—provides unmatched insight into how the world’s most successful conglomerate navigated unprecedented scale and succession challenges.”

-Tobias Carlisle, Portfolio Manager, Acquirers Funds®

“This exceptional history of Berkshire Hathaway will appeal to history buffs, finance enthusiasts, and investing professionals alike. Mead combines rigorous research with remarkably clear storytelling, tracing the company’s ascent from a struggling textile mill to one of the world’s most admired conglomerates. The book is impressively detailed yet fully accessible—equally valuable for students learning the foundations of investing and for seasoned professionals looking to deepen their understanding of Berkshire’s evolution.”

-Gillian Zoe Segal

“With his ability to make complex things seem simple, Warren Buffett made the difficult work of building Berkshire Hathaway look easy. With this excellent history, Adam Mead takes us behind the scenes to see the details of how that work happened and was so successful. For anyone interested in Berkshire Hathaway, or the development of American capitalism, this is essential reading.”

- Bryan Lawrence, Founder, Oakcliff Capital

“There is simply no book that details the economic lore of Berkshire Hathaway better. A true exposé that every intelligent investor should read.”

- Gwen Hofmeyr, Founder, Maiden Financial

“The most comprehensive book on Berkshire Hathaway that has ever been written. It belongs on the shelf of every business enthusiast!”

-Andrew Wagner, Author of the Economics of Online Gaming and Founder & Chief Investment Officer of Wagner Road Capital Management

“Adam’s accounting of the Financial History of Berkshire is like candy for Finance and Business Junkies alike. It’s a must read if you’re interested in studying the greats.”

- Carter Johnson, Managing Partner, Singleton Valuations

“I thought nothing else of value could be written about Warren Buffett. I was wrong. Adam’s detailed chronology of Berkshire’s evolution reveals the successes and failures of Warren in a unique and digestible way. A worthwhile read for every Buffett scholar, amateur and professional alike.” — Drew Estes, Banyan Capital

“Mead has done the Berkshire faithful an incredible service by stitching together the narrative and numbers so tightly, you can see the compounding in action—updated and genuinely useful.”

-Jacob Taylor, CEO of Baserate

“Adam Mead’s work reminds us that true value is found not just in numbers, but in the lasting quality where few care to linger. By doing exceptional due diligence his book clones the lessons of Warren and Charlie.”

-Jeff Gilbert

Adam Mead’s updated “Complete Financial History of Berkshire Hathaway” is a book like no other—chronicling six decades of evolution while reminding us that Berkshire, though Buffett’s masterpiece, remains subject to constant change—an indispensable addition to any serious investor’s bookshelf.

-Bogumil Baranowski, Founder of Blue Infinitas Capital, Author of “Money, Life, Family”, Host of Talking Billions Podcast