Boston Beer Q1 Update

A very attractive entry point amid current uncertainty.

Disclosure: Long SAM.

At $176/share, Boston Beer shares are down 33% from their 52-week highs. With 10.47 million shares outstanding, the current share price implies a market cap of $1.84 billion.

SAM has $129 million of net cash (no LTD + operating leases), but there’s a big asterisk next to it.

Ardagh Litigation

The big negative news of the quarter was a $216 million pre-tax charge ($162 million after-tax at 25%) related to a contract dispute with Ardagh Metal Packaging. A jury awarded Ardagh $175.5 million for SAM’s failure to meet contractual minimum purchases of aluminum cans during the height of the hard seltzer boom. The $216 million figure includes $36.5 million of pre-judgement interest expense and $4 million of legal fees (in G&A).

SAM says it will appeal the verdict. With absolutely no real knowledge of the legal merits of the case, I think it seems likely that SAM will have to pay. With no debt, cash on hand, and a $150 million line of credit, if/when SAM pays, it shouldn’t cause operational issues.

Operational Highlights

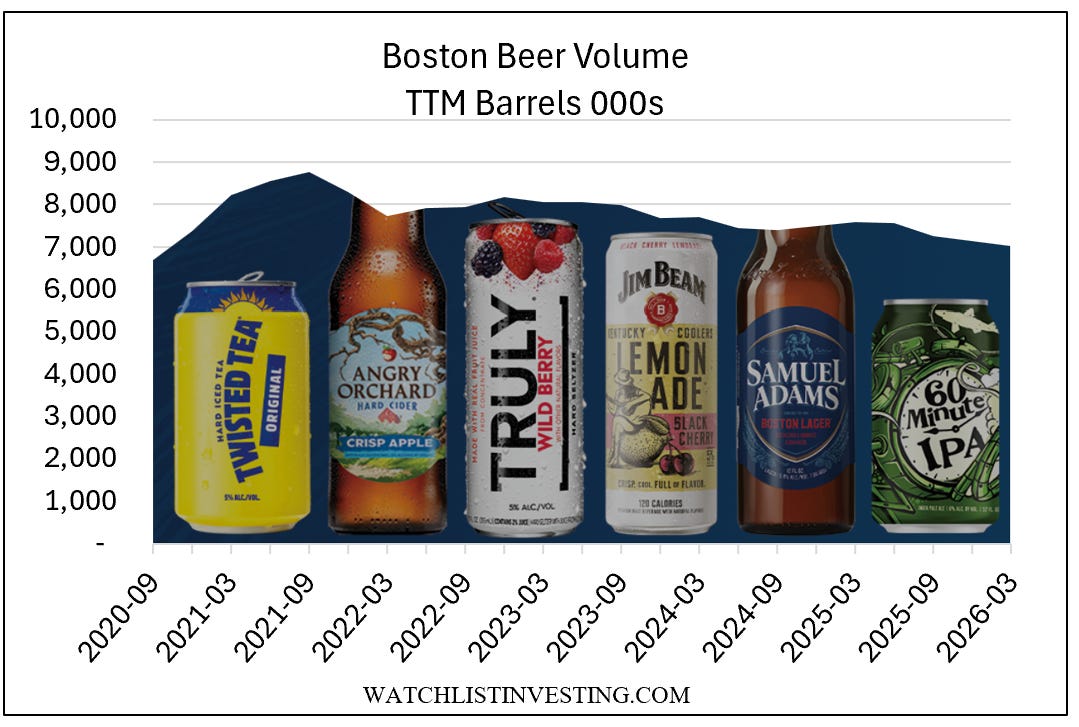

Volume/Pricing

The key driver for a beverage company is volume. You can’t generate revenue or profit if you don’t sell beer.

Q1 2026 volume of 1,561,000 barrels, a decline of 6.9% compared to the same quarter a year ago. Of note, this figure represents shipments. Depletions (distributor inventory) declined at a slower 4% rate.

The company produced 95% of its volume in-house during the quarter.

TTM volume was 7,025,000 barrels, a decline of 7.3% from a year ago.

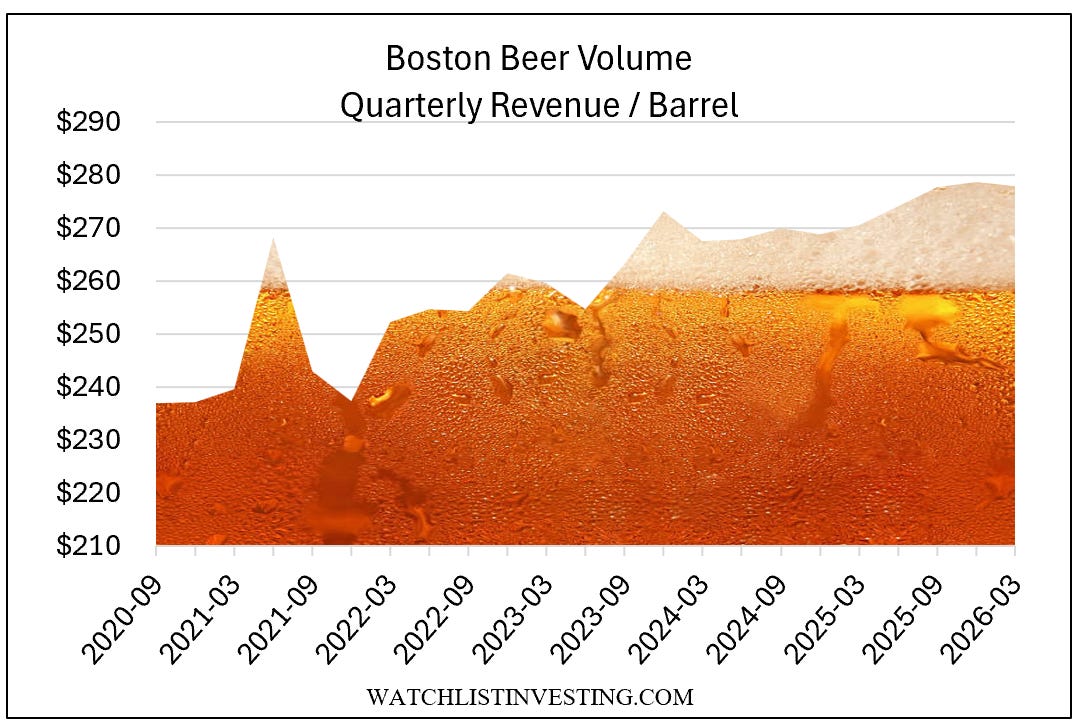

On the plus side, pricing (rev/barrel) increased 2.7% Q/Q and 2.8% on a TTM basis.

At a recent industry conference, the company’s CFO noted that beer was around 18% of volume, putting SAM solidly in the beyond beer category. He also highlighted the company’s expertise in creating brands, putting it at an advantage over larger rivals who must pay premium multiples to acquire them.

The company’s Sun Cruiser brand, which was launched in-house, is a bright spot offsetting some weakness in Twisted Tea and Truly.

Revenue

Q1 2026: $433.9 million, down 4.7%

TTM: $1,945 million, also down 4.7%

Costs and Expenses

Gross margin came in at 49.3%, up 100 bps from a year ago.

SAM posted a $190 million operating loss due to the $216 million litigation expense. It also reported a $2 million impairment of brewery assets.

On the expense front, advertising, promotional, and selling expenses increased 200 bps to 32.3% as the company continues to invest in its brands ahead of summer.

SG&A increased 150bps to 12.1%; 100bps to 11.1% excluding $4 million legal fees.

Overall, the operating margin was negative due to the litigation expense. Ex. litigation, operating margin declined 240bps to 5.0%.

TTM operating margin was 7.2% ex. litigation expense, down from 8.3% a year ago.

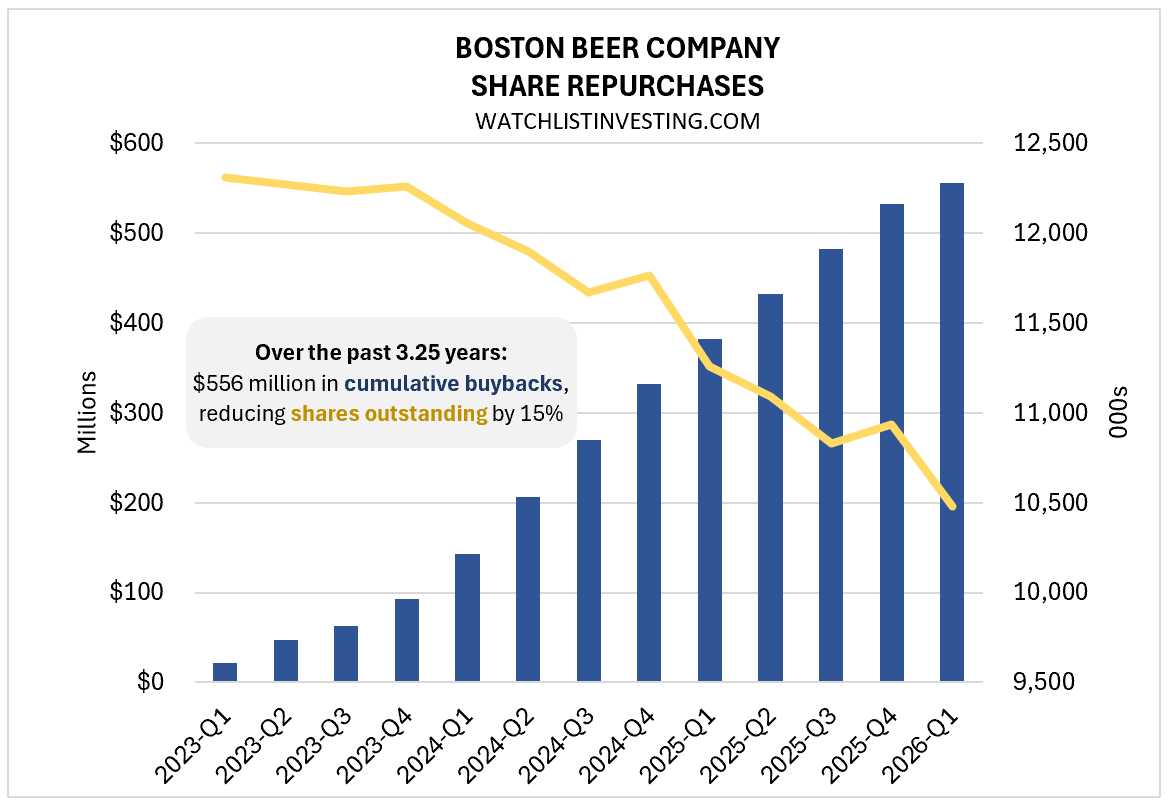

Capital Allocation

As noted above, SAM has no LTD and only modest operating lease liabilities.

From December 28, 2025 to April 24, 2026, the company repurchased 137,912 shares of its Class A stock for $31.2 million ($23.3 million in the quarter itself through March 28), implying a price of $226/share.

Valuation

With 10.5 million shares outstanding at a current price of $175/share, SAM has a market cap of $1.84 billion.

From this, we can deduct $129 million net cash. I’m also going to add $162 million as a best-guest estimate of the after-tax litigation cost.

That leaves an enterprise value of about $1.87 billion, fully accounting for the litigation expense.

Revenues are running at ~$2 billion a year. I think 15% operating margins are achievable, which would be $300 million in annual EBIT or $225 million after tax.

Let’s assume it can only do 10%, resulting in EBIT of $200 million and $150 million after tax.

That puts SAM’s valuation at between 12.5x (10% margin scenario) and 8.3x (15% margin scenario). Both look compelling.

More thoughts? Let me know in a private message or leave a comment.

Stay Rational!

Adam

Pre-Order the 2nd Edition Now!

Amazon, Barnes & Noble, or directly from Harriman House, and at other major bookstores, for delivery in April 2026.

Praise for the 2nd Edition

I’m incredibly grateful for the people who took the time to review early drafts of the new material and provided feedback, as well as praise for both editions:

“If you want to understand how Warren Buffett built Berkshire Hathaway into one of the most valuable businesses in the world, you have to read this book. This is your opportunity to stand beside Picasso as he paints each brush stroke. A must read for all Buffett and Berkshire groupies.”

- Bill Ackman, Founder and CEO of Pershing Square

“I and my teammates at the Gabelli Organization have been tracking Warren’s success for some 50 years. Adam’s book captures the work and highlights the history of Berkshire and the hard and diligent work of Buffett and Munger, Jain and Abel, and Combs and Weschler.”

- Mario Gabelli, Chairman and CEO, Gabelli Funds

“Adam Mead’s discussion of the values and virtues which have shaped Berkshire Hathaway over 50 years is a must read for those investors in search of the forces that have delivered such investment value over time.” – Thomas A. Russo, Gardner Russo & Quinn LLC

“Few activities can be more rewarding for any value investor than studying the history and evolution of Warren Buffett and Berkshire Hathaway. Adam has done us a huge favor with his yeoman efforts in producing this treatise. Since it is chronologically ordered, it is an invaluable reference guide for all things Berkshire.” — Mohnish Pabrai

“Adam continues to deliver a resource very valuable to both Berkshire fans and the investor community as a whole, his depth of knowledge is clearly demonstrated here again. I thoroughly enjoyed this latest addition.” - Dan Calkins, Chairman & CEO, Benjamin Moore

“The question must be asked, ‘Why another Berkshire book?’ When you read this monumental effort by Adam Mead, the answer will be obvious. Read cover to cover, both the uninitiated to Berkshire and its most ardent followers will derive enormous utility and satisfaction from it. I learned so many new and important things about Berkshire and its history. It is my pleasure to encourage you to enjoy this gem.”

- Christopher P. Bloomstran

“Whatever Adam writes is always first-class - guaranteed.

-Andy Kilpatrick, Author, Of Permanent Value: The Story of Warren Buffett